Separating economic fact and fiction – A market discussion with Ed Moya

The global economic situation is fraught with danger and possibility. Negotiating the currents and rapids of the trading environment calls for careful analysis and wisdom. From the risk-aversion and funding ascent of the US dollar in March to the hoped-for economic recovery, Brexit and the US Presidential election no one is better equipped to examine background and trends than Ed Moya, senior market analyst for OANDA. Join Joseph Trevisani, senior analyst at FXStreet for a discussion of these unique times and events.

Ed Moya: Good Morning Mr. Trevisani!

Joseph Trevisani: Felicitations Mr. Moya. Thank you for joining us at FXStreet. From your post at OANDA, you have seen and analyzed some of the most volatile markets of the last decade

Joseph Trevisani: Economic recovery in the US and around the world is the next topic for markets.

Joseph Trevisani: Do you think we can go up as fast as we went down?

Ed Moya: Always a pleasure Mr. Trevisani

Joseph Trevisani: The intensity and the speed of the collapse would seem to argue for an equal recovery. Historically the sharper the recession the faster the economic rebound

Ed Moya: It is fascinating how fast the Fed was in launching an array of programs that have helped markets and the economy throughout COVID-19. The Fed has been very clear in delivering the message that they are ready to do even more. I think much of Wall Street was expecting a frustration phase and this last leg up pretty much-crushed short-sellers. I'm skeptical of going forward mainly because of the permanent damage to the economy. Stimulus can't save all the jobs and with that, we will have a much weaker US consumer.

Ed Moya: The initial sugar high from the stimulus is easing and the rest of the recovery will be much slower

Joseph Trevisani: True, but there has been an enormous amount of deferred spending. If that starts to return in June and the third quarter, it may give businesses the funds to hire.

Joseph Trevisani: I know a number of small and medium-sized business owners, as a group they all desire to return to their firms. I think the plain and human desire to normalize is hard to fit into economic projections and may be the strongest component of a recovery.

Ed Moya: Yes, I completely agree that a big initial boost will occur from deferred spending, but a large part of the country lives paycheck to paycheck and many individuals who are at higher risk for severe illness will not contribute as much as they had before the virus.

Ed Moya: If we look at the initial results from Georgia (cell phone data) one of the earlier states to reopen, a lot of people are not going out and the economic activity is somewhat muted.

Joseph Trevisani: This is a particularly difficult event to model. The comparison I make is between the financial crisis and the first term Reagan recession

Joseph Trevisani: In the Reagan recessions the cause was plain, the Fed anti-inflation rate increases.

Joseph Trevisani: As soon as it was clear Volcker was changing policy, consumer sentiment, and soon the economy rebounded quickly.

Joseph Trevisani: In the 2008 crash, the causes were many and diffuse and the Fed and government policies enacted were far less successful in the near term, and so consumer outlook and spending recovered much more slowly.

Joseph Trevisani: I think we may now follow the Reagan model, however, the job losses are much more severe and faster.

Ed Moya: The big question is what happens over the next couple of quarters and unfortunately the job destruction, business bankruptcies, and defaults will finally dent optimism. The lingering uncertainty of the coronavirus makes this recovery clouded. Optimism is sky high that a vaccine will be in place by next year, but many businesses will refrain from making capex decisions off of hope.

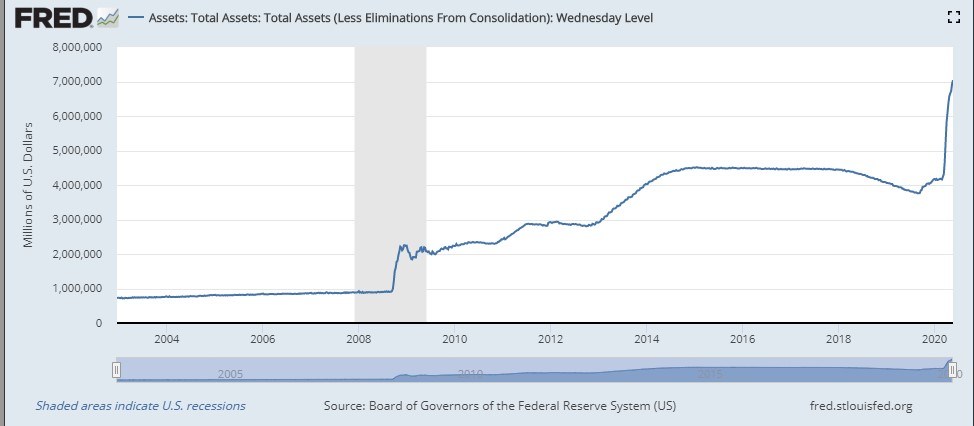

Ed Moya: The Fed's actions have been significantly more aggressive than what happened during the Great Recession and as the balance sheet approaches $10 trillion, we will start to see the effectiveness of stimulus fade.

