The German debt brake: The merits and limitations of fiscal rules

The recent decision of the German Federal Constitutional Court has fueled the debate on the debt brake, which imposes strict limits in terms of budget deficit. At the risk of oversimplifying, the question is whether fiscal policy should be based on an iron rule or a golden rule. The debt brake imposes fiscal discipline on future governments, which enhances fiscal policy credibility. However, its focus on the budget deficit implies that under realistic assumptions, public debt in percent of GDP will decline significantly. Proponents of the golden rule argue that, given the huge investment needs -green and digital transition, public support to innovation, etc.-, any leeway should be used to finance these investments, thereby enhancing structural growth and/or accelerating the green transition. The outcome of this debate also matters for Europe given Germany’s economic weight.

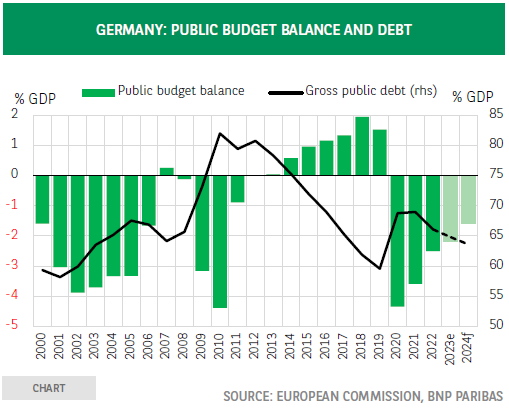

In 2013 the German government launched Industrie 4.0, a program focusing on the intelligent networking of machines and processes for industry with the help of information and communication technology1. In a recent article, Der Spiegel has extended the use of ‘x.0’ to the domain of public finances by referring to Schuldenbremse 2.02. The debt brake -which applies to the central government- was introduced in 2009 following the global financial crisis in order to bring public finances back under control (chart). It is enshrined in Germany’s Basic Law and its reform or abolition would require a constitutionally amended two-thirds majority in the Bundestag. It has a structural component, which limits net borrowing -i.e. adjusting for financial asset acquisitions and cyclical effects- to 0.35% of GDP per year and a cyclical component. According to the latter, the deficit can be bigger during a downturn, but this must be compensated when the economy improves again. Finally, there is an escape clause, “which allows the Bundestag to suspend the debt brake by a simple majority in the event of a natural disaster or other extraordinary emergency situations beyond the control of the state3.” It was the interpretation of this escape clause that on 15 November last year put the German government in a difficult position because the Federal Constitutional Court declared that “credit authorizations established within the scope of the exception clause can only be used until the end of the relevant financial year and then expire without replacement.” This blocked the Federal Government’s plan to use credit authorizations obtained in previous years but not yet used, to finance spending in the upcoming years because these authorizations had been declared void4. This forced it to reduce expenditures with EUR 17 bn to bring the 2024 budget back within the limit set by the debt break.

These developments fueled the debate about the need to update the debt brake. A survey of economics professors by the Ifo Institute and the FAZ showed that 44% want to keep it but reform it, 6% want to abolish but 48% want to retain it in its current form whereas 2% don’t know6. Those in favour of change consider it is necessary given the huge investment needs for infrastructure and the ecological transition whereas those arguing for the status quo see the current debt brake as essential for budgetary discipline and debt sustainability.

The Sachverständigenrat - German Council of Economic Experts (GCEE)- recently argued for a pragmatic reform, which would increase the flexibility of fiscal policy without putting debt sustainability at risk7. Firstly, after the application of the exception clause, bringing the structural deficit back to the regular limit could be spread over several years. Secondly, the annual structural deficit limit would depend on the debt level. If the latter is below a certain threshold, a higher structural deficit would be permitted. Finally, the experts propose methodological improvements in the estimation of potential output. This matters for the calculation of the structural deficit. German Finance Minister Christian Lindner has proposed a reform of the debt brake to enhance fiscal policy flexibility, but this should remain neutral in terms of debt dynamics. “Additional leeway in times of economic downturn would be balanced by stricter criteria in times of economic upturn.” However, he is against exempting investments in climate protection from the spending restrictions8.

At the current juncture, the debate in Germany boils down, to a large degree, to the question whether fiscal policy should be based on an iron rule or a golden rule. In case of the former, strict limits are set and by enshrining them in the Basic Law, they impose fiscal discipline on future governments, whatever their composition.

In terms of credibility, this has huge benefits considering that in the absence of such an iron rule, a commitment of fiscal discipline of the current government is not binding for future governments. Proponents of the golden rule argue that given the huge investment needs -green and digital transition, public support to innovation, etc.-, any leeway should be used to that end9. The GCEE has noted that the debt brake is more restrictive than the European fiscal rules. Moreover, its focus on the budget deficit implies that under realistic assumptions, public debt in percent of GDP will decline. Based on various simulations, the GCEE concludes that “as a median result, the debt-to-GDP ratio falls below 60 % of GDP by 2031 and to just under 42 % of GDP by 2070. In the long term, it converges towards around 30 % of GDP according to the simulation.” Aiming for stabilization at a still low but higher level than these longer-term projections -which would require a change to the debt brake- would create leeway to finance investments that would enhance structural growth and/or accelerate the green transition10. The outcome of this debate also matters for Europe given Germany’s economic weight.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.