The ECB is staring at two different inflation stories

Two different inflation stories

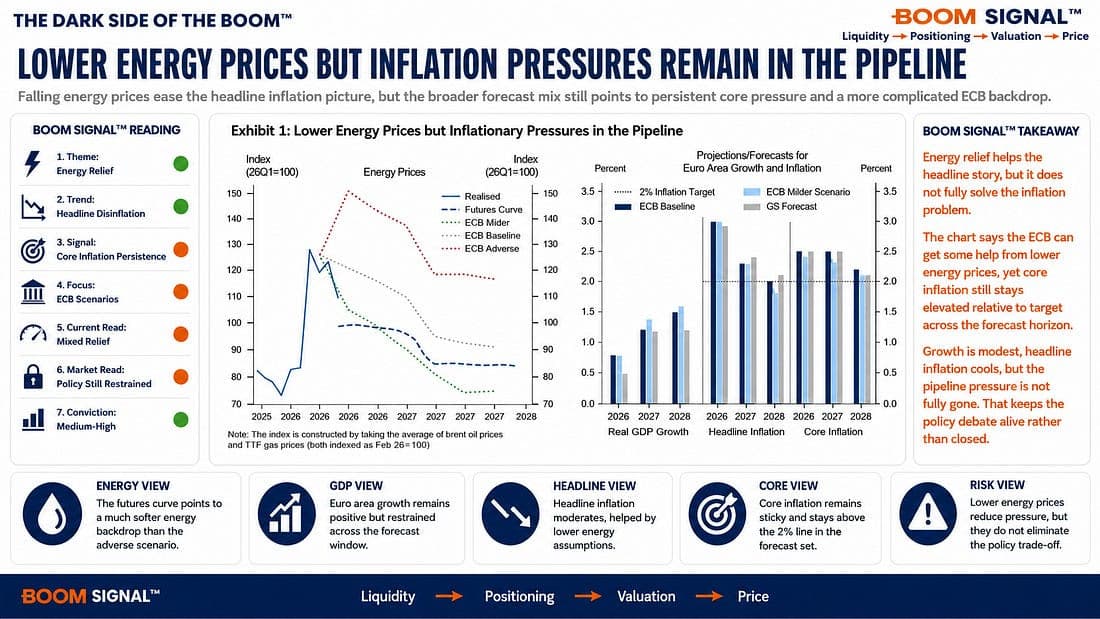

The European Central Bank is heading into Sintra with oil doing one thing and underlying inflation doing another. Energy prices have retreated sharply since the June meeting, taking some of the heat out of headline inflation and giving the doves a cleaner script. But beneath that more comfortable surface, core inflation remains the stubborn guest who has not taken the hint. Even under the ECB staff’s milder scenario, core inflation peaks near 2.6% and remains above the 2% target through 2028.

That is the problem for policymakers. Lower oil prices can make the inflation dashboard look calmer, but they do not necessarily extinguish the pipeline pressures coming from wages, services and still-firm domestic demand. The ECB may get relief on the front page of the inflation report, while the more important details continue to argue that the engine is running too hot.

One way to frame the decision is through a Taylor-rule lens: a mechanical policy benchmark that asks how far rates should move when expected growth runs above trend and inflation sits above target. It is not a forecast, and it is certainly not a substitute for central-bank judgement. Think of it as a Central Bank’s policy speed limit, calculated from where the economy and inflation are expected to be a year ahead.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.