The chips are up

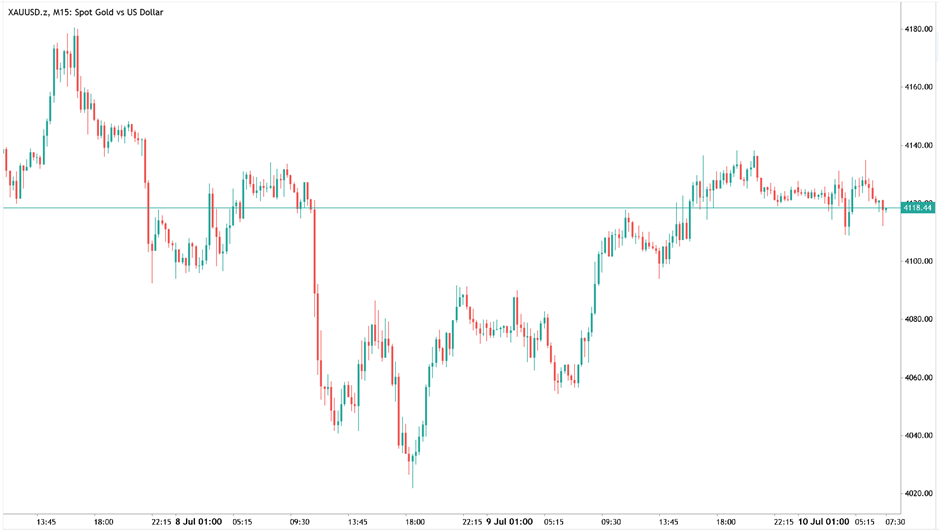

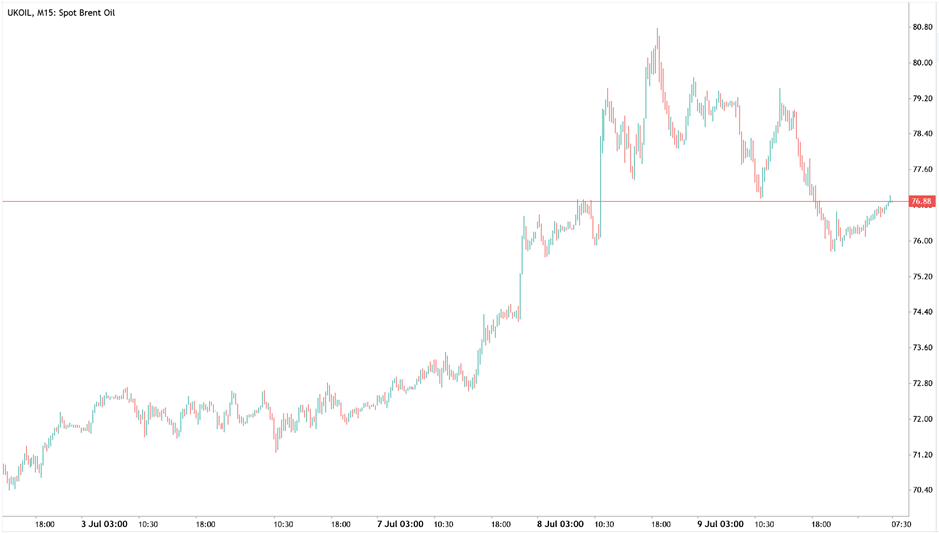

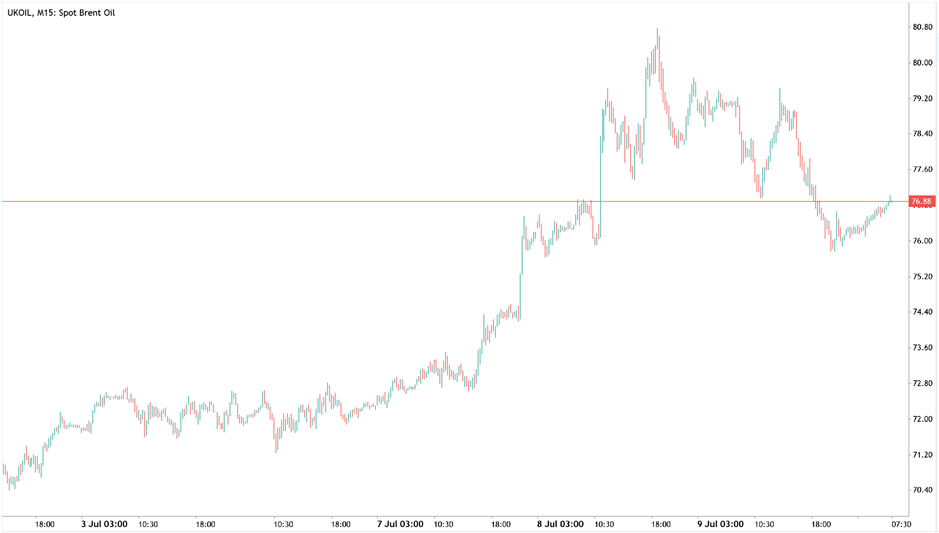

It has been a week of two halves for markets. Renewed military exchanges between the US and Iran brought energy prices back into focus coming out of the weekend, and in turn re-sparked fears of higher inflation for longer. This perceived danger saw the USD rally, oil spike, and tech stocks slide. But over the ensuing trading sessions, US equity markets have largely shrugged off the breakdown of negotiations in the Middle East. Oil has not been as resilient, ending the week up around 7% as traffic in the Strait of Hormuz slows anew. SK Hynix has broken records with its US listing, as the chip sector in general bounces impressively. Gold (XAUUSD)started the week strongly before sliding back towards the $4,000 handle, stabilising somewhat since around $4,100. Today we have seen the yen jump, but not for the reason we have been awaiting.

Re-escalation and de-escalation

Despite the President's best diplomatic efforts, the USMNT was knocked out of its home World Cup by Belgium early in the week. It may seem flippant to mention, but just as the real ceasefire commenced in time for the opening ceremonies, attacks in Iran resumed not long after Balogun and co.'s exit from the tournament. Energy markets spiked as a result, Brent crude (UKOIL) swiftly up to almost $80, before pulling back to stabilise somewhat around the $75 mark. The resumption of the conflict also brought rate hike expectations swiftly back into focus. Market expectations are now that the next increase from the Fed will come in October, rather than December. This adjustment pressured equity markets and supported the US dollar. Market participants on the whole though still view DJT's predilection for strong and stable equity and bond prices as a reassuring if historically unorthodox force to be relied upon. Thus reactions are far more measured than what we saw at the start of the conflict, now into its fifth month. Indeed the US dollar index (DXY) has now fallen to a three week low as signs of de-escalation flow through once again.

SK Hynix - largest launch ever

Despite pricing its US listing at a premium (~3%) to the Korean stock price, SK Hynix's sale of ADRs was oversubscribed by more than seven times. This confirmed it as the biggest ever share sale by a foreign company in the US, raising $26.5 billion in the process. The launch came as volatility in chip stocks hit its highest level since 2020. South Korea has emerged as one of the biggest winners of the AI boom, predominantly through the two largest memory makers worldwide in SK