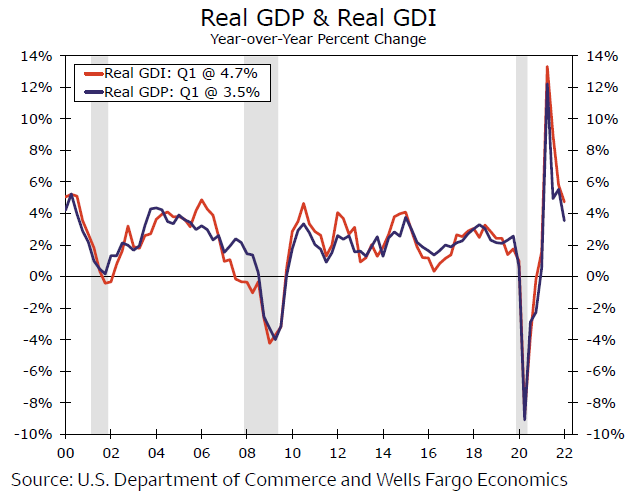

Real GDI shows the economy continued to plow ahead in Q1-2022

Summary

-

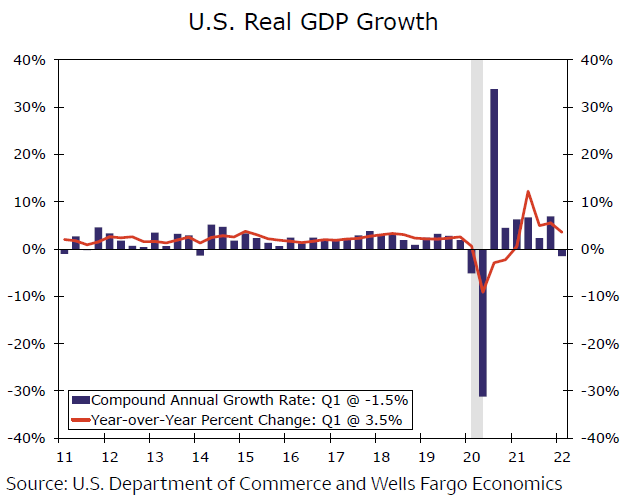

Revised data showed that real GDP contracted at an annualized rate of 1.5% in Q1-2022, which represents a slight downward revision from the -1.4% rate that was reported a month ago.

-

Two volatile spending components (i.e., inventories and net exports) were largely responsible for the contraction in real GDP.

-

The first look at real gross domestic income showed that GDI grew 2.1% in the first quarter, which is more in line with the solid growth in the “core” parts of the spending components that occurred in Q1.

-

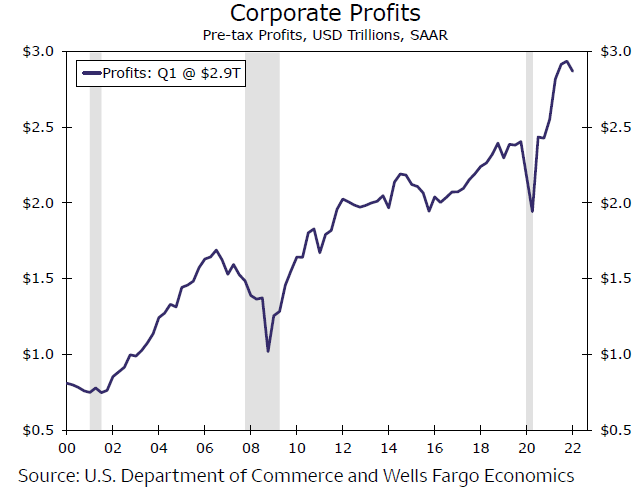

Corporate profits, which account for roughly 8% or so of gross domestic income, slid 2.3% (not annualized) in the first quarter. The profits that are reported in the national income and products accounts are roughly equivalent to operating earnings. But the decline in NIPA profits in Q1 is consistent with the weakness in reported profits that many S&P 500 companies have announced.

-

Our measure of profit margins show some compression in the first quarter. This compression in margins reflects the cost pressures that many companies are facing at present.

Growth in real income shows economy continues to plow forward

Revised data that were released this morning showed that U.S. real GDP contracted at an annualized rate of 1.5% in Q1-2022 (Figure 1). The outturn represents a slight downward revision to the “advance” estimate of -1.4% that was reported last month. The revised data continue to show that two volatile spending components, namely inventories and net exports, were largely responsible for the contraction in real GDP that occurred in the first quarter. Specifically, the downshift in stock building in Q1 subtracted 1.1 percentage points off the overall rate of GDP growth while net exports made a negative contribution to growth that was worth 3.2 percentage points. As we wrote in a report on April 27 that warned of a negative print in the first estimate of GDP growth that was slated for release the following day, the contraction in output in the first quarter does not imply that the economy has slipped into recession.

Today's release also gave us the first look at real gross domestic income (GDI) in Q1-2022. In theory, growth in GDI should be identical to growth in GDP (Figure 2). In practice, however, the two measures are rarely identical due to data errors and omissions. In that regard, real GDI grew at an annualized rate of 2.1% in Q1. This growth in the income side of the national income and product accounts (NIPA) is more in line with the “core” parts of the spending side. Specifically, real personal consumption expenditures grew at an annualized rate of 3.1% in Q1 while fixed investment spending rose 6.8%. In short, the economy continues to plow ahead, despite the modest contraction in real GDP growth in the first quarter.

Profits pull back

Economy-wide corporate profits are a component of income, and typically account for about 8% of GDI. Today's data release showed that corporate profits declined 2.3% (not annualized) in the first quarter on a pre-tax basis. With the advanced report of GDP having largely demonstrated that underlying demand had held up in the quarter despite the negative headline print, we were expecting stronger profit growth. Despite the modest pullback, at $2.87 trillion in the first quarter the level of profits is still consistent with elevated profitability with profits about 19% ahead of where they were prior to the pandemic in the fourth quarter of 2019 (Figure 3).

The detailed industry data lag a release, and will not be available until the third release of first quarter GDP on June 29, but the high-level details suggest profit growth was soft pretty much across the board. Domestic industries profits, which typically account for nearly 80% of profits, slipped 2.1%, driven lower by financial profits specifically. Domestic non-financial corporate (NFC) profits rose 2.8% to $1.8 trillion. We recently analyzed the ability of the NFC sector to service its debt amid higher interest rates, and sustained profitability in the sector would help offset higher borrowing costs as the Fed lifts rates. Foreign profits (remittances from foreign subsidiaries less remittances of American subsidiaries to foreign parents) slid 3.2% in the first quarter.

Author

Wells Fargo Research Team

Wells Fargo