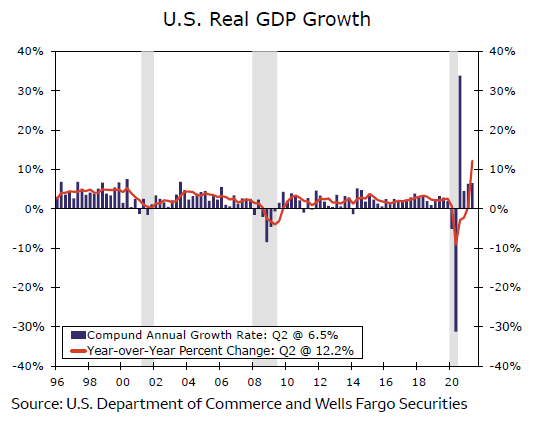

Real GDP grew 6.5% in Q2-2021

Summary

-

Real GDP grew at an annualized rate of 6.5% in Q2-2021, which was not quite as strong as the consensus forecast had anticipated.

-

Despite the lower-than-expected growth rate, real GDP has now surpassed its pre-pandemic peak.

-

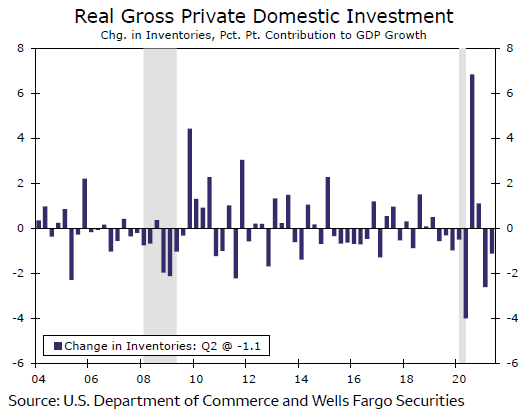

Overall GDP growth was driven by sizable gains in consumer spending and business fixed investment spending. On the other hand, net exports and inventories exerted drags on overall GDP growth.

-

Stocks have been depleted by strong spending and constrained supply. Restockingshould help to support real GDP growth in coming quarters.

-

The PCE deflator, which is a measure of consumer prices, jumped at an annualized rate of 6.4% in Q2-2021, the sharpest quarterly increase since 1982.

Strong PCE growth drives GDP growth in Q2

Data released this morning showed that U.S. real GDP grew at an annualized rate of 6.5% in Q2-2021 relative to the first quarter of the year (top chart), which was not quite as strong as the consensus forecast had anticipated. Despite the lower-than-expected growth rate in Q2, real GDP is now 0.8% higher than it was at its pre-pandemic peak in Q4-2019. That said, output is still 2.5% below where it would have been had the pandemic never happened and real GDP would have grown at its 2010-2019 average rate of 2.3%(annualized) per quarter. In other words, there is still an "output gap," which is consistent with the level of payrolls still 4.4% below their pre-pandemic peak.

Growth in real GDP in the second quarter was driven largely by consumer spending. Real personal consumption expenditures(PCE) shot up 11.8%, which was stronger than most analysts had expected, and every major category of spending posted solid gains. Specifically, spending on durable goods rose 9.9%, non-durable goods jumped 12.6% and services surged 12.0%. This robust growth in real PCE reflects the reopening of the economy that occurred in the second quarter and the fiscal relief measures that put money in consumers' pockets. Growth in business fixed investment spending was also generally robust with equipment spending shooting up 13.0% – businesses continue to invest in tech equipment to facilitate employees working from home–"and spending on intellectual property products rising 10.7%.

Drags from Inventories and net exports

However, net exports and inventories exerted headwinds on overall GDP growth. Although real exports posted a solid growth rate of6.0%, real import grew even faster, rising 7.8%. Consequently, net exports sliced 0.4 percentage points from the topline GDP number. In addition, the $166 billion decline in inventories translated into a 1.1 percentage point drag on overall GDP growth (middle chart). The sizable decline in inventories over the past two quarters reflects strong growth in spending in conjunction with supply shortages that have hampered production. As supply chains become functional again in coming quarters, businesses will endeavor to rebuild stocks and this stock building should support GDP growth in coming quarters. Indeed, we look for overall GDP growth to remain generally solid incoming quarters. Consumers remain flush with cash and there still is pent-up demand for spending on services. Additionally, recent monthly data on factory orders suggest that business spending on equipment remains solid. These orders will need to be produced incoming months. However, the recent surge in COVID cases represents a downside risk to the economic outlook. We do not expect that the economy will lockdown as it did a year ago. That said, consumers could potentially become more cautious regarding travel, restaurant dining, stadium attendance, etc. if cases surge significantly higher.

Author

Wells Fargo Research Team

Wells Fargo