The market dodged the Oil shock, but the rate trap is still set

Monday’s bounce was relief, not confirmation. Oil backed away from the geopolitical cliff, tech found a bid, and risk assets stabilized, but the late-day fade showed that conviction remains thin.

• The real threat is no longer just Middle East escalation. It is the possibility that stronger labour data, sticky CPI, and renewed inflation pressure force the market to price a Fed that stays tighter for longer.

• The 10 year yield near 4.5% is the key tripwire. If rates push higher while AI chipflation and oil risk linger in the background, the market’s favourite growth trade starts facing a much harsher valuation regime.

The Rate Trap Is Still Set

Monday’s price action had all the hallmarks of a market trying to convince itself that Friday’s wreckage was merely a positioning accident rather than the first groan from deeper structural timber. Global equities were still soft around the edges, but Wall Street managed to find a bid as technology shares bounced from Friday’s air pocket, oil gave back the worst of its weekend panic premium, and investors took some comfort from the suggestion that Iran and Israel had stepped back from the ledge after President Donald Trump pressed both sides toward a pause. But this was not a clean victory lap. It was the market crawling out from under the desk, brushing broken glass off the keyboard, and realizing the real danger may not have passed. It may simply have changed costumes.

The relief came because crude did not turn into the full geopolitical bonfire traders had feared at the open in Asia. After surging higher on fresh Middle East escalation, oil was pulled lower by headlines suggesting Iran had ended military operations against Israel, then bounced when Israel pushed back against Iranian warnings over Lebanon, then eased again after Netanyahu said Israel was holding fire in Iran for now. By the close, WTI was only modestly higher and Dated Brent, the more honest physical market read, ticked up but remained below $100. That matters because oil is still trading insurance, not Armageddon. The market can smell smoke, but it has not decided the refinery is on fire. My view is that as long as Dated Brent stays below the panic line and physical stress does not metastasize into cargo chaos, equities can live with geopolitical risk. They may not like it, but they can price it.

That gave risk assets just enough oxygen to breathe. Big tech and bitcoin outperformed, the dollar softened slightly, gold caught a modest bid, and bonds chopped around without delivering a clean verdict. But the equity rebound was not a stampede back into risk. It was controlled, careful, and by the final hour the sellers were already leaning back on the tape. The Nasdaq led as traders bought back the same AI names that had been taken to the woodshed on Friday, while the Dow lagged and the S&P 500 barely held much of its bounce into the close. That is not how a market behaves when conviction has fully returned. That is how a market behaves when dip buyers show up with one hand on the mouse and the other hovering over the eject button.

So the real question is not whether Monday bounced. It did. The real question is whether this was a genuine dip buying opportunity or just a dead cat with a Bloomberg terminal. Friday’s tech-led rout was not random noise. It exposed the market’s most sensitive nerve: the belief that the AI infrastructure boom can compound through any macro weather system. For months, investors have treated the AI trade like a runaway freight train with no brakes, no speed limit, and no valuation ceiling. Every wobble was explained away as consolidation. Every multiple was justified by tomorrow’s data centre. Every funding curve was treated as a footnote to the great machine age. But even the strongest secular story still has to pass through the toll booth of interest rates.

This is where the tape becomes more dangerous. Bull markets rarely die from old age. Expansions do not simply collapse because the calendar says they are tired. They usually need a catalyst, and more often than not, the assassin wears a rates badge. Friday mattered because payrolls came in hot enough to make the market question whether the labour market is cooling at all. Instead of a soft-landing glide path, investors suddenly had to price in the risk of an economy that may be reaccelerating, with a Federal Reserve that has not yet won the inflation war. That is when the market’s internal wiring changes. Rate cuts stop being the baseline. Higher for longer stops being a slogan. Additional tightening, even if only discussed rather than delivered, becomes the ghost in the machine.

That is the trapdoor sitting beneath this entire tape. The Fed does not have to spring it. The market only needs to believe the floorboards are creaking again. Once that happens, everything with a long duration dream attached to it gets repriced. AI is still real. The infrastructure build-out is still structural. The capex cycle remains one of the dominant forces in global markets. But when discount rates rise, even the most beautiful growth story starts paying rent. My trader view is simple: the AI theme is not broken, but the price investors are willing to pay for it becomes far more fragile if the 10-year yield starts acting like a wrecking ball again.