Hynix and Samsung. The government there this week reiterated its commitment to further bolstering the sector through investment in the AI ecosystem and related infrastructure. This rapid rise to global dominance has coincided with the launch of leveraged ETFs in the country, leading in combination to some extraordinary daily moves in domestic indices. The KOSPI this week triggered its sixth circuit breaker for the year, its 12th in history. It closed on Wednesday down over 20% from its peak, moving into official bear territory, but has gone a fair way to recovering in the days since. SK Hynix's stock will begin regular trading in the US next week, under the ticker SKHY.

Buy local

While certainly not the money market intervention that traders have been on high alert for, we have seen a notable poloicy shift in Japan today. Finance Minister Satsuki Katayama announced that the government will be encouraging "households, as well as pension funds including the GPIF, to increase their investment in Japanese financial assets". The Government Pension Investment Fund manages around $1.81 trillion in assets. Now that Japan has finally returned to a positive interest rate regime, the government has signalled that it wants its citizens to benefit from public investments in the tech sector in particular. Katayama's announcement had an immediate effect on markets: USDJPY off 0.5%, back from 40-year highs; and the Nikkei (JPN225) up 2%, continuing to grind higher on the back of recent strength. Naturally this reallocation domestically will likely flow on to offshore investors too, moving money managers worldwide to up their allocations to Japanese assets. But it is the relatively reliable and steady cohort of domestic investors that will much more significantly move the needle.

Next week

US CPI is expected at 0.1% month on month, vs 0.5% in May. It is the year on year figure that will be in the headlines however, after Chairman Warsh reiterated his intentions to bring inflation back closer to the official target of 2%. Later in the week we get US retail sales. China also releases its main economic marker in GDP, as well as retail sales and industrial production figures for June. The Bank of Canada will announce its rate decision on Wednesday, expected to hold steady at 2.25%.

US earnings season kicks off next week too. As always the big banks get us under way; among others Morgan Stanley (MS.US) and Goldman Sachs (GS.US) will release their quarterly results. Go well out there.

Author

Scott Redford

Fintrix Markets

Through his 14 years in the industry, Scott has managed risk for a number of the world's biggest brokers, including IG and Pepperstone.