Rates will be higher for longer, exactly as Mr. Powell has been warning all along

Outlook: This is a week full of PMI’s, including ISM services in the US today. The WSJ reports the S&P services PMI is forecast at the same 51.1 in May as in April, while the ISM version will be a rise to 52.3 from 51.9 in April.

In the PMI sweepstakes, China is the laggard and Europe is doing better than anyone expected, but the US has some troublesome numbers, too. We also get durables and factory orders. On Wednesday it’s the trade deficit, which has a lot less power over currencies these days but has strong implications for growth when imports are robust.

Amid a vast rise in Treasury issuance this week, we get a somewhat mysterious report in the WSJ that big banks may have to raise capital requirements by 20%. Bloomberg summarizes the report: “Banks with at least $100 billion in assets may have to adhere to the new requirement, lower than the existing $250 billion threshold, for which regulators have reserved their most stringent rules, according to the report, which cited people it didn’t identify. Michael Barr, the Federal Reserve’s vice chair for supervision, has previously said US officials are reviewing bank capital requirements.” Meanwhile, the FT notes that US banks are dumping commercial real estate loans as fast as they can find buyers—see below.

We found some confusing talk about banks going whole-hog for the new Treasury issuance, which means less money available for lending—or it could mean the banks stop accessing the reserve repo market. At the same time, the Fed has never stopped engaging in QT at about $95 billion per month. Either way, this adds up to tightening by the back door even if the June hike gets skipped, as so widely expected. The question is whether these forms of tightening end up delivering a credit crunch.

Bottom line—rates will be higher for longer, exactly as Mr. Powell has been warning all along. The stock market is not wild about it, nor holders of gold. Here’s the funny thing—instead of a recession driving the Fed to cut rates in Q4 or Q1 2024, as expected up until Friday, we may well get a cut or at least expectations of a cut because inflation is coming down nicely enough. This is not what anyone expects today… just an idea from left field.

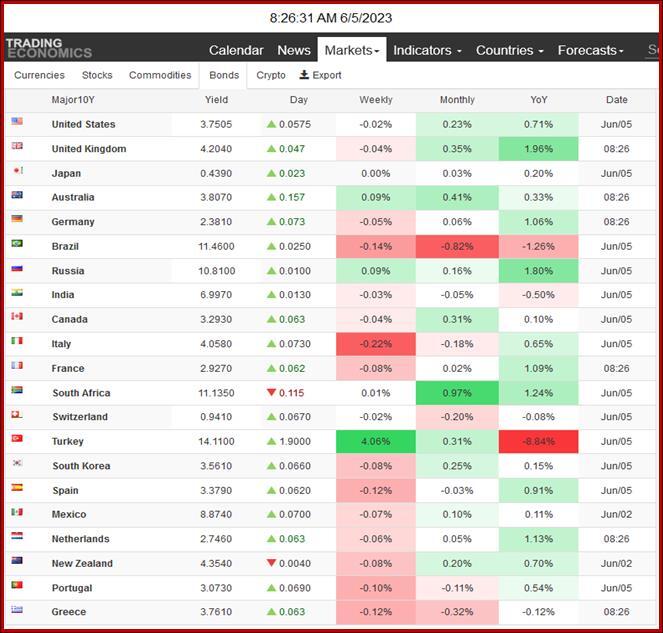

Forecast: We warned on Friday that the dollar rally might not be over, but did not expect payrolls to exceed forecasts by so much and bring so much repositioning with it. So far it looks like this is the version of risk assessment that holds good news is good news, not bad news. You’d think that a new forecast that shows a recession being averted would be risk-favorable and thus dollar-unfavorable, but that’s not what we are getting so far. A switcheroo in interpretation of riskiness is not uncommon but not to be trusted. Everyone’s 10-year yields are on the rise—for the day. See the y/y to get a better picture.

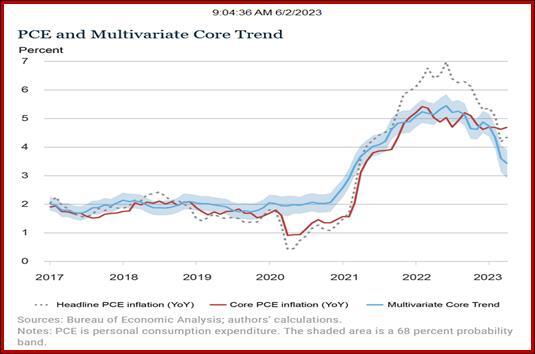

Inflation Tidbit: On Friday the NY Fed reported its “Multivariate Core Trend (MCT)” model showed a big drop in April to 3.4% from 3.6% in March (and March itself revised down from 4.5%), although the uncertainty is high. The purpose of the model is to measure the stickiness of inflation, aka “persistence.” So the persistent inflation is 3.4% while the raw headline core PCE is 4.7%.

Tidbit: It’s official—the US commercial property sector is in freefall. The top story in the online FT today is that a slew of named US banks are peddling commercial property loans at a deep discount, even when borrowers are in good standing, to get out of the sector. This time the banks actually read the newspaper and are aware of high vacancy rates and a grim outlook. They missed the boat on shopping centers two decades ago and the Fed’s series of rate hikes last year, but this time they think they in sync. It didn’t hurt that FDIC chief Gruenberg warned “that real estate loans — especially those backed by offices — face challenges if demand remains weak and ‘values continue to soften. These will be matters of ongoing supervisory attention by the FDIC.’”

Tidbit: The FT has a splendid story on the anti-monarchy guy who calls the royal family “tax-funded Kardashians.” He says arresting protesters is deeply un-democratic, along with all the pomp and ceremony, the appeal to tourism not a compelling argument. By the end of the story, the FT has refuted his arguments, but he does get the front page. One key point—Harry and Meghan are driving a big, fat wedge. Harry just appeared on “60 Minutes” to make his point, again, that the royal family’s secret deals with the tabloid press, aka leaking, is toxic and the press literally the cause of Princess Diana’s death. Never mind the French ambulance service delayed 45 minutes before arriving on the scene.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat