Strength for the Pound as sentiment on new government improves

The pound has gained significantly against most other major currencies in recent days as current Home Secretary Shabana Mahmood emerged as the frontrunner for next Chancellor and monthly GDP returned to growth. However, British inflation seems likely to have slowed down in June, which might put the brakes on possible tightening by the Bank of England (BoE). This article summarises recent news affecting the pound then looks briefly at the charts of GBPUSD and EURGBP.

A primary catalyst for the pound’s strength on Wednesday 15 July was the credible report that Shabana Mahmood is likely to be Andy Burnham’s choice for Chancellor. Previous expectations that Ed Miliband, nicknamed ‘Red Ed’, might take the job were negative for sentiment on the pound. Media reports overall in recent days have concentrated more on the likelihood of Mr Burnham’s government to stress continuity with Keir Starmer’s rather than a clear, sudden shift leftward. This is positive for stability in bond markets and for the pound.

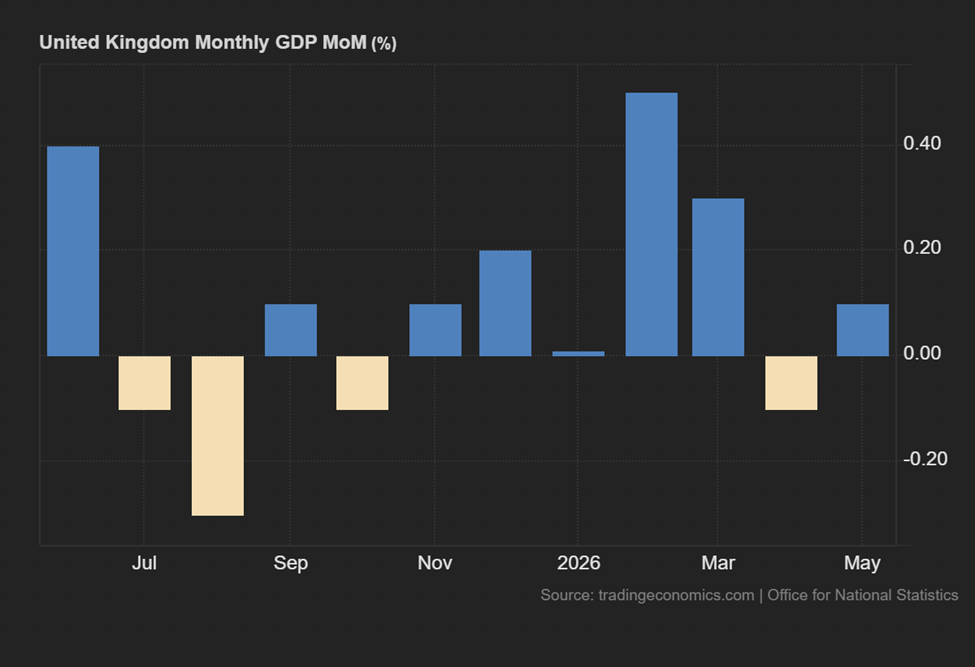

Meanwhile on Thursday 16 July monthly British GDP for May was moderately positive:

0.1% monthly growth isn’t fantastic but it does represent a recovery from April’s decline. Final British GDP for the first quarter as announced on 30 June met the consensus at 0.6%. While a significant upcoming recession seems very unlikely for now, the BoE still doesn’t have a lot of room to move with hiking rates.

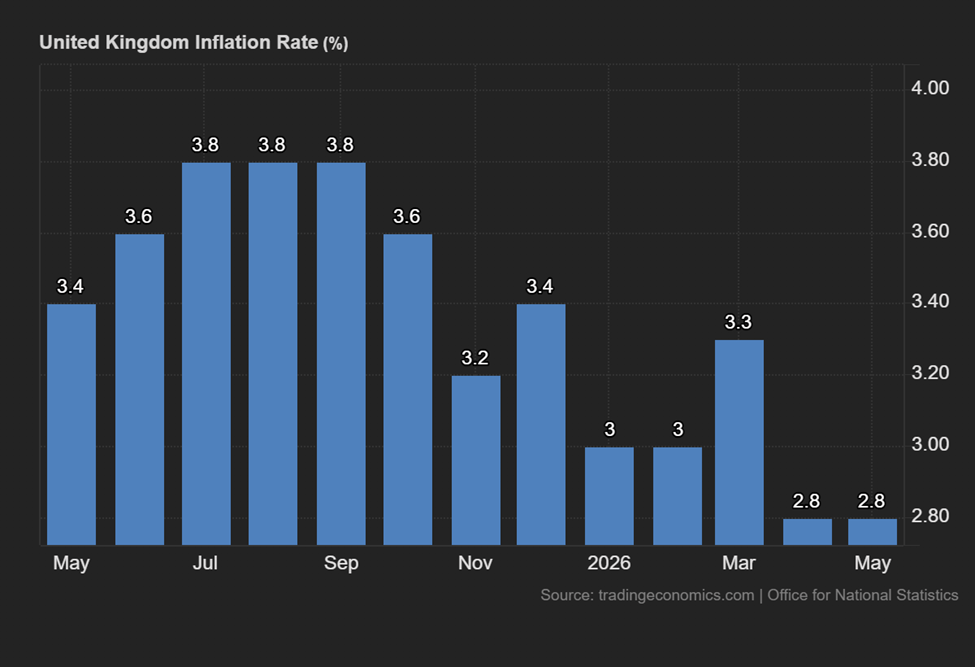

However, based on recent inflation data, tighter monetary policy doesn’t seem immediately necessary:

Rather than rising as expected in the early stages of the current Gulf conflict, British annual headline inflation has actually declined. Early estimates suggest that the rate could have continued to go down last month, possibly as low as 2.4%, so traders will concentrate on the upcoming release on Wednesday 22 July.

