The ECB is expected to hike this week, maybe the Fed would act in July?

Outlook

For Trump to call for both Iran and Israel to stop shooting is the clue to what happens next—Trump wants the ceasefire to go on, and on. We guess it’s untenable for the US to demand—at Iran’s demand—that Israel stop defending itself against the Iran proxy Hezbollah. This isn’t over and will most likely escalate.

Over the weekend, we wrote it was shocking to see standard old-fashioned macro data (US jobs) move the FX markets so much when we had become accustomed to seeing war news rule the roost. So far it’s a one-time thing but this week we need to watch for whether it has become the new normal and war events have to be Really Big to take center stage again. To be fair, traders dislike politics of all stripes and do their best to ignore them, so putting economics first is in keeping with long-standing convention.

You’d think that the robust job reports would lift up expectations of the Fed hiking soon-ish and putting the rate comparison with the eurozone (and others) closer to an even keel. The ECB is expected to hike this week, so golly, maybe the Fed would act in July?

But that is not what is happening. Bloomberg reports “Bond traders fully priced in a Federal Reserve interest-rate hike by the end of this year after US job growth topped all forecasts in May, spurring yields higher in the $31 trillion Treasuries market.

“Interest-rate swaps indicated traders expect a quarter-point increase in the US central bank’s target for the federal funds rate by the December policy meeting, with a roughly 60% chance of a move in October.”

October?

The bond vigilantes took yields way up on Friday, with the 2-year up 11 bp to 4.14%, the highest this year, and the 10-year 7 bp to 4.53%. Maybe you don’t need expectations of the Fed doing anything—the yield alone does the job. Or, as a BlackRock manager told Bloomberg, “’The question is: Will the Fed get out ahead of where markets are pricing, or are markets going to try to push the Fed. “So far, it’s the latter.’”

“That leaves policymakers, who will meet June 16-17 for the first time under the leadership of Chairman Kevin Warsh, ‘playing catchup.’”

Well, the Fed will have new data to chew on. CPI on Wednesday is expected to go to 4.2% y/y from 3.8%, the highest in three years, with core at 2.9% from 2.8%. We continue to say core is irrelevant by excluding oil and energy when the war is driving both up so much. We can expect to see the monthly annualized and the other usual tricks to alter the outcome, but the year-over-year is what most folks watch and will suffice. A reading of 4.2% can’t justify a hold or a dovish view. Similarly, PPI on Thursday is irrelevant.

We also get the ADP, existing homes sales, and on Friday, the U Mich consumer sentiment, including inflation expectations. This week brings the Bank of Canada (Wed), the ECB (Thursday) and UK GDP (Fri), which will influence expectations for the BoE next week.

Forecast

Restoring the ceasefire on Iran’s terms is a stopgap and not a solution. Isreal is not giving up its right to defend itself. We must expect the next war move to be Hezbollah or Iran assaulting Israel again and Isreal fighting back. In the meanwhile, it would be wonderful for everyone if Trump were to demand that in return for muzzling Israel, Iran agrees to re-open the Strait and remove mines. It’s not clear Trump has the brains or the guts to do that, even though it would meet one of this other objectives, driving the oil price and the dollar down.

That leaves us with the inflation/Fed story, and specifically whether Mr. Warsh returns to his hawkish stance of yesteryear. We say he does—there is no viable alternative. But we must also expect some Trump-ish distractions from the main message, including perhaps a change in the Fed’s balance sheet or a change in the whole forward-guidance apparatus.

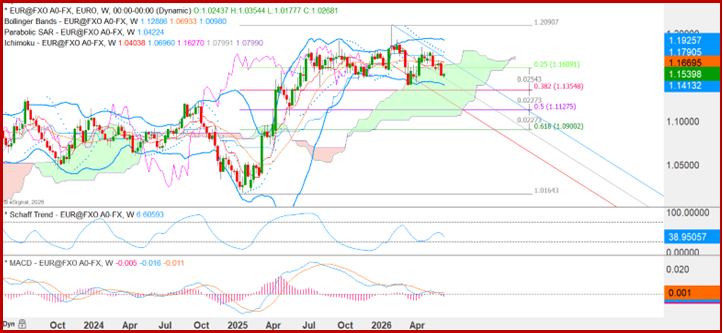

The dollar resurgence, mostly on yields, is on-going. See the chart of the euro in the weekly format. This puts the 50% retracement of the euro’s gain at 1.1128, about the midpoint of the euro’s rise in the week of April 7th.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat