SP500 Analysis: Can a new stimulus package save the stock market? [Video]

![SP500 Analysis: Can a new stimulus package save the stock market? [Video]](https://editorial.fxstreet.com/images/Markets/Equities/SP500/wall-street-sign-637299022550250958_XtraLarge.jpg)

Bulls believe there is room to climb even higher with many U.S. citizens getting another $600 for passing "Go" and perhaps another $1,400 from "Community Chest".

Buyers are also looking to continued low interest rates and energy prices, and the steadily progressing vaccine rollout. At the same time, we see an increased number of small businesses bankruptcies.

Technical analysis

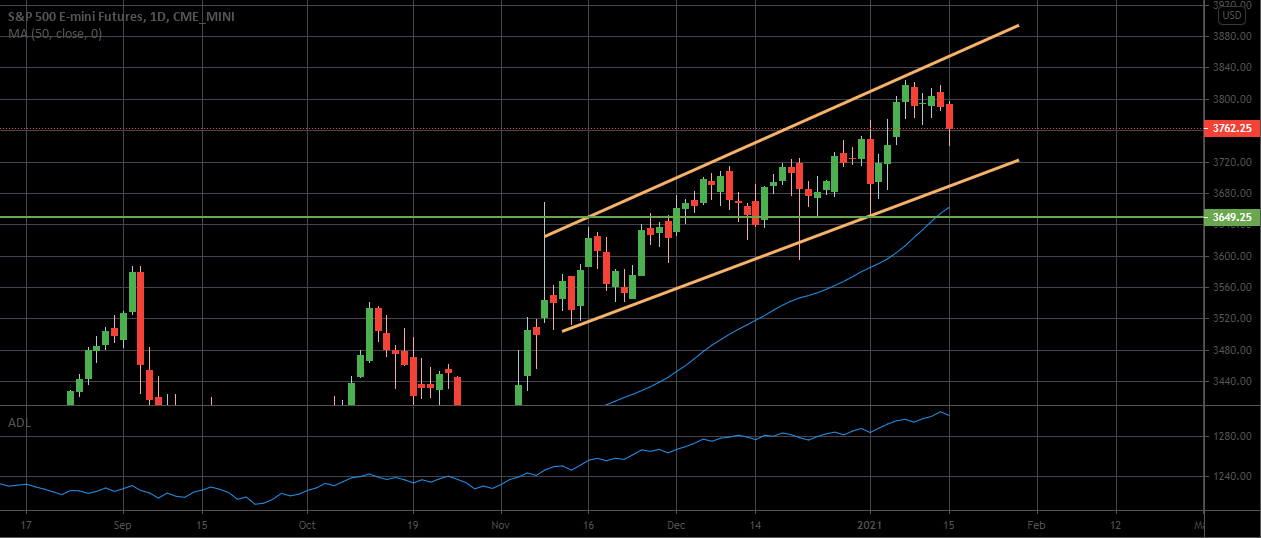

There is a clear channel up on the daily chart. The price is just in the middle of it. With that in mind, we have few levels to watch. If price finds support near the lower range of the channel (3720), we can see the next leg to the upside with potential extension to 3900. If 37200 fails, the nearest support is at 3650. There is still no Advance Decline Line signal. Based on Cycles study we can expect deeper pullback and swing buy entry between March and April. So, the best for now is to focus on short-term trading from mentioned above levels.

Fundamental Analysis

President-elect Joe Biden unveiled a massive $1.9 trillion stimulus plan, titled "American Rescue Plan", which includes more direct payments to qualifying taxpayers, expanded unemployment benefits, a federal minimum wage increase to $15 an hour, extension of eviction and foreclosure moratoriums, changes to the child tax credit, $350 billion in state and local aid.

The package also calls for more than $400 billion to combat the pandemic, including accelerating vaccine deployment and safely reopening most schools within 100 days of the spending bill's passage.

President-elect Biden's package will likely sail through the House with the Democrats in control but he would need at least 10 Republicans to join all the Democrats in the Senate to overcome a filibuster.

Biden also plans to unveil another set of spending proposals in February which Washington insiders say will likely be larger than the Rescue Plan. That package is expected to focus on infrastructure, health care, and education.

Investors are also digesting comments from Fed Chair Jerome Powell who warned that central bankers should be careful not to pullback on easy monetary policy too early.

Powell's comments come amid some concerns on Wall Street that the Fed might reign in asset purchases sooner than expected. Powell said the economy remains far from the Fed's goals but he is optimistic about the recovery.

Powell did warn that a post-pandemic economy could even see some “exuberant spending” that pushes inflation higher but brushed off ideas surrounding "persistent" inflation, citing disinflationary trends across the globe.

He also said any moves to ease asset purchases or raise interest rates would be broadcast well in advance. The Fed's next policy meeting is January 26-27.

The big event for the week is of course the Presidential Inauguration on Wednesday, January 20. Wall Street will also be tuning in the day before on Tuesday, January 19, with the Senate Finance Committee set to hold a hearing on Janet Yellen’s nomination to be Treasury secretary.

This is a highly anticipated appointment that the bulls are extremely comfortable with as the former Fed Chair is notoriously dovish.

Yellen is expected to win easy confirmation, making her the first woman to serve as Treasury secretary and also the first person to have held all three top economic posts — chair of the president’s Council of Economic Advisers, chair of the Federal Reserve, and head of Treasury.

Next week also brings fresh housing data, including Housing Starts on Thursday and Existing Home Sales on Friday. Earnings will also be on tap next week, with key results due from Bank of America, Goldman Sachs, and Netflix on Tuesday; Morgan Stanley, Procter and Gamble, United Health, and U.S. Bancorp on Wednesday; Charles Schwab, CSX, IBM, and Union Pacific on Thursday.

Author

Inna Rosputnia

Managed Accounts IR

Inna Rosputnia is a stock and futures trader, portfolio manager and financial analyst that has been in the trading industry for the last 12 years.