The Eurozone is exporting its savings, but is it investing them advantageously?

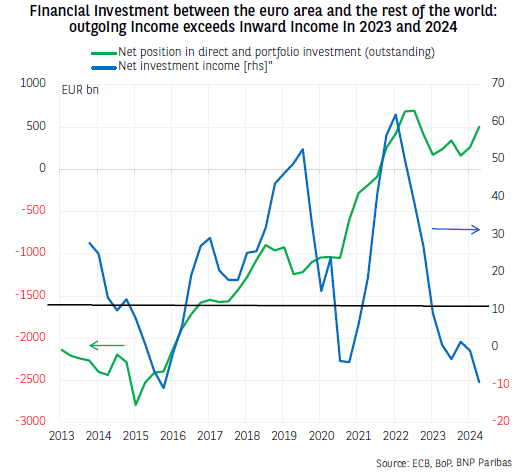

The eurozone’s net international investment position in terms of direct and portfolio investment recovered significantly between 2015 and 2022, becoming positive from 2021 onwards, meaning that the eurozone has become a net creditor to the rest of the world. However, the income it receives from these assets is lower than the income it pays to non-resident investors. What are the reasons for this?

The relative choices of savers and investors from outside the eurozone and non-resident investors within the eurozone have an impact on the flow of investment income into and out of the eurozone.

The change in the eurozone’s net international investment position is due to the recovery in the net balance of debt assets. Since 2019, eurozone investors have held more debt issued by non-residents than non-residents hold of eurozone issuers, and the gap has widened since then. Conversely, the net position in equities1 and fund units remains negative, and is moving in a horizontal tunnel: non-resident investors consistently hold more equities and fund units issued in the eurozone (including private equity) than eurozone investors hold outside the eurozone.2 This means that, structurally, European savers investing abroad have a lower risk appetite than non-resident savers investing in Europe.

Notwithstanding the relative stability of the net international investment position in terms of direct and portfolio investment since 2022, the balance of investment income has fallen sharply, from a year-to-date peak of +EUR 62 billion in the first quarter of 2022 to -EUR 9 billion in the second quarter of 2024.The balance has even become slightly negative in cumulative terms over the entire period (-EUR 1.8 billion).

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.