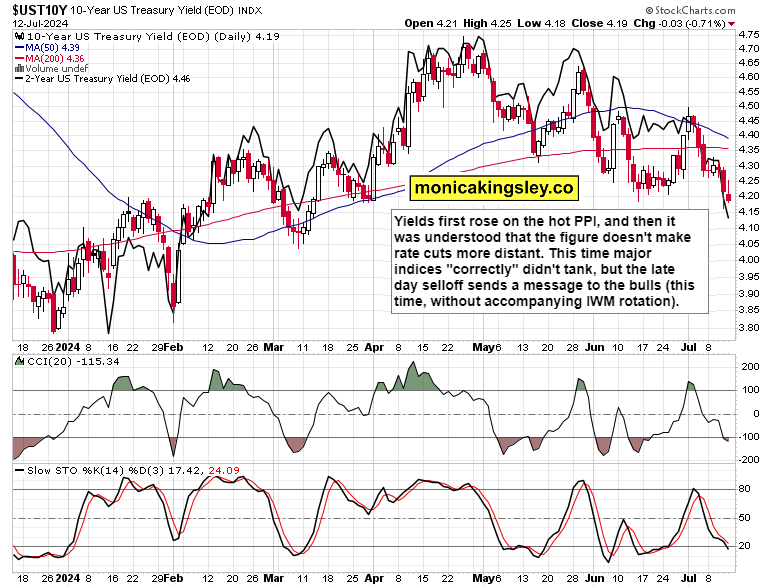

That fear of deflation

S&P 500 went nowhere till PPI – dumping on hot figure, and then the realization of its implications hit. Not deferring the rate cuts, the dip was dialed back fast, and buyers prevailed after the opening bell. It‘s simple – rising input costs while inability to pass them over to consumers ultimately means weakening profit margins and earnings (provided you see PPI stopping its ascent, how likely is that?). But first, weakening economy means rate cuts, and the odds of no Sep cut went duly down again since Thursday‘s 7% to 4% before reverting to 6% to finish the day.

These two charts that are determining the stock market path, shape of corrections and rotations.

The following analysis explains Friday‘s sectoral moves – did megacaps come back strongly enough? Is the Russell 2000 slowing down here, with reversal impending? As the earnings season is starting and select banks didn‘t fly (WFC, C, not even JPM – those loan loss provisions), what does it tell us about the consumer?

UoM consumer sentiment came in weak, and while stocks didn‘t waver, rate cut odds didn‘t increase. We‘re now to (already) a coin toss on whether we get three rate cuts this year – and that‘s before more weakness in the data coming weeks shows up. Please revisit prior Friday‘s super extensive article to understand deflation risks. Those retail sales Tuesday better be good, because consumer discretionaries have been mirroring Thursday‘s events internally as well.

Big picture down the road – if sales aren‘t good, earnings growth isn‘t good, what do companies do then?

Let‘s drop a few more clues – Thursday, USD, bonds and S&P 500 all simultaneously declined, which is very rare. Did Friday bring about different dynamics, and what did corporate bonds do?

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.