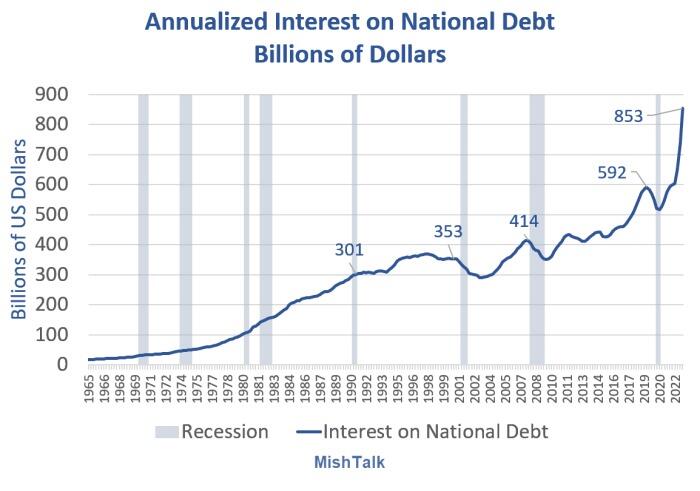

The annual interest rate payment on government debt is $850 billion and rising fast

At the current pace, interest on US government debt will soon hit one trillion dollars.

Note that interest on the national debt either stabilizes or drops during recession.

This happens because the Fed slashes interest rates and holds them too low, too long, creating the next bubble that it eventually must react to.

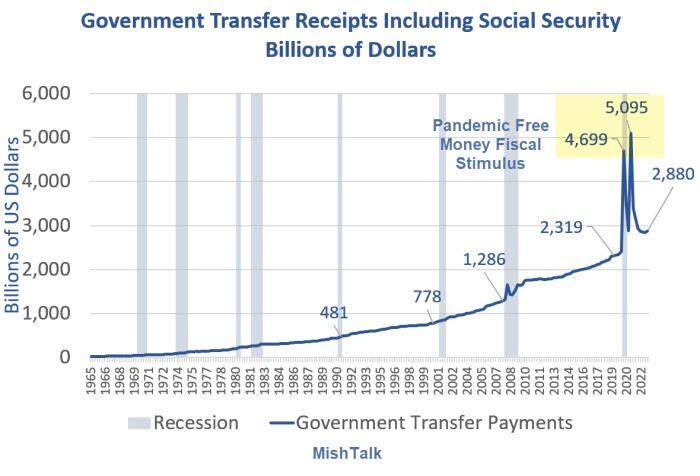

Social security and transfer payments

Transfer payment notes

- Transfer payments are redistributions of money for which there are no goods or services exchanged.

- Social Security, Medicare, Medicaid, and food stamps (now called SNAP) are examples of transfer payments.

- During recessions transfer payments tend to soar in recessions unlike interest on the national debt.

- Transfer payments are also influenced by retirements so demographics come into play. That $2.88 trillion is guaranteed to rise from here.

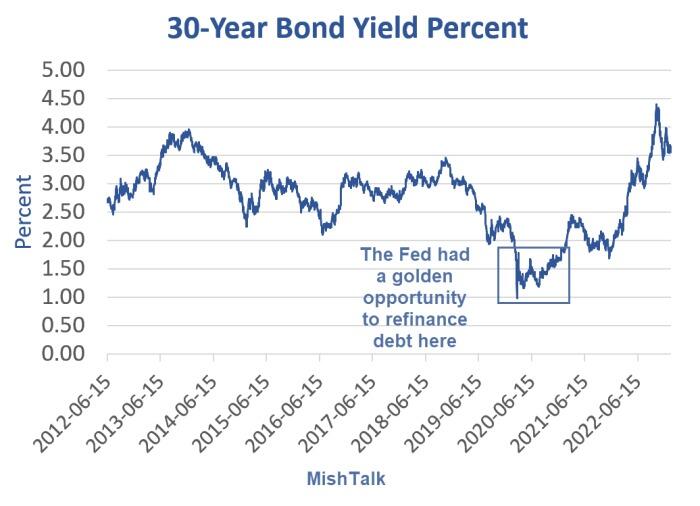

Your Fed at work

Between February of 2020 and February of 2021, the US Treasury had a golden opportunity to refinance long-term debt at 2.0 percent or under, most of the time well under 2.0 percent.

The 30-year bond yield bottomed at 0.99 percent. That was the secular low. The decades-long bond bull is over.

It's important to note the Treasury could not have refinanced at the lowest of those rates because the act of doing so would have tended to push yields up, but perhaps something around 2.0 percent on average may have been doable.

Now the Fed is promising to hold yields higher for longer. The three-month yield is currently 4.66 percent. Lovely.

Your tax Dollars at work

Before a dime is spent on roads, build back better, infrastructure, or anything else, the first $3.7 trillion (transfer payments plus interest on national debt) has already been spent.

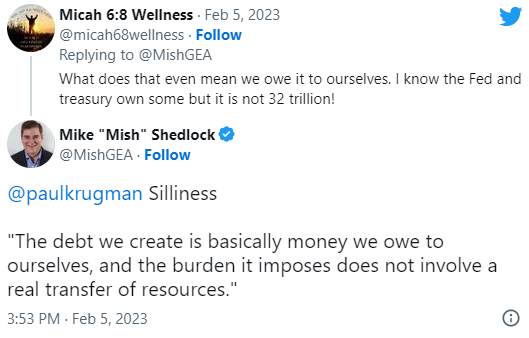

Not to worry, they say we owe this money to ourselves.

Yeah, right.

Correction: Between February of 2020 and February of 2021, the US Treasury had a golden opportunity to refinance long-term debt at 2.0 percent or under, most of the time well under 2.0 percent.

I previously said Fed instead of Treasury

A word about owing debt to ourselves.

Apparently debt does not matter because we owe it to ourselves. Ridiculous.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc

Mike “Mish” Shedlock is a registered investment advisor for SitkaPacific Capital Management.