The conventional big news today is the Fed minutes

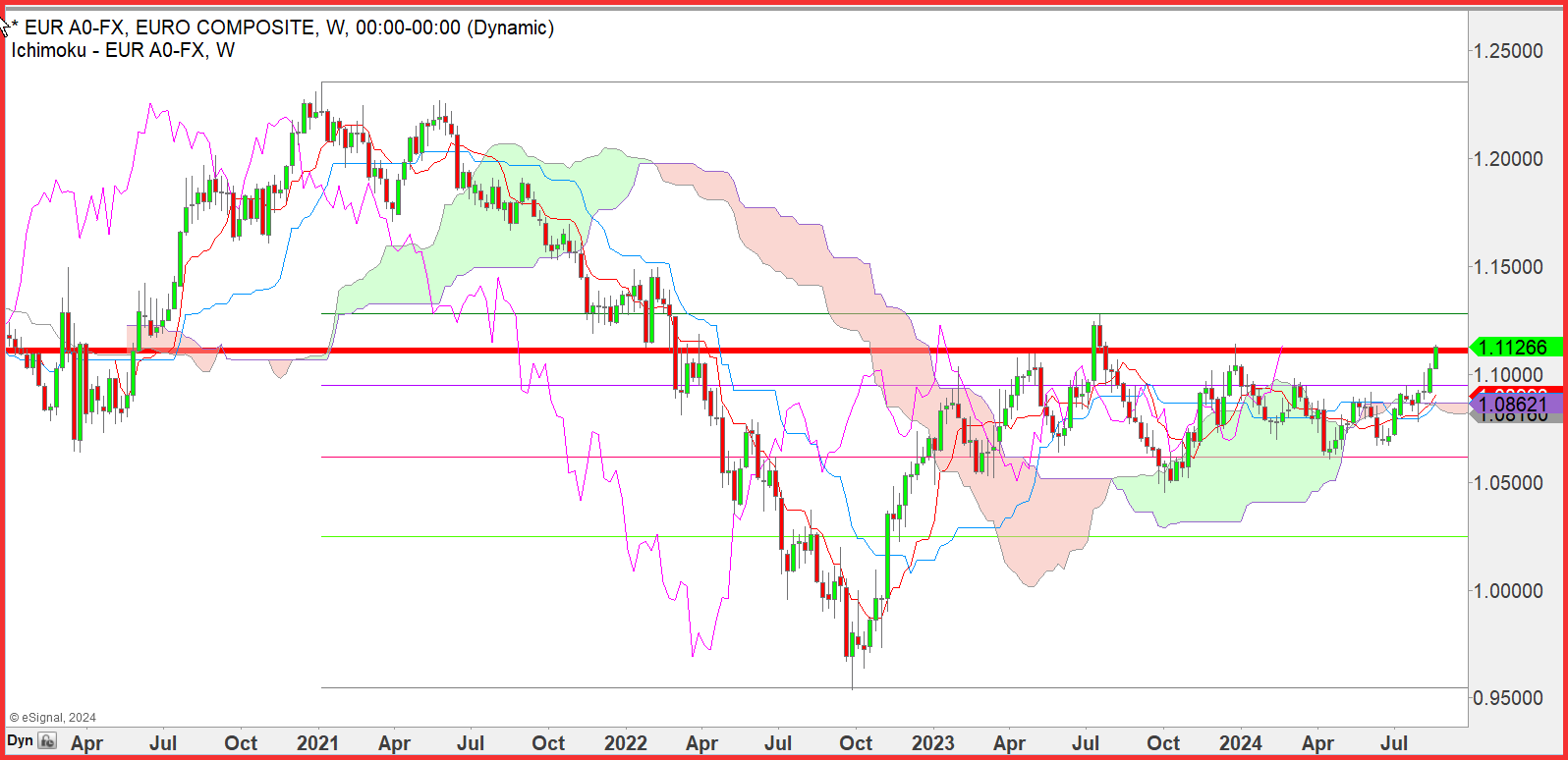

The euro rose strongly yesterday and nearly matched the previous highest high at 1.1140 from Dec 27 last year. Today’s pullback is normal as a retreat from a “historic” number like that.

Historically, the euro is seriously overbought. One analyst notes the close has been over 1.1100 a mere nine times in the past two years. The euro has closed above 1.1130 only five times in the last two years. “We are in rarified air.”

Thanks to Brent Donnelly. And we agree. Seldom-seen new highs need new players to come in at risky levels. They usually see the risk and stay away. Then the players who took the high levels get into a frenzy of selling to reduce losses, and the resulting drop looks like a crash.

The red line on the chart lies at 1.1100. The majority of prices fall between the 38%-50% retracement levels of the big move from end-2020 to Oct 2022, or 1.0615 to 1.0946.

The macro data support the idea of the US outperforming the eurozone and especially Germany. The US has growth; Germany is on the cusp of recession. US inflation is falling; eurozone inflation is flat and even rising in some places and some categories. And so on.

Outlook

The conventional big news today is the Fed minutes, expected to sound dovish. Yesterday Atlanta Fed Pres Bostic said "Evidence of accelerating weakness in labor markets may warrant a more rapid move, either in terms of the increments of movement or the speed at which we try to get back." Zowie.

We also get the Atlanta Fed business inflation expectations, but attention has turned from inflation to employment so it may go unnoticed.

