Silver enters industrial resilience phase as growth expectations stabilize

Key takeaways

Silver trades around the 60.00 participation pivot as investors reassess industrial demand following a week dominated by Federal Reserve communication.

Treasury yields have stabilized after the release of the FOMC Minutes, allowing market attention to gradually shift back toward manufacturing activity and broader industrial participation.

The US Dollar remains range-bound, reducing immediate pressure on industrial metals while investors evaluate the outlook for global growth.

Silver enters the end of the week with improving technical participation as cyclical demand and industrial expectations regain influence across the metals complex.

Silver returns to its industrial identity

Silver finishes the week inside a market that is becoming increasingly driven by the quality of economic growth rather than by immediate monetary policy repricing.

The publication of the FOMC Minutes provided additional clarity regarding the Federal Reserve's policy framework. While policymakers maintained a cautious approach toward inflation and future rate adjustments, the Minutes largely confirmed expectations already embedded in financial markets.

As policy uncertainty becomes less dominant, investors are once again evaluating the strength of the underlying industrial cycle.

That transition is particularly important for silver.

Unlike gold, whose valuation is primarily influenced by reserve allocation and monetary credibility, silver derives a substantial portion of its value from manufacturing activity, electrification, technology investment and broader industrial production.

The market therefore begins shifting from policy interpretation toward industrial participation.

This transition creates a different pricing environment.

Rather than reacting exclusively to Treasury yields or Federal Reserve communication, silver increasingly reflects expectations surrounding factory activity, infrastructure investment and the resilience of industrial demand.

Growth moderation supports a more balanced market

Recent macroeconomic data continue describing an economy that is slowing gradually without entering a contraction phase.

The latest ISM Services reading remained comfortably above the expansion threshold despite moderating from previous levels, reinforcing the idea that economic activity continues expanding while becoming more balanced.

This environment reduces the probability of aggressive macro repricing.

Instead, investors are increasingly differentiating between sectors that remain structurally supported and those that depend entirely on monetary stimulus.

Industrial metals belong to the first category.

Demand associated with electrification, renewable-energy infrastructure, data-center expansion and manufacturing investment continues providing a structural foundation for silver consumption even as overall economic momentum becomes more moderate.

This combination allows industrial participation to remain active without requiring an acceleration in economic growth.

Markets therefore begin rewarding resilience rather than rapid expansion.

That distinction becomes increasingly relevant for silver because industrial demand tends to evolve over medium-term investment cycles rather than responding exclusively to individual economic releases.

Copper continues guiding industrial participation

Silver rarely moves in isolation.

Copper remains one of the most important reference points for evaluating industrial participation across the metals complex.

Although price volatility has moderated compared with earlier phases of the year, copper continues reflecting expectations regarding manufacturing activity, infrastructure spending and long-term electrification demand.

That relationship matters because institutional investors frequently evaluate industrial metals as an interconnected ecosystem.

When confidence in manufacturing conditions improves, participation tends to broaden across the sector rather than concentrating on a single commodity.

Silver benefits from that dynamic.

Its dual role as both a precious and industrial metal allows it to attract flows from investors seeking exposure to cyclical growth while maintaining diversification characteristics typically associated with precious metals.

This hybrid identity continues distinguishing silver from other commodities.

Rather than competing directly with gold, silver occupies a position where industrial activity and macro positioning evolve simultaneously.

Treasury stability allows industrial themes to re-emerge

The stabilization of Treasury yields represents another constructive element for silver.

During periods of rapid yield repricing, monetary policy tends to dominate commodity pricing.

As volatility across fixed-income markets declines, investors gain greater visibility regarding underlying sector fundamentals.

Silver has begun benefiting from that transition.

The current environment allows industrial demand expectations to regain influence while Federal Reserve policy gradually shifts into the background.

This does not imply that monetary policy has become irrelevant.

Treasury yields continue influencing financing conditions, investment flows and Dollar dynamics.

