Surging Oil prices: A new concern for central banks

Life for the European Central Bank has become even more complicated as surging oil prices add to the trilemma of how to balance slowing economies, the delayed impact of the rate hikes so far and still too-high inflation.

Surging oil prices have become the new concern for central banks, aggravating the current trilemma: how to balance slowing economies, still too-high inflation and the delayed impact of unprecedented rate hikes. Interestingly, the answer to this conundrum differs between major central banks.

Looking ahead, the recent surge in oil prices will make things even more complicated as it will both worsen the economic slowdown but also push up inflation (or at least reduce the disinflationary trend). Balancing growth and inflation will become even harder and future interest rate decisions will not only be determined by these two variables but also by central banks’ credibility.

In this regard, central banks most concerned about their credibility and the longer-term impact on inflation expectations could end up continuing to hike interest rates. In the following article, we will mainly focus on the eurozone and the ECB.

Oil price rally likely to continue, but it's not sustainable in the longer run

Oil prices are currently up by more than 25% this quarter and briefly reached 95 USD/b last week. Our commodities analyst Warren Patterson expects oil prices to break above 100 USD/b in the near term as supply cuts by OPEC+ countries more than offset weaker demand due to the global economy’s slowdown.

However, he doesn’t see oil prices remaining above 100 USD/b for long as weaker demand and political pressure to increase supply should help to bring oil prices back to levels slightly above 90 USD/b.

Is this the second wave of inflation that we thought would never come?

A few weeks ago, we argued that the current inflation situation is not the same as the 1970s and that a second inflation wave looked highly unlikely. However, we also admitted that in the late 1970s, the second energy crisis was a main driver for the second inflation wave in many countries.

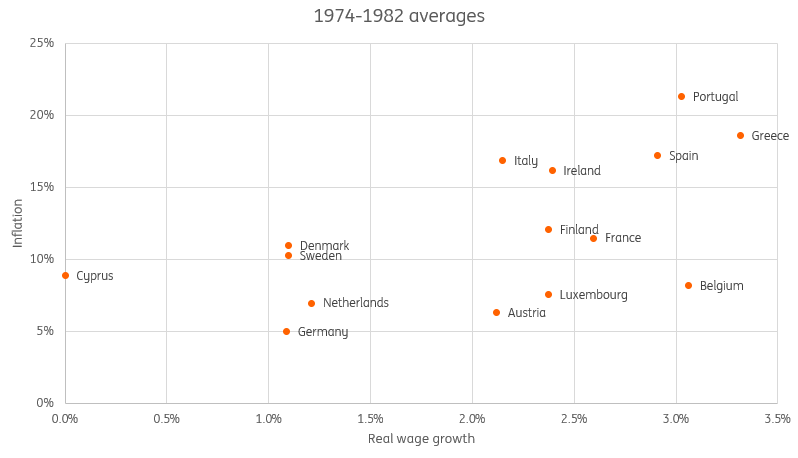

In the eurozone, there were three peak periods for inflation in the 1970s. The first was in 1974, when headline inflation was close to 14%; the second in 1977 with headline inflation above 10%, and then again in late 1979 and early 1980 with headline inflation back at double-digit levels.

Back then, real wage growth remained positive even during the spikes of the oil crises, which allowed inflation to remain above 7% for more than a decade (1972-84). Indeed, the countries that experienced higher real wage growth for the period also experienced the highest inflation over this period (see chart below).

The current surge in inflation is different in that real wage growth turned negative quickly, which has slowed consumer demand drastically. This makes the chances of a prolonged second spike in inflation much smaller. With inflation currently trending down and wage growth stabilising above 4%, real wage growth is set to soon turn positive again, but we wouldn’t expect it to erase the losses from the past two years.

At the same time, it is important to note that government support and employment growth have limited disposable income losses quite substantially.

In the 70s, countries with higher real wage growth also experienced higher inflation

Source: European Commission AMECO

Inflation is measured as the average annual growth in the national CPI and real wage growth as average annual growth in real compensation per employee, with private consumption as deflator.

How do current oil prices change our inflation forecast?

Despite this not being the 1970s, expectations of further disinflation will be impacted by higher oil prices. This could result in a slower decline of inflation to 2%. Given that our expectations for oil prices do include a drop in the first half of 2024 again, the effect on our own forecast is rather moderate. Plus, a smaller decline in energy prices has materialised this year compared to expectations (which impacts next year’s base effects).

Assuming oil prices stay at 95 USD/b for all of 2024, however, the headline figure would rise by 0.3pp next year, with a peak of the energy price contribution of 1ppt in the second quarter. At the same time, higher oil prices would probably further dent consumer confidence and spending, thereby contributing to the current disinflationary trend due to weaker demand.

Indeed, the big question is whether the higher oil price will once again result in broad-based second-round effects like we saw last year. A lot of drivers of core inflation are at this point still disinflationary, with manufacturing businesses still indicating that input costs are falling despite higher wages and energy prices. And as new orders are weakening, deflation for non-energy industrial goods is realistic towards the end of the year. For services, weaker demand is also contributing to slowing inflation despite higher wage costs, according to the September PMI. Our expectations are that core inflation will slow significantly from the 5.3% August reading towards the end of the year.

Still, if the labour market remains as tight as it is now and the economy bounces back a bit in early 2024, there is a risk that higher energy input costs would also put core inflation further above 2%. A lot depends on the strength of the economy in the months ahead, adding uncertainty for the ECB.

Pressure on the ECB to continue hiking

Prior to the pandemic, most central banks would probably have looked past surging oil prices. Some even considered rising oil prices to eventually be deflationary, undermining purchasing power and industrial competitiveness. However, we are no longer in the pre-pandemic era, but the era of returned inflation. The ECB has emphasised in recent months that doing too little is more costly than doing too much in terms of rates.

For the ECB, the recent staff projections were based on the technical assumption of an average oil price of 82 USD/b in 2024. If oil prices were to average 95 USD/b next year, this would probably push up the ECB’s inflation forecasts to 3.3% for 2024 (from 3.2%) and more importantly to 2.4% in 2025 (from 2.1%). As a result, the return to 2% would be delayed to 2026.

The delayed return to 2% would not be the only reason for the ECB to consider further rate hikes. Even though the ECB would still acknowledge the deflationary nature of a new oil price shock, the risk that this new oil price shock could lead to a de-anchoring of inflation expectations will definitely add to the ECB’s concerns, making not only an additional rate hike more likely, but also that they stay higher for longer.

Read the original analysis: Surging Oil prices: A new concern for central banks

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.