Ed Moya: Federal Reserve total assets

Ed Moya: We will be trapped in a low-interest-rate environment for a while and right now the Fed will be focused on all the deflationary pressures that will persist in the short-term.

Joseph Trevisani: On the other hand from a cost point of view...now is an excellent time for investment, and even if the recovery is slow, the investment could be cost-effective. Still, on this one, it’s a matter of assumption and conviction. When you model the recovery from this event you are mostly modeling your own assumptions.

Joseph Trevisani: On a more difficult topic, the US Presidential election is about to take over the news flow. In a way, this may help people forget about or at least downplay the virus. The intensity of the media coverage will certainly slacken. Equity markets seem to be positioned for a strong recovery. Though I don’t think the market is yet pricing the election.

Joseph Trevisani: Yes, zero interest rates are a policy trap. The Fed managed to largely avoid the trap after the crash, as the ECB did not, and the BOJ has been essentially at zero for two decades.

Ed Moya: The economic outlook could go out the window if we see a clean sweep by the Democrats. A few months ago, everyone assumed Trump would get re-elected and keep the Senate. Now it seems everything is up for grabs.

Joseph Trevisani: True, the economics of the shutdown have made the election far more difficult to predict. And to some degree the election may turn on the recovery itself, the faster and stronger being likely better for Trump's election.

Ed Moya: Trump's greatest political asset was a strong economy and his handling of the coronavirus, an impossible situation, has many believing that could lead him to defeat. Eventually, financial markets will reflect the possibility that Biden can win, and that will weigh on the outlook. It warrants attention however now even if one doesn't put a lot of weight in models this early and especially as everyone's situation will greatly change over the next six months.

Joseph Trevisani: Yes we are certainly in for an interesting six months.

Joseph Trevisani: The dollar risk premium has not completely faded. Do you think this is a function of the appreciable risk of the pandemic return?

Joseph Trevisani: The USD/CAD broke its two-month support yesterday, but has crept back above 1.3800 today.

Ed Moya: It seems we always have some geopolitical risk that will warrant new safe-haven flows. Tensions between the world's two largest economies, Hong Kong's security law, and a second peak/wave of COVID-19 are providing steady flows when risk appetite wanes. Most of the scientists I have listened too are all confident the pandemic will return and that will keep the dollar somewhat supported. The Canadian dollar is slowly breaking out as oil price volatility has eased and as expectations grow that the oil market will balance next month.

Joseph Trevisani: Stronger oil demand would argue for recovery. The rhetoric between the US and China has largely, but not completely avoided the trade deal, which seems to be being implemented. I saw a report that Chinese purchases of US pork are sky high. Both sides, whatever their other disputes need the deal for economic recovery.

Ed Moya: You are correct, both China and the US need each other. Circling back to oil, the demand pickup has come out of China has been very impressive. Global oil demand however will see a slower recovery as air travel seems like it won't bounce back as quickly until a vaccine is in place. If you look at the curve for oil prices, WTI crude is not expected to go much higher from current levels. Oil is likely near its near-term high, as the battle for market share amongst OPEC+ and US shale will resume once the market is balanced. The Canadian dollar might see little support from higher oil prices over the medium-term.

Joseph Trevisani: The success of North American shale drillers have capped WTI somewhere between $45 and $50, which is good for the global economy in general as low energy prices keep all costs down.

Joseph Trevisani: A topic that has almost disappeared is Brexit.

Joseph Trevisani: Yet the UK is still leaving the EU. Perhaps the economic disaster from the pandemic will make it easier for the sides to reach agreement, the need for trade to assist revival is so clear.

Ed Moya: Brexit trade talks and negative rate speculation will make this a rollercoaster ride for the British pound. I must give credit to PM Johnson, he has defied his critics and continues to push forward. The June 30th deadline is approaching and this will likely go down to the wire like it always does.

Joseph Trevisani: Such high stakes negotiations are always a last-minute affair. But a successful conclusion would support both pound and the sterling.

Joseph Trevisani: It may take a while for the markets to return to econometrics, though equities seem to be there already, but the US credit market is beholden to the Fed.

Ed Moya: The Brexit cliff-edge remains as the risks remain for the transition period to end without a deal. The UK economy and stock market are benefiting from the freedom to act quickly and swiftly in fighting the impact of the coronavirus.

Joseph Trevisani: It seems like the markets have much to hope for in the next six months but limited certainty. That should make for good trading conditions.

Joseph Trevisani: Ed, it has been too short as always. I would like to thank you for visiting with us and bringing your insights to FXStreet. We have several dinners to work through when we resume our normal lives. I trust Cafe L will survive. Thanks again

Ed Moya: The pleasure was all mine. Looking forward to seeing you hopefully soon.

Author

FXStreet Team

FXStreet