The focus is on today’s European session

With US markets closed for the Thanksgiving holiday, the focus is on today's European session as markets continue to track this reflation/reopening trade to see whether it's got further to run. We've seen the second-largest 3-week inflow into value on record - Dec 2019 was the biggest, but didn't pan out too well. At the open, the main bourses lack any real direction and were treading water in the first hour. They may not offer much movement without the steer from Wall Street – usually Thanksgiving is a good excuse to hit the pub early for City traders. The FTSE 100 opened above 6,400 after yesterday's weaker session but struggled to find buyers above this level and quickly turned lower. Ex-dividend factors account for 5.5pts. The FTSE 100 has massively underperformed global equities, and has the best 2021 expected dividend yield (4%) of all major stock markets: it ought to be due to catch up if you buy into the reopening trade vis-à-vis energy, financials and value.

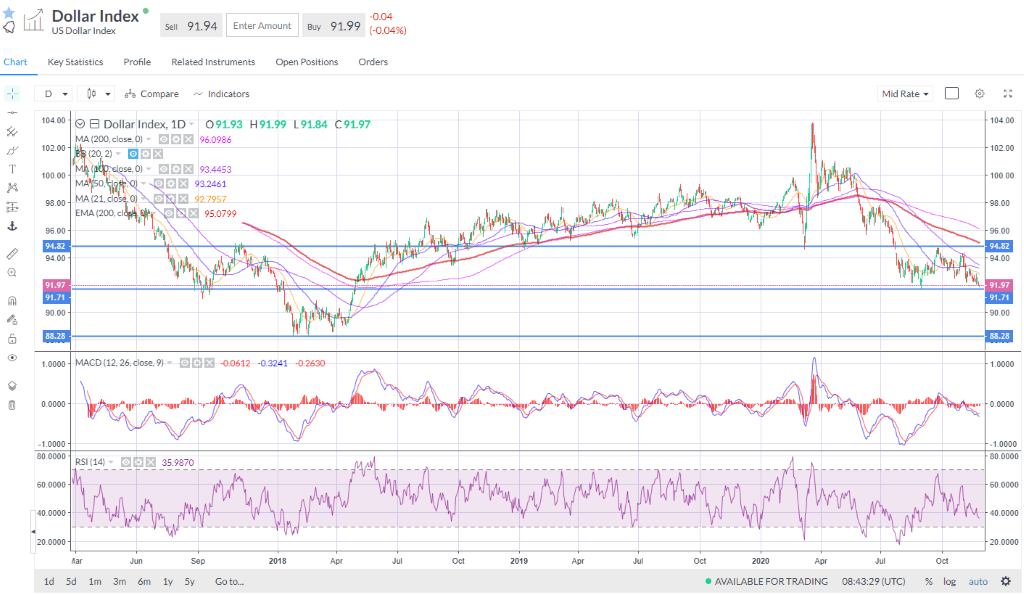

Yesterday, the Nasdaq rose, and the S&P 500 and small cap Russell 2000 fell as the rotation stalled. Tesla shares rose again to fresh record highs, climbing over 3% to $574 and come close to the market cap of Berkshire Hathaway. US 10-year Treasury yields ticked higher to 0.886%. The dollar is weaker with DXY under 92 and facing the key horizontal support at 91.70, the Sep low. Not a lot of support under that before the 2018 lows at 88. EURUSD is approaching the line in the sand at 1.20 as it trades at 1.1920 this morning. The worsening pandemic in the US - 16th consecutive day with fresh all-time high Covid hospitalisations show it's far from under control – may result in relative economic underperformance vs peers, albeit we should note that the main reason for economic contraction is lockdown, not the virus per se. Chiefly dollar weakness can be attributed to an improved global trade outlook post-Trump, negative real rates in the US and an improving global economic outlook should be a recipe for dollar weakness. Rising oil prices should lift inflation (in addition to other factors previously discussed) next year, furthering pushing real US rates negative. However, the dollar always surprises as the global reserve currency and a short squeeze cannot be written off.

Crunch time for USD as Apr 2018 lows approach.

AstraZeneca is facing growing scepticism over the way it reported the results of its vaccine trials. The company has since admitted that the more effective half-dose regimen was only given to participants because of mistake. Serendipitous it may have been, but the charge is that Astra has not been entirely forthcoming with the data. Moreover, the head of the US ‘Operation Warp Speed' programme, Moncef Slaoui, said yesterday that the more effective dose was only administered to people aged under 55. Worth noting that he used to work for Moderna until very recently. The criticism seems to be coming largely from across the pond, but shares have taken bit of a hit since Monday – it may be difficult for Astra to get emergency approval in the US. Pfizer and Moderna would not be too unhappy about that.

Minutes from the Federal Reserve's November meeting showed participants want to provide updated guidance on their bond buying "fairly soon", but they did not think they need to make any immediate adjustments. Some policymakers felt that lower- and middle-income households may soon run out of cash if there is no further fiscal stimulus. Looks as though the Fed, as expected, will try to step up if the fiscal side does not come through.

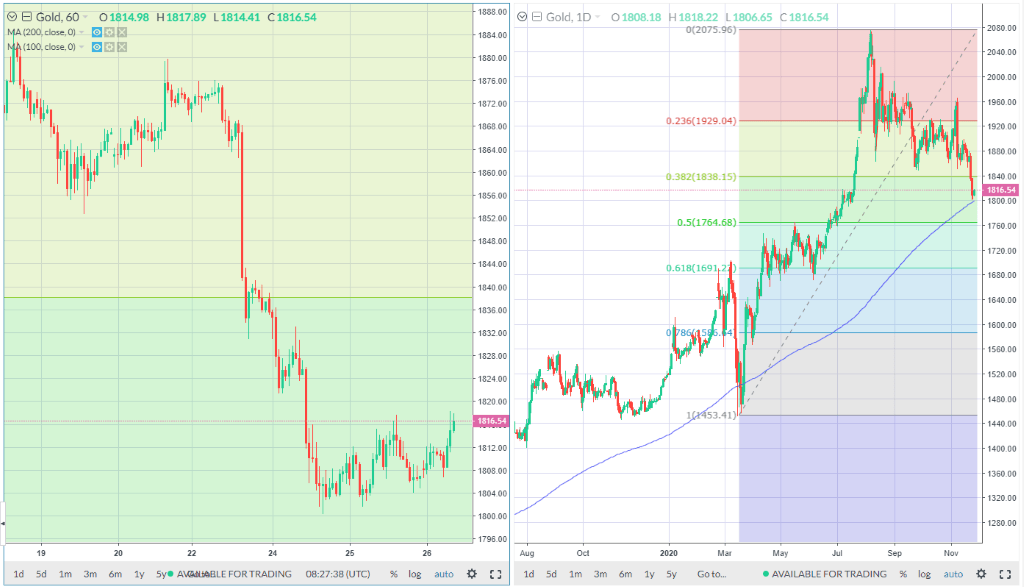

Gold appears to be making a base at $1,800 with the 200-day average offering the major support. On the hourly chart we see a push to $1,833-$1,838 area as being key for the bulls to regain the near-term momentum.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.