Shock UK job losses help cement August rate cut

The cooling in the UK jobs market is gathering pace. Wage growth is slowing, too. While the bar for the Bank of England to speed up rate cuts seems to be set fairly high, this data helps cement cuts in August and November.

The UK jobs market might be turning a corner – and not in a good way. What stands out from the latest hiring numbers is a sharp 109,000 fall in payrolled employees in May. That is the largest monthly fall outside of the Covid-19 pandemic, since the data began in 2014.

However, there’s a fairly significant caveat, which is that this data has a habit of being revised up later on. Back in March, we saw a 78,000 fall, which was later revised up to a drop of 35,000. We’ll have to reserve full judgment until next month.

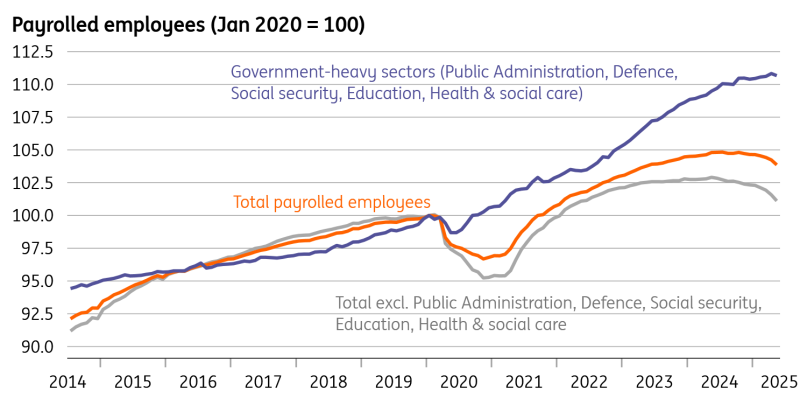

Even so, these employee numbers have fallen for nine of the past 10 months, following a 44-month positive streak. The figures also look a little more dramatic when you strip out sectors dominated by the government. Our “ex-government” measure of employee numbers has fallen by 1.2% since December.

Remember, too, that this data is the most reliable way of analysing the jobs market right now, at a time when the unemployment rate and associated labour force survey are plagued by sampling issues.

Employee numbers are falling more rapidly

Source: Macrobond, ING

The jury’s out on whether this marks the start of a more serious deterioration in hiring conditions. Economists tend to worry when the pace of job losses accelerates, something often associated with recessions. We are sceptical that this is where we are right now, though famously the jobs market is a lagging indicator of economic strength.

Vacancies are now materially below pre-Covid levels and have started falling a little bit faster too. But other metrics don’t look as worrisome. Despite the rise in employers’ national insurance (social security tax) in April, redundancy notices submitted to the government haven’t risen at all.

So let’s see. But if nothing else, this should help cement another rate cut in August and further quarterly cuts in November and into 2026. We wouldn’t totally rule out the Bank of England moving faster, particularly because we are more upbeat about the inflation outlook.

But recent commentary has suggested the bar to speeding up is set relatively high. Officials tend to point to wage growth, which, despite the material cooling in hiring conditions over the past couple of years, has stayed stubbornly high.

This is changing. Private sector wage growth is down to 5.1% from 5.9% two months ago, a faster-than-expected slowdown. Much of that is down to base effects, but it does seem there is a more genuine cooling going on as well.

The latest BoE Decision Maker Panel suggests firms expect wage growth to fall to 3.5% over the coming months. While we’d be sceptical about it going that far in the official data, not least because of the recent near-7% rise in the National Living Wage, we do think the latest fall in wage growth should continue through this year.

Read the original analysis: Shock UK job losses help cement August rate cut

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.