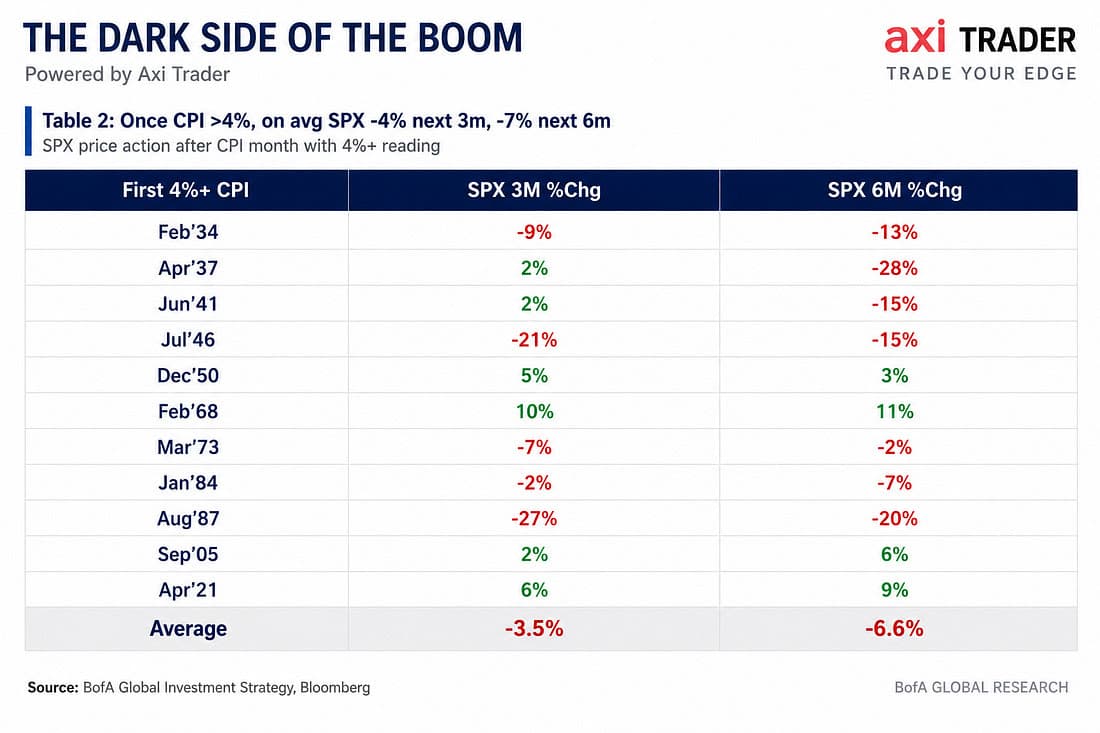

This week’s CPI report is therefore not just another macro data point. It is the next stress test for the market’s entire operating system. Inflation has already been running too hot for comfort, and if the next reading pushes annual inflation back above 4%, investors may have to confront a regime they have spent much of the past year trying to ignore. Above that level, history becomes less forgiving. Valuations become more brittle. Central banks become less patient. Bond markets stop offering sympathy. Equities no longer get the benefit of every doubt. Above 4%, the market does not trade like a smooth runway. It trades like a crowded theatre where everyone suddenly remembers where the exits are.

That is why the 10-year yield matters so much here. The stock yield correlation has turned sharply negative, meaning equities are once again dancing to the bond market’s drumbeat. The 4.5% level on the 10-year remains the tripwire every equity bull needs to watch. Higher yields do not usually arrive in a vacuum. They tend to carry inflation concern, tighter financial conditions, and a valuation haircut for anything priced on distant cash flows. In other words, the bond market is no longer background music. It is the conductor, and right now it is tapping the baton just loudly enough to make the equity orchestra nervous.

The hidden story is that inflation pressure may be reappearing in places the market is not fully watching. The 10-year has bounced from key support, economic surprises are ripping higher, and the old inflation dragons are beginning to stir again. At the same time, AI-driven chipflation may be creating a new source of price pressure that traditional inflation measures barely capture. This is the part of the story that could matter most. If the AI boom is not just lifting equity multiples but also lifting memory prices, infrastructure costs, data centre inputs, and producer price pressure, then the market’s favourite growth story starts feeding the very rate pressure that threatens its valuation.

That is the circular trap. AI has been the market’s escape hatch from the old macro cycle, the glittering tunnel through which investors believed they could outrun the Fed, oil, politics, and the business cycle itself. But if AI capex becomes inflationary at the margin, the escape hatch turns into another pressure valve. The trade that was supposed to float above the macro swamp may end up dragging the Fed deeper into it. My view is that this is where the next market debate lives: not whether AI is transformative, but whether the market has priced transformation as if capital were still free.

The regional damage reinforces the point. Korea’s KOSPI traded near lows overnight, down almost 17% from last Wednesday’s highs, because the countries most tightly wired into the AI hardware chain are the ones most exposed when investors start questioning the price paid for that growth. Taiwan, Korea, Japan, US semis, memory names, and the hyperscaler supply chain all sit close to the blast zone when the AI trade becomes less cathedral and more crowded cinema. That does not mean the structural story has failed. It means the market is starting to distinguish between a secular theme and a one-way positioning machine.

The old saying is that markets do not bottom on Fridays. Like most old market sayings, it is not always true, but it exists because liquidation often leaves footprints. Friday selling, especially when concentrated in leadership, rarely disappears just because Monday opens green. A relief rally was always likely after a violent flush, a weekend of calming bank desk notes, and some de-escalation in oil. But relief is not repair. The Nasdaq remains materially below Thursday’s close, and the S&P 500’s late-day fade suggests the market is not ready to declare the wound closed. In market terms, Monday stitched the cut. It did not prove there was no internal bleeding.

My view is that Monday was a reprieve, not a resolution. The oil market backed away from the cliff, but the rate market is still walking across a frozen lake in spring. Equities can live with geopolitical risk if crude does not detonate. They can live with AI froth if yields remain contained. They can even live with a hot economy if inflation behaves. What they cannot easily live with is all three pressure points pulsing at once: higher oil risk, sticky inflation, and a Fed that may have to sound less like a future rate cutter and more like a reluctant fire inspector walking through a building full of dry timber.

That leaves the market in a dangerous but tradable zone. If CPI cools, yields back off, and oil stays below the panic threshold, Friday may look like a classic flush in crowded AI risk, and Monday may prove to be the first step in rebuilding the tape. But if CPI comes in hot and the 10-year yield starts pressing back toward 4.5%, the bounce will look less like bargain hunting and more like a reflexive squeeze in a market that has not finished repricing the cost of money.

The market dodged the oil shock on Monday. It has not escaped the rate trap. In this tape, the danger is no longer the headline you can see. It is the pressure plate hiding beneath the valuation floorboards.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.