LNG enters flexibility phase as storage season progresses

Key takeaways

- European storage continues rebuilding, although refill dynamics increasingly depend on cargo flexibility rather than abundant supply.

- Asian LNG demand is recovering, drawing additional cargoes toward Pacific buyers as competition for flexible volumes strengthens.

- Shipping risks across Hormuz and the Red Sea continue influencing voyage planning, delivery timing and freight conditions.

- The Renko structure remains balanced, with price holding above the EMA 21 while participation stabilizes around a neutral regime.

LNG enters a flexibility-driven market

Liquefied natural gas enters Friday's session with market attention gradually shifting away from concerns surrounding outright supply availability and toward the operational flexibility of the global LNG system.

European storage injections continue progressing through the summer refill season, while Asian buyers are returning more actively to the spot market following several months of relatively subdued purchasing activity. These developments are occurring against a backdrop of persistent geopolitical uncertainty across major shipping corridors, creating an environment where timing, destination flexibility and cargo allocation increasingly determine market pricing.

The softer US inflation data released earlier this week have also contributed to a more supportive macro backdrop by easing pressure on Treasury yields and reducing strength in the US Dollar. Financial conditions have become slightly more accommodative for commodity markets, although LNG continues to derive its primary pricing signals from physical trade flows rather than monetary expectations.

As the injection season advances, the market is increasingly evaluating which cargoes remain available, how quickly they can be redirected and where they generate the highest marginal value.

This transition defines the current phase of the LNG market.

Storage season increases the value of flexibility

The European refill campaign remains well underway, although inventory accumulation has become increasingly sensitive to competition from Asia.

According to Reuters, Asian LNG imports are expected to reach approximately 23.05 million tonnes during July, representing the strongest monthly level in six months. China is projected to import around 5.62 million tonnes, reflecting a substantial recovery from the lows recorded earlier this year. At the same time, European LNG imports are expected to ease toward 6.9 million tonnes, illustrating how cargoes are gradually responding to stronger Asian demand signals.

The European market therefore faces a different challenge than earlier in the year.

Supply remains available.

Storage continues expanding.

The key variable increasingly becomes the ability to attract sufficient flexible cargoes before winter.

Reuters estimates that European storage still trails the historical seasonal trajectory by roughly 158 TWh, highlighting the importance of maintaining consistent injections throughout the remainder of the summer.

Rather than creating immediate supply stress, this situation gradually increases the economic value of flexible LNG volumes capable of responding quickly to changing regional demand.

Cargo allocation becomes the primary pricing mechanism

Global LNG pricing increasingly reflects optionality.

Each cargo carries value through its ability to move between competing demand centers.

Portfolio players continuously evaluate destination economics.

Utilities compare regional spreads.

Trading houses optimize voyage economics.

Every routing decision contributes to price formation.

This process is becoming increasingly important as Europe and Asia compete for the same pool of uncommitted cargoes.

The European LNG system currently remains balanced.

Total regasification flows reached 361.37 mcm, while concentration indicators continue describing a diversified network with the Top 3 terminals accounting for 29.2% of throughput and an HHI of 572.9, indicating that flows remain broadly distributed across the region rather than concentrated in only a handful of facilities.

Terminal activity also illustrates the ongoing redistribution of physical volumes.

Gate Terminal continues operating as one of Europe's principal entry points, while Wilhelmshaven and Eems Energy Terminal have recorded meaningful weekly increases in throughput. The network continues absorbing LNG efficiently, although future injections increasingly depend on the availability of globally flexible cargoes rather than local infrastructure capacity.

This evolution reinforces LNG's identity as a cargo market.

Price increasingly reflects flexibility.

Shipping continues shaping market optionality

Maritime logistics remain one of the most important transmission channels for LNG pricing.

Shipping intelligence continues highlighting elevated operational risk across the Strait of Hormuz and the Red Sea. Although large-scale disruptions have not materialized, security concerns continue influencing voyage planning, insurance costs and routing decisions across several energy corridors.

