Signs of a decline in globalization

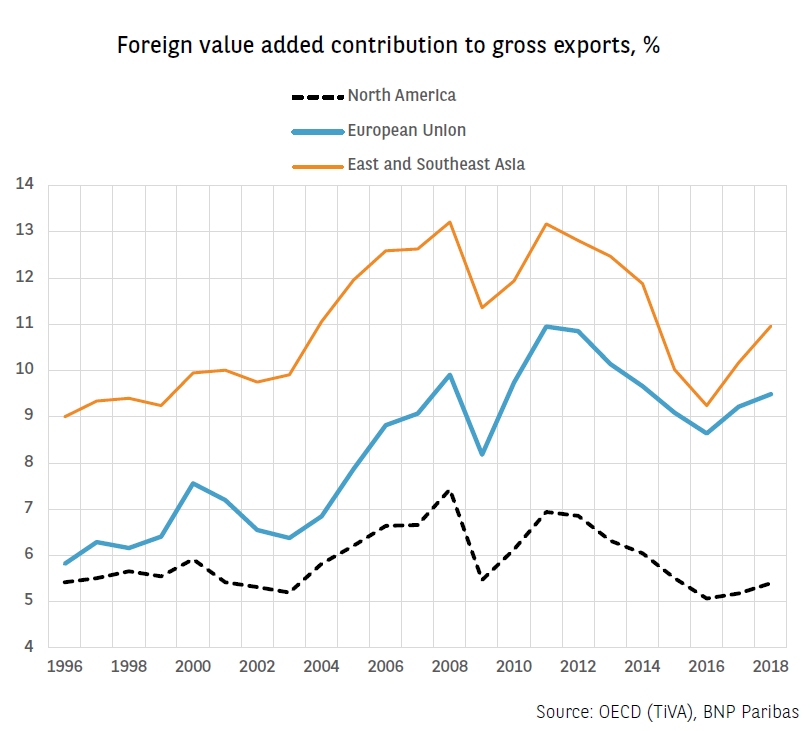

The Covid-19 crisis is still generating lively discussions on the future of globalisation of trade and finances, and global value chains. The share of foreign value added embedded in the exports of a country or region is a good indicator of the level of involvement in global value chains. This share increased rapidly from the early 1990s until the global financial crisis of 2008, under the effect of trade liberalisation (cuts in tariffs and proliferation of free trade agreements) and falling transport costs. This increase was particularly significant in Asia, the emergence of China as the factory of the world leading to the imports of more intermediary goods mainly from Europe and North America.

After the Great Recession of 2008, globalisation has slowed, as the foreign inputs in the major regions have declined. One reason is that trade in intermediate goods have become more regionalised. German industry has increased the inputs from Central and Eastern Europe, whereas the US manufacturing sector has focused more on Mexico. By moving up in the value chain, China has become less dependent on the inputs from the OECD countries and even became a competitor for Western industries. The foreign input share of East and South-East Asia lost even three percentage points between 2010 and 2016, before climbing again. The Covid-19 crisis may strengthen the trend towards more regionalisation as industries seek to improve the resilience of supply chains, e.g. reliance on multiple suppliers, greater redundancy in transportation and logistics.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.