A hike by the BoE seems fairly likely in November but the possibility of a move up this month seems very remote. With the current bank rate of 3.75% being significantly higher than annual headline inflation and the latter likely to continue declining in the near future, there’s no clear reason immediately for the BoE to pivot to hiking as soon as possible. At its last meeting, only two members of the Monetary Policy Committee (MPC) voted for a hike.

The week beginning on 20 July is likely to be active for the pound with the job report, inflation and retail sales all being released. Traders will also continue to monitor hostilities in the Gulf and their influence on the price of oil plus developing sentiment on Andy Burnham’s incoming government.

Cable reaches two-month highs as political worry subsides

Efforts by likely incoming Prime Minister Andy Burnham to stress continuity and involve figures on the right of the Labour party in the change of government have been received positively by participants in financial markets. Monetary policy is less of an intrigue in Britain with the BoE unlikely to hike until the fourth quarter, but there are differing possibilities for the Fed in September with the likelihood of a hold and single hike nearly equal.

15 July’s large up candle, cable’s strongest daily gain since April, pushed clearly above all the moving averages here. The price has now retraced and might consolidate around $1.35 in the near future dePending on news. A strong gain like 15 July might in itself suggest further upward movement but there’s evidence of buying saturation from the slow stochastic and volume hasn’t increased. The area slightly above $1.36 is a possible resistance.

A retreat below $1.34 seems unlikely technically but might be driven by news from the Gulf or British politics. If the price breaks back below $1.35, the 200 SMA around $1.343 could cap losses at least temporarily. Traders will now monitor several important British releases coming up, primarily the job report on 21 July and inflation on 22 July.

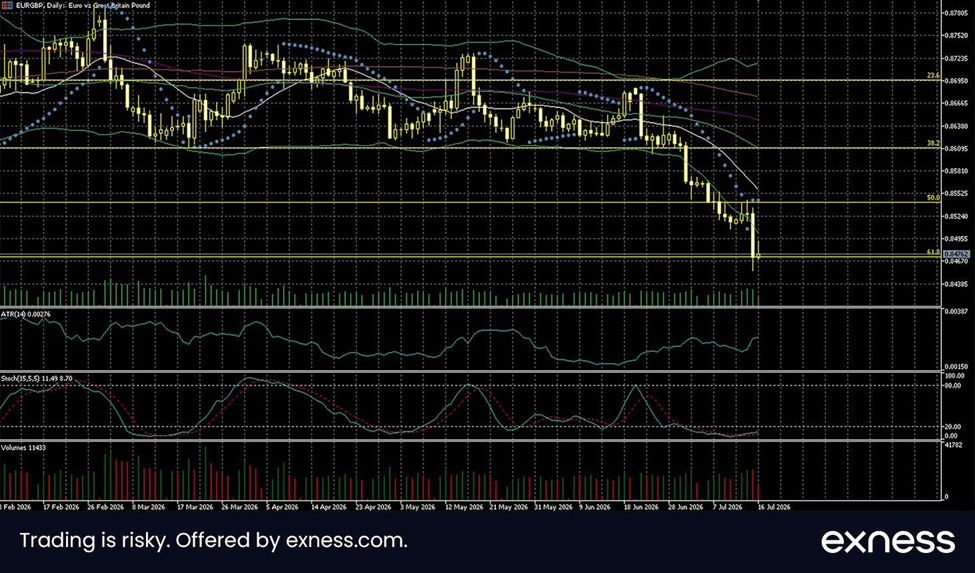

Euro-pound reaches fresh annual lows

The pound made strong gains on 15 July against most major currencies including the euro as participants expected less of a lurch leftward by the incoming British government under Andy Burnham. The ECB seems to be broadly more hawkish than the BoE with a hike by the former likely in September, but the difference in rates remains 1.25% in favour of the pound, so the carry trade in itself will probably continue to pressure euro-pound lower.

Although the downtrend now seems obvious, this situation is challenging for new sellers because the price is so strongly oversold. With volume having been mostly steady since last month, selling around the lows seems even more questionable than usual. The 61.8% weekly Fibonacci retracement is also a possible support. A bounce to around 85p or at least a move out of oversold based on Bands and the slow stochastic might derisk the entry somewhat.

The 50% Fibo around 85.4p is a possible resistance and might cap any potential bounce to come, but basic fundamentals don’t support an ongoing strong bounce. Apart from the British job report and inflation coming up on 21 and 22 July respectively, traders will also watch the ECB’s press conference on 23 July closely.

Author

Michael Stark

Exness

Michael has been investing since 2007 and trading CFDs since 2013. He favors considering both fundamental and technical analysis where possible, with a focus on swing and position trading.