RBA’s Lowe and RBNZ’s Wheeler on Trump, rates and currencies

In Q&A sessions this week, RBA Governor Lowe and RBNZ Governor Wheeler, one just beginning his tenor, the other coming to the end of his, provided some insights into how they view their economies, rates and exchange rate policies, and the isolationist rhetoric in the USA with Trump in the White House.

Faced with similar conditions, the RBNZ sounded cautious, while the RBA sounded cautiously optimistic. The RBNZ was more dovish seeing rates on hold for over 2-years and continues to talk down the NZD exchange rate. RBA’s Lowe was, perhaps to many, surprisingly sanguine about the AUD exchange rate.

RBNZ’s Wheeler considered protectionist trade policies in the USA as the biggest threat to global growth, citing research from the OECD. RBA’s Lowe noted that barriers were surely not the road to prosperity.

Lowe was also worried about signs that the US was withdrawing from global forums on financial stability, and criticized US administration officials for their comments on the yen, the yuan, and euro.

Lowe is a supporter of the G20 gatherings, noting on several occasions since becoming Governor that it has supported growth orientated policies, including infrastructure spending, reduced regulation, and tax reform. Lowe pointed out that, to some degree, these were Trump’s core domestic political message. If this were to serve as an example to others, like the Australian government, Lowe said this could be very good for global growth.

Seeing either a very good or a very bad outcome from the Trump administration, Lowe said he is in watch and wait mode. Trump has some good domestic economic policy, but destructive isolationist tendencies.

RBNZ Wheeler discussed how higher global interest rates would tighten financial conditions in New Zealand. Lowe outlined his concern over excessive household debt in Australia, stating why it would not be a good idea to cut rates further despite still low inflation. It is evident that both the Australian and New Zealand economies and currencies would be dampened in a rising global yield environment more so than most countries due to high household debt and regulatory changes that require banks to seek more long-term funding; a lot of it still coming from foreign sources.

RBNZ cautious, Lowe optimistic

The RBNZ and RBA policy statements appeared very similar; both essentially have a neutral policy bias and seem in no hurry to change policy. Both tend to think the next move in rates, while some time away, will be higher.

Even though both central banks are faced with similar conditions, the RBNZ sounded cautious, whereas the RBA sounded cautiously optimistic.

RBNZ Governor Wheeler said in his press conference that, “what we have adopted is very much a neutral bias…. If you go back to November we had an easing bias, a slight easing bias built into the forecast, because we had a 20% probability of a cut in the OCR built in, now we have removed that”. He further said that the risks of rates rising or falling are now “evenly balanced”.

RBNZ project more than two years of rates on hold

The RBNZ always provide specific rate projections over three years in its quarterly Monetary Policy Statement (MPS), unlike the RBA that does not.

The RBNZ forecast has no change in rates for more than two and a half years, and only one full 25bp hike at the end of its three-year forecast horizon (Q1-2020); which would be an unusual length of time with no change in rates.

Of course, this projection has a wide (unspecified) probability distribution around it, that gets much wider the further out the forecast, and is far from a commitment by the RBNZ. Nevertheless, the slow return to normal rates suggests the RBNZ remains relatively dovish.

RBNZ Wheeler gave weight to the dovish perception in his press conference. He said, “If you look out in the very longer term….in perhaps two years or more out, we might start to see, as the cycle matures further, that OCR increases may be needed, but we have built in one increase over that time”.

In response to a question on “if the market had got ahead of itself” in projecting rate hikes earlier this year. Wheeler took the bait and said, “We think the market assessment on rate hikes has got a bit ahead of itself”.

Assistant RBNZ Governor McDermott, the Head of Economics, and in the running to be the next Governor of the RBNZ, emphasized the reluctance to hike too early in a later interview, saying the RBNZ “wants to be sure of 2% inflation before hiking “ (according to Bloomberg news headlines).

Governor Wheeler has announced that he will leave after his 5-year term expires on 26 September, and Deputy Governor Grant Spencer has agreed to act in the Governor role for six months from September to March 2018, to allow the appointment of a new Governor to be held over until after the New Zealand Federal Election on 23 September (the date was announced by PM Bill English on 1 February).

We can only guess where the RBA might project rates over three years if they chose to. Presumably, they too would have them on hold for around a year, but perhaps not so much time as the RBNZ.

However, the RBA remain very reluctant to give much guidance. Apart from sounding neutral in its bias, there was no commitment to keeping rates steady. The RBNZ was much clearer that it prefers to wait for some time before adjusting rates.

Different views on exchange rates

This divergence is also apparent in their views on the exchange rate. The RBNZ persisted with its assessment that, “The exchange rate remains higher than is sustainable for balanced growth and, together with low global inflation, continues to generate negative inflation in the tradables sector. A decline in the exchange rate is needed.”

However, in his speech on Thursday, RBA Governor Lowe dismissed the suggestion (in a question from Bloomberg News) that the recent rebound in the AUD was a cause for concern. It appears that the level of the AUD is hardly registering on his radar.

