The Billionaire Tax: Too timid

10/27/2021

I’m having trouble getting my head around the idea of having a net worth of $1 billion. If only… Think of it. Written out, $1 billion is $1,000,000,000. If you had $1 billion of wealth and 50 years to live, and if you simply put that wealth in a safety deposit box, thereby forgoing the prospect of ever realizing any appreciation, you’d be able to spend $20 million each year for the rest of your life. Tough life. Given that level of wealth, the one conclusion I’m comfortable making is that billionaires can’t legitimately claim that they’ve been overtaxed. Quite the contrary.

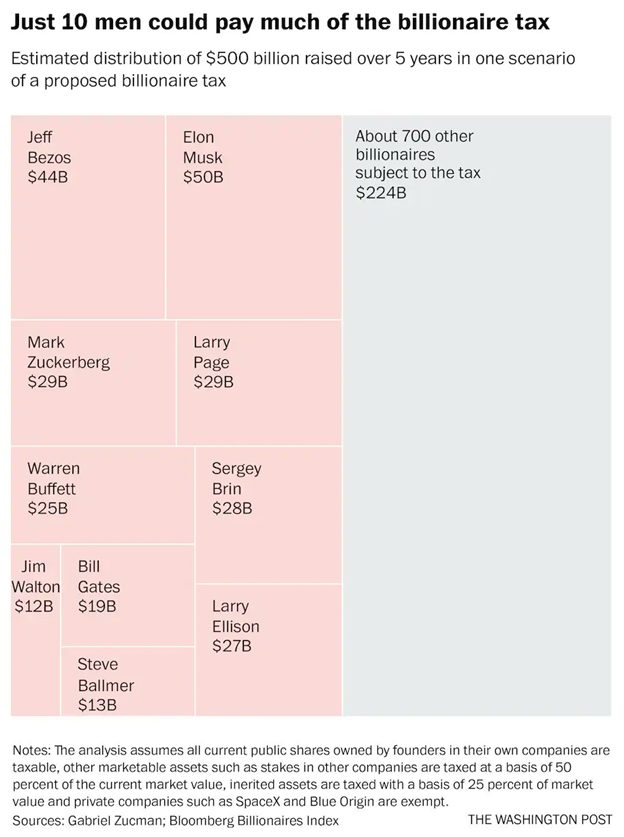

Some of those undertaxed individuals are listed on the table below, prepared by the Washington Post; and the amount of their wealth is nothing short of staggering.

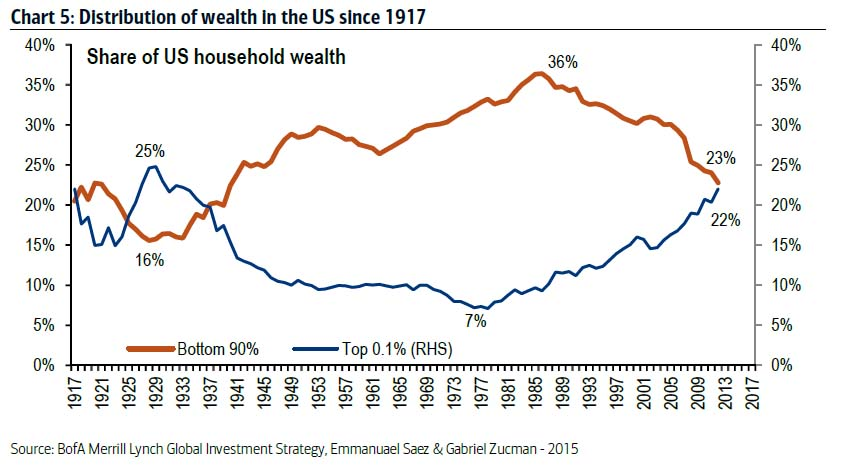

The billionaire tax currently being discussed is a nod toward addressing the dramatic economic divide that has evolved over the last 30 years or so (see the chart at the start of this post) and the sense that those at the top of the economic ladder have simply not paid a fair share to Federal coffers. Of course, this conclusion and any effort to address it will have its critics, but it seems that, subject to Senator Manchin overcoming his resistance, Congress may finally be ready to do something to collect higher taxes from this population.

My own preference would be to institute the kind of wealth tax the Senator Warren had proposed during the democratic primaries. Her plan called for a 2% tax on wealth in excess of $50 million, rising to 3% on wealth in excess of $1 billion. Seems reasonable to me, but it never got the kind of broad support needed to move it forward. Somehow, the idea of taxing unrealized capital gains for a targeted population of billionaires may be more politically palatable. Go figure.

My problem with the wealth tax and the current billionaire tax proposals is that they are both too timid. If we can accept the conclusion that the ultra-rich have been undertaxed — which, in my mind, is self-evident — the incremental effect of any new tax change should be more significant. With the wealth tax, couldn’t we make the respective tax rates a bit higher? As Elizabeth Warren has been fond of stating: taxpayers with wealth below $50 million would be unaffected, but if you had a wealth of $50,000,001, your tax liability on that incremental dollar above $50 million would be just two cents. Couldn’t we at least go for a nickel!? As for the billionaire tax, applying the new treatment only to billionaires is wholly arbitrary. Why not make the threshold somewhat lower — say, to the same $50 million that Elizabeth Warren suggested? It’s not like those in the $50 million-to-$1 billion bracket suffer from being overtaxed, while billionaires are not.

The point is that we can afford additional spending for the host of initiatives detailed in the Build Back Better bill. Any statement to the contrary is a canard — as is the claim that this legislation necessarily has to stick future generations with the costs. We don’t need to do that. Given the investment nature of so much of that legislation, some deficit spending should be acceptable; but I believe the bulk of these expenditures could, and should, be covered by the billionaire tax along with the other less controversial tax provisions in the bill (i.e., higher corporate rates as well as a surtax on the highest marginal tax rate).

The reluctance to adopt the proposed billionaire tax — or any other alternative provisions that would end up raising taxes from this echelon of taxpayers — boggles my mind. First of all, the concern that higher taxes for these taxpayers would diminish their capacity to be “job creators” or otherwise compromise whatever societal good these people are credited with providing is risible. More critically, failure to tap into the resource available to these taxpayers necessarily transfers the cost incidence of the Build Back Better program to others — either currently or in the future.

The ultra-rich can afford to bear the necessary incremental taxes without even breaking a sweat. Not so for those lower on the economic ladder. Admittedly, any new tax regulations with the intent of raising taxes on the rich will be fraught with practical difficulties; but the inequities that might arise in connection with these efforts pale in comparison to those of the current tax treatment.

Author

_Profile.jpg)

Ira Kawaller

Derivatives Litigation Services, LLC

Ira Kawaller is the principal and founder of Derivatives Litigation Services.