The latest shipping radar continues classifying the current environment as EXTREME STRESS, with multiple active risk signals affecting freight markets and regional energy logistics. Flow-related alerts remain present alongside security developments, indicating that transportation conditions continue requiring active operational adjustments.

For LNG participants, these developments matter because shipping flexibility directly influences commercial flexibility.

Longer voyages reduce vessel availability.

Alternative routes increase transportation costs.

Scheduling uncertainty reduces portfolio optimization.

Each additional constraint reduces the number of cargoes capable of responding quickly to regional pricing opportunities.

The physical market therefore continues assigning greater value to operational flexibility than to nominal supply availability.

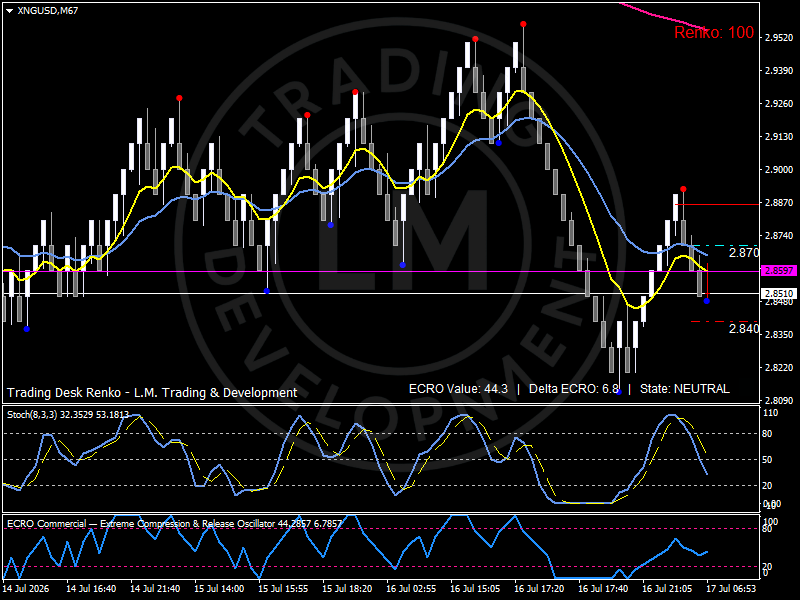

Technical structure

The Renko chart continues describing a balanced market transitioning toward a new participation phase.

Price remains above the EMA 21, preserving the constructive structure established during the recent recovery, while the EMA 9 has flattened as short-term participation moderates.

The EMA 200 remains well above current prices, illustrating that the broader long-term trend still reflects the earlier structural decline, while the recent recovery continues building a more stable medium-term base.

The ECRO oscillator stands at 44.3, confirming a neutral participation regime consistent with a market redistributing positions rather than expanding directionally.

At the same time, Delta ECRO has improved to +6.8, indicating that participation is gradually rebuilding as buying interest stabilizes after the recent rebound.

The stochastic oscillator has rotated lower from overbought territory toward the middle of its range, remaining consistent with a consolidation phase rather than a deterioration in market structure.

Immediate participation develops between 2.85 and 2.87, while initial support is located near 2.84. Price continues oscillating around these levels as the market waits for the next catalyst capable of increasing directional participation.

Bird's eye view

The LNG market is progressively evolving into a flexibility-driven pricing regime.

European storage continues advancing.

Asian demand is recovering.

Cargo allocation is becoming increasingly dynamic.

Shipping risks continue influencing delivery timing across major maritime corridors.

Every flexible cargo acquires greater strategic value as buyers compete for reliable deliveries during the remainder of the refill season.

The interaction between storage progress, cargo mobility and maritime logistics increasingly defines LNG price formation.

Outlook

LNG enters the second half of July with a market structure centered on flexibility rather than scarcity.

The pace of European storage injections, the recovery in Asian imports and the resilience of global shipping networks are likely to remain the dominant variables shaping pricing over the coming weeks.

As long as storage continues rebuilding and maritime logistics remain operational, the market is likely to remain balanced. The premium assigned to flexible cargoes may continue increasing as Europe and Asia optimize procurement strategies ahead of the winter demand cycle.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.