Stocks and gold – Hot and hotter

The rebound off Tuesday‘s lows continued semisuccessfully yesterday – further upside was rejected in spite of signs of strength both within the S&P 500 and outside markets. Technically, the bulls are still on a dicey, vulnerable ground – but increasingly less so. It‘s that VIX is calming down, and the put/call ratio has sharply moved into its complacent spectrum. And not only that – new highs new lows are rising in spite of the advance-decline line being little moved.

These are all budding signs of the upcoming break higher, and no change in the reflationary positive dynamics for stocks, let alone the red hot commodities. These (copper, agrifoods, base metals, lumber, oil) continue appreciating in spite of nominal yields pulling back a little these days. Make no mistake though, deflation isn‘t about to break out.

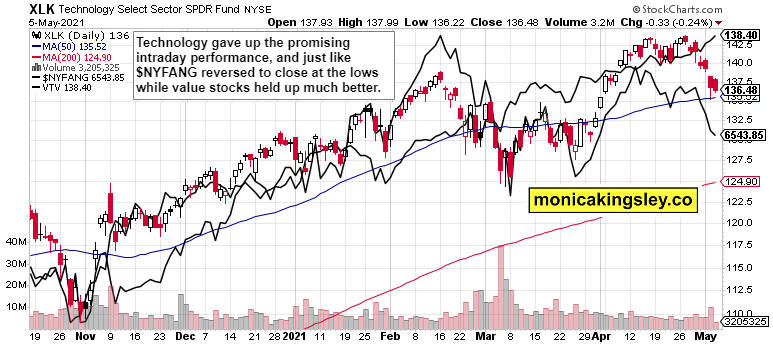

Lower yields no longer work in support of all the defensive sectors – technology has passed the leadership baton long ago to value stocks (think Mar), but appears to be bottoming here in spite of the reversal late yesterday. That‘s positive as any S&P 500 advance has to count on both value and tech pulling ahead more or less simultaneously. A welcome sign of returning animal spirits in the 500-strong index would be the Russell 2000 juices flowing again. Thus far, even the emerging markets are hesitating.

Not that they should be – the USD Index looks very vulnerable to me here, and its anticipated downside move (the smoke and mirror games I talked about on Monday and Wednesday are nothing but a distraction) would help lift international markets, and is also part of the explanation behind the strong commodity performance these days. This CRB Index move is key, and shows how far have real assets progressed in shaking off the dollar link – if you compare the dollar‘s value in early Feb and now, you are looking at very meaningfully higher commodity prices over that same time period.

Gold and silver are about to shake off the dollar shackles as they catch up to commodities that have left them in the dust since Aug or Nov. The key metrics such as nominal or real yields support the precious metals rebound increasingly more – don‘t be fooled, gold would break above the $1,800 resistance, whether you look at it as a purely psychological one, or as a neckline of an inverse head and shoulders on the daily chart.

The advance across the real assets, the precious metals and commodities super bull, would be more well rounded then. As I wrote yesterday:

(…) I‘m known for incessantly beating the copper bullish drum, and also the oil one, and here we are with further gains added since my latest oil analysis. Silver might pull back a little here, but look for it to mirror the insatiable appetite for base metals and other commodities. Beyond the Green New Deal mandates, the monetary demand is set to help power the white metal higher.

Let‘s move right into the charts.

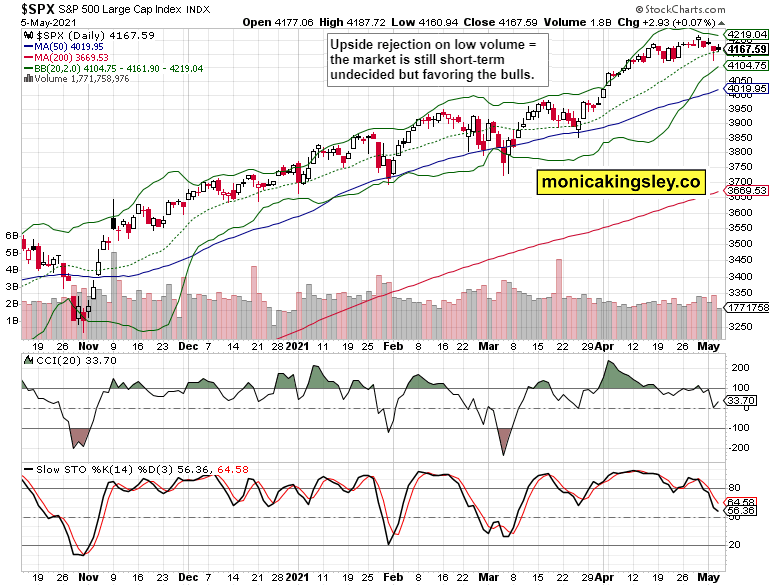

S&P 500 Outlook

Short-term vulnerability and drying up volume as we‘re waiting for the daily indicators to turn brighter. Some more sideways trading would do that trick.

