The Case for Higher Interest Rates: (Still) The Fundamentals

In early January, we laid out the case for higher Treasury yields across the yield curve based on the macro fundamentals. Since then, markets have adjusted, but we believe yields still have some room to run this year.

The Evolution of the Fundamentals

Back on January 8, we released a piece making the case for higher U.S. Treasury yields across the curve in 2018.* Thus far, this call has proven correct, with the 10-year benchmark yield up 61 bps year to date and the 2-year note up 62 bps. More recently, however, long-term yields have stagnated, leading some to suggest that we have already reached the highs for 2018 (though these calls have faded somewhat in the past few days). We believe interest rates are still poised to move higher, albeit at a more gradual pace than seen early in Q1. Below, we examine three of the most fundamental determinants of Treasury yields: economic growth, inflation and the Fed.

Economic growth expectations began to take off last fall as the prospects for tax cuts in the United States brightened. As illustrated in the top chart, the consensus forecast for 2018 real GDP growth from the Blue Chip Survey rose every month between October 2017 and February 2018. Over the past couple months, however, growth expectations for the year have stagnated alongside the 10-year yield. Interestingly, this stagnation has occurred in tandem with falling forecasts for Q1 growth. Our Q1-2018 real GDP growth forecast, for instance, has fallen from 2.9 percent in January to 1.3 percent today.

If full-year growth expectations have remained steady but first quarter forecasts have fallen, real GDP growth forecasts for the remaining quarters of the year have implicitly risen. The drivers of this dynamic are varied: wintry weather late in the quarter, potential residual seasonality problems in the Q1 data, new individual tax withholding tables that did not go into effect until mid-February and a recent deal to raise federal government spending that will likely not see peak outlays until later this year. Regardless, we do not believe a weak Q1 GDP print would portend slowing growth/falling longterm yields the remainder of the year.

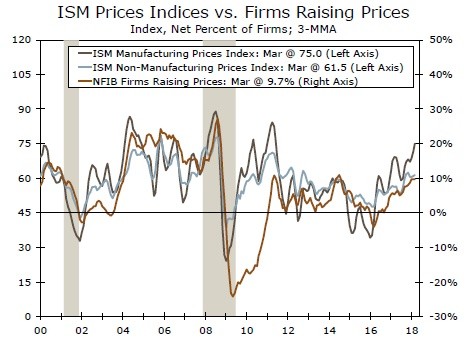

Inflation has also reversed course from its 2014-2016 slowdown, with core consumer price inflation above the Fed's 2 percent target and core inflation as measured by the PCE deflator not far behind. Market expectations have adjusted, with five-year breakevens rising 22 bps since the start of the year. A tightening labor market and rising costs for raw materials are pushing input costs higher, and survey-data suggest firms are starting to feel the pressure, signaling more inflation is building in the pipeline (middle chart).

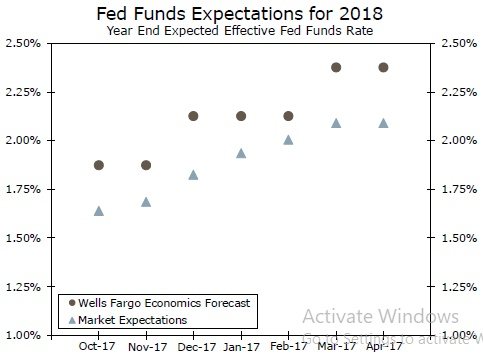

Market expectations for the Fed have risen alongside our own, but they remain shy of pricing in four rate hikes in 2018 (bottom chart). With real GDP accelerating in the coming quarters and core inflation reaching 2 percent around the same time, we believe the Fed will hike 3 more times this year. In our view, this confluence of faster growth, rising inflation and a steadily hiking Fed is a recipe for higher yields across the Treasury curve (our explicit forecasts can be found on page 2). In part II, we will examine our interest rate forecast in the context of supply and demand fundamentals.

Author

Wells Fargo Research Team

Wells Fargo