A big risk to our debunking of the endless rate cut narrative could well be the BLS revision to payrolls later today (with the final due later next Feb). Eve the FT has caught this fever and has a headline on the front page: “Cooling US jobs market looms over central bankers at Jackson Hole.”

The Bloomberg report yesterday lays it all out: “US job growth in the year through March was likely far less robust than initially estimated, which risks fueling concerns that the Federal Reserve is falling further behind the curve to lower interest rates.”

The big banks have forecasts. Goldman Sachs sees a cut of some 50,000 per month for a total of 600,000 but as much as one million. JPMorgan Chase has 360,000.

“… a downward revision to employment of more than 501,000 would be the largest in 15 years and suggest the labor market has been cooling for longer — and perhaps more so — than originally thought.” See the table showing previous years’ revisions.

“As it stands now, the BLS data show the economy added 2.9 million jobs in the 12 months through March 2024, or an average of 242,000 per month. Even if the total revision is as high as a million, monthly job gains would average around 158,000 — still a healthy pace of hiring but a moderation from the post-pandemic peak.”

Will a fat downward revision affect what Mr. Powell says at Jackson Hole? Powell has admitted the Fed is looking more closely at the employment data. Ah, but employment data covers a multitude. See the list from Trading Economics. The jobs report is hardly the only data that needs review. And not to be a broken record, the jobs report is not all that good even after revision, which relies on state unemployment claims, among other iffy factors. There are plenty of states whose data is not what you’d call well-managed.

Another argument against taking the revision too seriously is that revisions end at March, when it was the lousy July data that sent markets into hysteria.

That doesn’t mean a one-time shot of (say) a million fewer jobs will not goad the rate-cut-hopers into a frenzy of betting on lower rates and a lower dollar. Sentiment is always based on expectations of the next hand, so to speak. If the next hand delivers a king, you are going to expect a royal flush when maybe all you have is the high card.

Then there is the alternative—that the revision does not increase job losses by a big number but only a small one. Dollar sellers will have to cover really fast and we could get a spike.

Whatever the outcome, the trend-setters are at tremendous risk. Bloomberg reports “Bond traders are taking on a record amount of risk as they bet big on a Treasury market rally fueled by expectations the Federal Reserve will embark on its first interest-rate cut in more than four years.

“The number of leveraged positions in Treasury futures has risen to an all-time high ahead of the central bank’s annual economic symposium in Jackson Hole, Wyoming, which will commence on Thursday. At the event, Fed Chair Jerome Powell will speak and provide more insights into the central bank’s monetary policy path for the rest of this year.”

See the chart and be scared. Be really scared. “Open interest in futures, or the amount of risks taken by traders who can be long or short positions, peaked at a record of almost 23 million 10-year note futures equivalent, last week, CME Group Inc. data and Bloomberg analysis shows. That’s roughly $1.5 billion of risk per one basis point move in the underlying cash notes.”

Forecast: The FX market always overshoots. Conditions today are a classic case of that. It’s a little unusual that the bond market is also overreacting, but then again, this is not your grandpa’s bond market.

We can’t recall a time in the past few decades when a revision to the jobs report had any effect at all, let alone this giant effect. To be fair, we haven’t had this confluence of factors before, either, and we should never forget that even a few years later, the pandemic is still having economic effects, especially in conjunction with the demographic upheaval.

As for the labor market revision driving the Fed to extreme behavior (like a 50 bp cut at the Sept meeting), two points: first, the labor market is not as weak as the market seems to project. If it were, we would not have retail sales (and GDP) where they are.

Secondly, we can never forget the gray and black markets, which are basically tax avoidance but also avoidance of being counted at all by any government. This is a hobby horse for us. The un-reported work is vast, perhaps as much as 10% of the economy and certainly higher as the years go by and trust in government falls even further. We could cite bitcoin and other crypto as a symptom of distrust of government. In any case, the revision does not cover the multitude of other labor market factors, and we suspect some heavy bettors will be crying in their beer tomorrow.

We are getting set up for a sucker punch. The revision may generate spikes but nothing lasting. Watch the expectation of 50 bp in Sept continue to fall back. Also watch for some retreat in expectations of Mr. Powell sounding like Mr. Bostic—it’s not his style. The Fed never, ever signals a huge amount of impending rate changes. It’s coy about a single rate change up to the last minute. We may indeed get a series of cuts at every upcoming meeting, but it’s foolish to expect such a thing in the face of data-dependency and traditionally careful, cautious “transparency.” Besides, for Mr. Powell to affirm a cut at every upcoming meeting would be the same as admitting the Fed had over-tightened, and admitting mistakes is not in the Fed playbook, either.

Bottom line, while another dollar dip is all too likely, it is now vastly oversold and likely to stage a big and fast recovery as these developments take shape. Markets may be slow to change their minds, but once they do, the effects occur at lightning speed.

Political Tidbit: As of yesterday, PredictIt had the implied probability that Trump wins the election down to 46% from 69% in July (before the Biden step-down). The Silver Bulletin has Harris at 47.0% and Trump at 44.5%. A little weird: the Dems are ahead in each of the nine swing states, even though the Republicans picked up a few points in some of them.

A hidden weapon in Harris’ possession may turn out to be a winner—recruiting and embracing social media influencers—to get the youth vote. Trump was always going to lose the youth vote, anyway, but the difference between youth participation in the 2016 election and this one could well be huge. “Youth” is ages 18-29. In 2016, Trump got only 37% of the youth vote. (He gets a majority in ages 45-65 and 65+.)

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat