The Makings of a Debt Crisis: Corporate Debt Soars While Credit Ratings Fall

Two big news items in the last 24 hours have grabbed my attention.

The first is Congress’s approving a bill to roll back the Dodd-Frank Act. If this passes, smaller financial institutions will find relief from the strict rules that have applied to Wall Street banks since after the 2008 crisis.

This is sheer idiocy! It will not end well.

The second is the U.S. corporate debt is suffering one of its worst sell-offs since 2000. This is another disaster in the making.

U.S. corporate debt has risen from $40 trillion to $70 trillion since the top of the last bubble in 2007. That’s 63% in 10 years. It’s risen 135% since 2000!

Only government debt has risen faster, from $35 to $64 trillion, or 83%.

China is the worst by far, going from $6 to $36 trillion or a 500% increase!

Of course, many of these bonds are simply financial engineering to buy back stock to increase earnings per share. Uber-low long-term interest rates thanks to QE have allowed companies to do this cheaply.

The problem is these long-term rates have been rising since just July 2016. They’ve gone from 1.38% to 3.10%. That’s an increase of 172 basis points in the risk-free 10-year Treasury bond. That naturally reverberates up through the risk spectrum from investment grade corporate bonds to junk bonds.

You see, here’s the thing…

Governments have artificially pushed down bond yields for so long that companies have embraced speculation rather than productive investment (i.e. they’re not spending money on productive assets that will serve them and the economy well in the long-term).

This mentality only creates financial asset bubbles that burst.

When companies buy back their own shares at historically high valuations, they’re speculating, just like an investor or hedge fund.

When stocks crash ahead, shareholders will demand to know why these corporations used the money they will need to survive the crisis to speculate in their own stock… at the highest prices in history!

Well, as the numbers are now showing, this corporate bond bubble is starting to burst, and of course that will ultimately hit junk bonds the worst… then stocks and real estate.

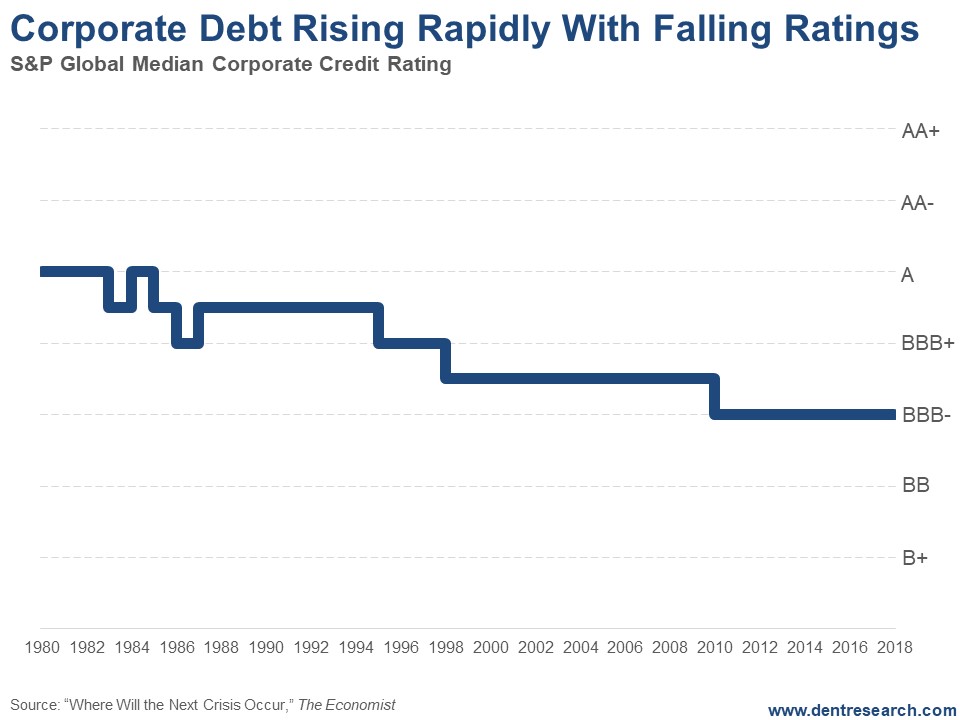

But the real story here is that we’ve been in this bond bubble since 1981. And the quality of this corporate debt has been falling for nearly 40 years now. QE has only accelerated the decline.

We’re now at the point where the median corporate bond rating is borderline junk…

Median ratings started at A in the early 1980s when this unprecedented boom began. Since then, it has steadily fallen to BBB-. The next step down is junk bonds.

And this is a global phenomenon. It’s not just isolated to U.S. corporations.

Forty-eight percent of investment grade bonds are rated BBB, just one notch above the median in this chart. The net leverage ratio for such BBB issuers has gone up from 1.7 in 2000 to 2.9 today.

All of this means that investors are getting rewarded less and less for lower quality bonds. Yet such investors are less worried than ever, as shown by a 40% drop in the cost of insuring such bonds (through credit default swaps) in the last two years. Continued tightening by the fed only makes this worse.

This is a bond crash and debt crisis in the making and could end up being the biggest trigger for the stock crash. And it’s already in motion!

Author

Harry S. Dent, MBA

Dent Research

Harry S. Dent Jr. studied economics in college in the ’70s, but found it vague and inconclusive. He became so disillusioned by the state of his chosen profession that he turned his back on it.