Lowe said, “The way we ultimately judge this is whether the configuration of interest rates and the exchange rate we’ve got will deliver reasonable growth. And our central forecast at the moment is that they will deliver reasonable growth [3% over the next 2-years]. So it is hard to say that the exchange rate is fundamentally too high”

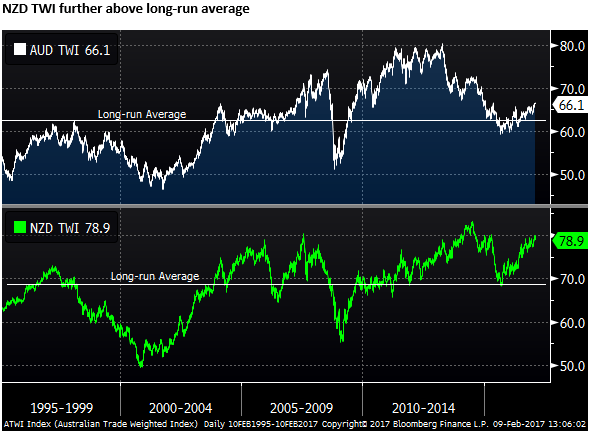

It is the case that, historically, the NZD looks further above average than the AUD, and thus the RBNZ might be more justified than the RBA in expressing additional concern over its exchange rate.

However, one wonders if the RBNZ is exaggerating a bit concerning its exchange rate comments. Wheeler was asked if intervention was under consideration. He gave his stock standard reply suggesting the topic was not given any serious discussion inside the RBNZ.

Lowe says commodity price rise is good, but not a major boost

In his Q&A on Thursday, Lowe said “the movement in our terms of trade is boosting our national income at the moment which is good news. It is pushing up equity prices and hopefully the government will get some more revenue, and it improves confidence in the economy. “

But he further said, “We are not expecting the rise in commodity prices to lead to much more investment. We’ve done so much investment in the resources sector, so unless the prices were to stay high for a long period of time I don’t think we will see a reinvigoration of investment.”

“We are expecting iron ore prices and coal prices to come back a bit as the supply adjusts. We are not expecting it to be a major boost to the economy, but it is helping. It’s a much better situation than it has been in the last four years when in each year it has been down down down.”

Wheeler sees risks from higher global yields

Wheeler noted that mortgage rates had risen in New Zealand since last year, despite no change in the RBNZ’s policy rate (OCR) and a stable rates outlook. This reflected the rise in long-term rates abroad pushing up New Zealand bank funding costs. This effect has become more pronounced in recent years because of the regulatory requirements on banks to rely on a greater share of long-term funding sources.

Wheeler said, “In terms of mortgage rates, what does it mean for that? You’ve seen fixed mortgage rates, say 2-year mortgage rates, increase by around half a percent”.

He said the “long-term outlook for mortgage rates will very much depend upon what happens to long-term interest rates, and that will very much depend on what happens globally, particularly in the US, and where the US goes in fiscal policy amongst other things.”

The same is true in Australia. Both countries are impacted by rising global bond yields, as their banks rely on a significant share of foreign-sourced funds and must maintain longer term funding books overall, both forcing them to issue longer-dated bonds and compete more aggressively for deposits.

As such, in a rising global yield environment, monetary conditions in Australia and New Zealand will tend to tighten, creating upward pressure on bank lending rates. It follows that the RBNZ and RBA will be less inclined to raise policy rates as yields abroad rise.

This is a reason to anticipate some under-performance in the AUD and NZD compared to the USD in a rising interest rate environment.

Furthermore, we are likely to see less focus by investors in searching for incrementally higher yields in currencies like the NZD and AUD, in a rising global yield environment. An additional reason to expect these currencies to weaken as yields globally rise.

A third reason is that Australian and New Zealand households are relatively highly indebted. As such, consumption and housing investment may lose momentum more quickly than in past episodes as mortgage rates rise.

In his press conference, in a discussion on risks, Wheeler noted potential upside risk to US bond yields related to Trump’s policies. He said, “risks out there in terms of bond markets and therefore interest rates is what the US does on fiscal policy in terms of the potential for tax cuts, infrastructure spending and increases in operating spending such as around the military and other things that have been identified.”

RBA Lowe more concerned by high household debt

RBA’s Lowe has shown more concern over high levels of household debt. For him, this is a reason to avoid further cuts and live with more prolonged undershooting of inflation. He made this point when quizzed in Q&A on Thursday about conditions in the housing market.

Lowe said he does not worry about the impact of a decline in housing prices on the stability of the banking system, because of the efforts of APRA and the banks themselves. He said, “Banks are quite resilient against even a quite bad scenario [large fall in house prices].”

However, he said, “The other consideration that is more concerning is not so much the run-up in house prices but the run-up in debt. At some point in the future the household sector may feel that the level of debt it too high, particularly if house prices were to come back.”