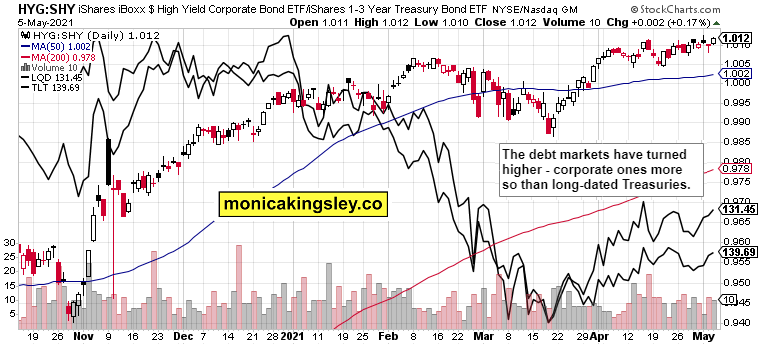

Credit Markets

The corporate credit markets keep signalling higher stock prices next, though. Notably, both HYG and LQD rose in spite of long-dated Treasuries turning up as well.

Technology and Value

Did it bottom, did it not? For much of yesterday‘s session, the tweezer bottom approximating formation was in place. Both semiconductors (XSD ETF) and heavyweights ($NYFANG) gave up the encouraging intraday gains, and value (VTV ETF) wasn‘t strong enough to save the day. The question of a tech bottom remains of crucial importance, and looking at the distance between both XLK and $NYFANG price swings relative to the 50-day moving average, the odds are good for higher tech prices right next.

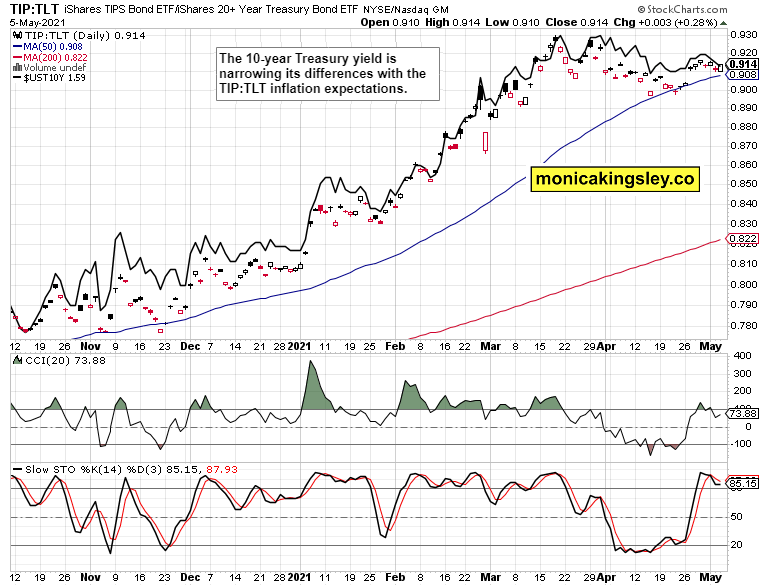

Inflation Expectations

Inflation expectations have moderated their run, and are currently consolidating. The key sign here is that Treasury yields are no longer frontrunning them, but have come modestly down lately. Coupled with the USD/JPY below 109.20 making a rounding top, that‘s one less headwind for gold.

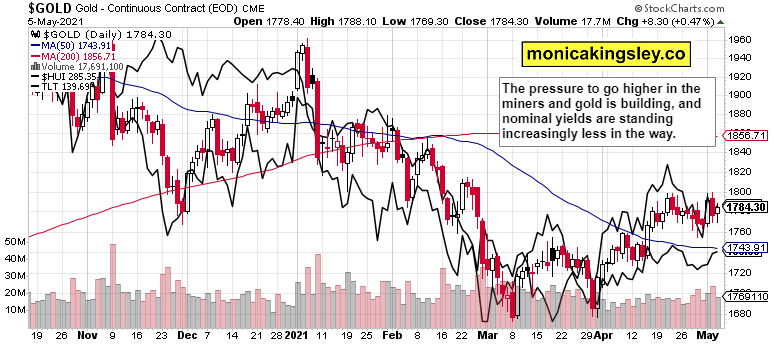

Gold, Silver and Miners

Miners aren‘t underperforming, and the tentative signs of strength beyond the intraday flavor returning, are there.

-637559096396007075.png)

Silver didn‘t outperform yesterday, which means that the precious metals sector isn‘t approaching short-term overheating. At the same time, the copper to 10-year Treasuriy yields is increasingly supportive of the coming gold upleg.

Summary

S&P 500 is short-term consolidating only, and getting ready for a new upswing whenever the technology behemoths turn. These are the decisive factor of sustainable and noticeable stock market gains.

Gold and miners have bullishly consolidated yesterday, and are amply supported by related markets to score strong gains next.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.