The difference is that those variables no longer generate the same degree of day-to-day uncertainty observed around major policy events.

That reduction in macro volatility encourages a broader evaluation of structural demand drivers.

For silver, those drivers remain centered on industrial consumption, manufacturing resilience and long-term investment linked to the global energy transition.

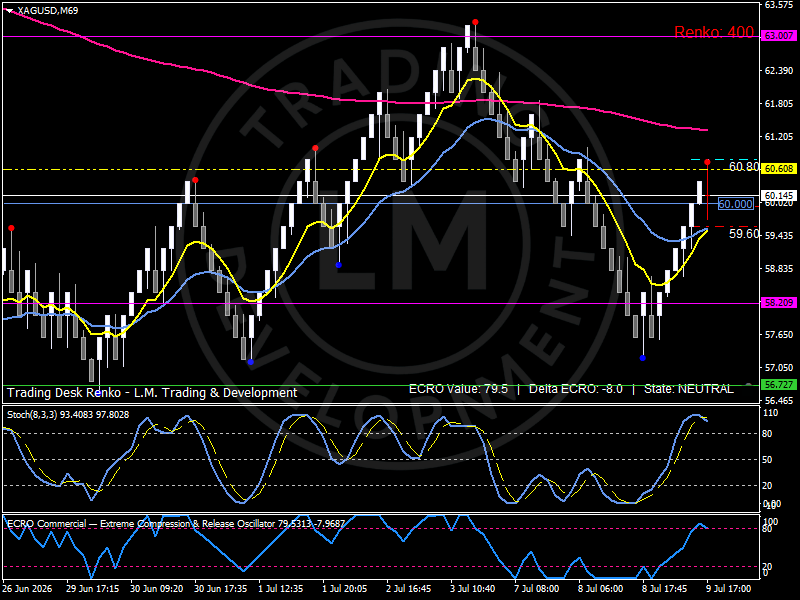

Technical structure: Participation rebuilds around the 60.00 pivot

The technical configuration closely reflects the broader macro narrative.

Silver has recovered from the recent corrective phase and now rotates around the 60.00 participation pivot, where buyers and sellers continue establishing a more balanced equilibrium.

Immediate resistance develops between 60.15 and 60.30, while the next participation objective emerges near 60.60.

On the downside, the first dynamic support remains around 59.60, followed by the broader structural support near 58.20.

The EMA 9 has moved back above the EMA 21, indicating renewed short-term participation after the recent recovery.

Meanwhile, the EMA 200 remains above current prices, reminding investors that the longer-term structural trend has not yet fully transitioned back into expansion.

ECRO currently stands near 79.5, signaling that participation has strengthened meaningfully compared with the previous sessions.

Delta ECRO remains modestly negative, suggesting that the initial recovery impulse has entered a consolidation phase rather than a renewed acceleration.

The stochastic oscillator remains elevated following a strong rebound, indicating that participation continues supporting the recovery while allowing room for additional consolidation before the next directional expansion.

Overall, the technical picture describes a market rebuilding participation instead of chasing momentum.

Bird's eye view

Silver currently operates inside an industrial resilience regime where manufacturing expectations, copper leadership and structural demand remain increasingly interconnected.

The dominant transmission channel now runs from growth expectations to industrial participation and from industrial participation to silver pricing.

Technically, the market continues rotating around the 60.00 participation pivot, with resistance concentrated between 60.15 and 60.60, while support remains around 59.60 and 58.20.

Both the macro and technical frameworks describe a market rebuilding participation through improving industrial confidence rather than through monetary-policy repricing.

Outlook

Silver enters the new trading phase with attention gradually shifting away from Federal Reserve communication and back toward the resilience of the industrial cycle.

Manufacturing activity, infrastructure investment and long-term electrification continue providing structural support for industrial demand, while the stabilization of Treasury yields allows those themes to regain prominence.

The next directional phase will likely emerge from the interaction between growth expectations, industrial participation and the broader evolution of manufacturing activity across the global economy.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.