“And then consumption could be very weak for a period of time as household sought to rebuild their balance sheets. That is a consideration when thinking about monetary policy.”

“I don’t think it is in our interest to encourage people to borrow more, to push up house prices, even more, just to get a bit more growth this quarter or next, because I think we could, later on, come to rue the day that the level of debt went up even higher.”

“So that is a conversation we talk about at the Reserve Bank. And because our inflation target is a flexible medium-term one, we have the flexibility to take that into account. I want to make sure that over my seven years, just as [former Governor] Glenn did over his seven years that inflation averages two point something. I am confident we are going to do that, but we don’t feel compelled to push it back to 2.5 at the earliest opportunity if it comes at the cost of higher levels of debt.”

Protectionist Trump seen as the biggest risk

The RBNZ Governor was employed at the World Bank for 13 years before heading the RBNZ. As such, he has a considerable interest and understanding of global economic and policy developments. He described President Trump’s trade policies as the biggest potential risk to the global economy.

It wasn’t exactly clear if he meant the biggest risk out of all of Trump’s policies, or the biggest risk in a global context. But given the length of time he spoke about these risks it is certainly a significant new dynamic that Wheeler is concerned about.

He said, “If you go to the US, I think the biggest risk is primarily around protectionist policy. If you look at the statements around TPP, or TTIP, where these negotiations between Europe and the US about harmonization about standards, investment treaties and trade, which was really very promising under the Obama administration…, you look at the potential for the renegotiation of NAFTA, you could end up with a situation… of higher tariffs.”

“And what would that mean to the global economies? So let’s say for example that the US really did get serious about imposing 45% tariffs on China or large tariffs on Mexico, then that would have serious implications, I believe, for the global economy.”

“Because one thing it would do is raise inflation rates in the US, the Federal Reserve would need to push harder against rising inflation, so those interest rates would rise, the exchange rate in the US would probably rise, you’d see retaliation by other major countries.”

“And the OECD did some work on this recently, basically looking at what would be the impact if costs associated with trade, i.e. tariffs, were to rise by 10% in China, the US, and Europe. And not unexpectedly it led to a very significant slowdown in global growth.

“Higher costs associated with global trade reduced volumes of trade and slower growth in the rest of the world, which would certainly affect us.

“So the biggest risk is the protectionist risk, and it’s unfortunate that a lot of this rhetoric is taking place at a time when we’ve seen the slowest growth in merchandise trade volumes in the last five years than we have seen since the early 1980s.”

Lowe also highlighted the protectionist Trump agenda as a big risk to the global economy. He said, “If we do see a retreat from the international order, then the US economy will be weaker, and the world economy will be weaker. It surely can’t be the case that the way we build prosperity is to build barriers between one another.”

Lowe worried about other isolationist trends in the USA

Lowe was critical of the broader isolationist type agenda that appears to be gaining traction in the US with Trump in the White House.

He said, “One of the issues we face globally at the moment is that many central banks and governments have wanted lower currencies. We are starting to see this in the US now, with various parts of the US administration being concerned about the value of the yen and the yuan and the euro. It would be problematic for us and the world if currency manipulation were to be seen as a way to manipulate growth. I hope that doesn’t happen. But for us, the Australian dollar has been the great stabilizer.”

When asked about the possible rollback of Dodd-Frank, Lowe said, “Some adjustment to Dodd-Frank may be entirely sensible and may improve the efficiency of the system without impairing its stability.”

However, Lowe said, “It’s not the change in financial regulations that concerns me the most, it’s the possible retreat from an international rules based common system.”

He said, “If the US were to go its own way that may increase the incentive for Europe and others to go their own way. I think we would all suffer from that; we’d lose the level playing field, the system will become less efficient and more prone to arbitrage, as people tried to move funds around or businesses around to take advantage of that.”

“We don’t know if the US will ultimately move away from that, but you have seen in recent times the Federal Reserve and others being instructed not to participate in the international negotiations in foreign lands, which I think is problematic, if that takes us to a place where the US cannot be a part of the rules based international order.”

Lowe can see potential for Trump to inspire the G20 growth agenda

However, Lowe said he was in “watch and wait mode” on Trump’s global impact. He said, “It’s quite possible that the outcomes are good. Increased spending on infrastructure, reducing regulation and cutting corporate tax are things that the Group of 20 have been calling for to stimulate growth. To some degree that’s at the core of president Trump’s domestic political message. So if that works, and serves as an example to others, it could be very good for global growth.”

A theme that runs through Lowe’s responses is that he is a big believer in the positive influence on the global economy that arises from global gatherings like the G20 and the Financial Stability Board. Trump and his supporters in Congress appear to see global economic and financial cooperation as much lower importance than any previous administration in decades; seeming, in fact, to not care less.

Author

Greg Gibbs

Amplifying Global FX Capital

Greg has had a long career in foreign exchange. He began his career at the Reserve Bank of Australia in 1989 and in the early 1990s he was the first economics graduate at the Bank to be assigned to the foreign exchange dealing desk.