Rates spark: One million swallows should make a summer

Although large negative real yields have become the norm in core Europe, they were less common in the US. Covid-19 changed that. The re-opening should change that back, but so far it hasn't. A big payroll report followed by a near 4% inflation number next week should tip the balance. But then again, this bond market is proving to be a tough audience to please.

The Fed calms markets ahead of payrolls, but it does not need to. Bonds are snoozing. They shouldn't be though.

It is important to keep in mind that the Federal Reserve's current stance is outcome-based, not forecast-based. In recent days, Fed officials have come out to mark the taper discussion as something for after the summer at the earliest.

The bond market is trading with a large inflation expectation, but in a seemingly depressionary state - something must give

This adds to the growing disconnect between the macro backdrop and what rates markets are pricing. Eventually we think there has to be a realignment with nominal rates moving higher. Part of the reason that yields remain so calm is a genuine fear factor of what exactly awaits after the re-opening euphoria is complete, for example a year from now. What then? Some ask whether there is then the risk for a return to growth disappointment and inability to generate long lasting inflation.

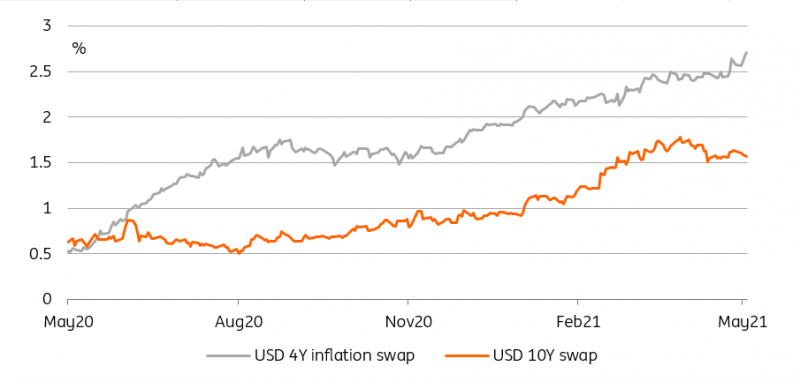

Short-term inflation outlook heats up but nominal rates remain depressed

Source: Refinitiv, ING

The Fed is waiting for the case favouring stubborn inflation uplift to be proven, and the bond market is doubting its own discount.

Remember, inflation expectations as discounted by the market are already high (e.g. discounting 2.8% inflation per annum for the next four years), so its a bit perverse for nominal yields to remain so low, and a refusal of nominal yields to rise is what is compressing real yields into deep negative yields space. And that remarkably is verging on a depressionary discount.

The offsetting argument is that strong demand for fixed income explains why bond yields are contained. But is that really it? Surely we need more.

All eyes will be on the US jobs data. How big is big?

The payrolls report is expected to show the addition of one million new jobs created in April - an extraordinary number in admittedly extraordinary times.

Will it change the immediate picture? Probably not. Fed chair Jerome Powell had indicated that he wants to see not just a couple of good data points but a series of good data. He’ll likely get a good one today, and indications after yesterday’s jobless claims data are that May could present a decent figure as well. And we'll get a near 4% inflation reading next week. Need more, bond market? Yes, it seems.

The Fed falling is behind the pack as the focus already shifts elsewhere

Other central banks have already turned their attention to tapering and tightening, such as the Bank of Canada or the Bank of England, who decided to cut the pace of asset purchases. Even in the Eurozone, the focus shifts towards phasing out the extraordinary crisis measures as the vaccine roll out and the recovery gain traction. EUR rates, for that matter, had underperformed yesterday; with 10-year Bund yields not joining the rally lower, the spread of 10-year USTs over Bunds remains just below 180 basis points.

The shift of focus may also be keeping spreads of Italian bonds over Bunds at elevated levels, now 114bp in the 10Y area. At least Italian bonds were one of the main beneficiaries when the crisis measures were implemented.

We think that simple view falls short of the mark as it ignores a changing backdrop not just domestically but also with regards to the potential further EU integration as political landscapes shift in Germany, for instance. Maybe not today, but going forward, the fiscal stimulus and reforms with the Draghi government could play out in improved bond ratings. Near-term factors that keep the spread elevated can also be found in upcoming bond auctions next week and the possibility of a long end syndicated bond issue in the coming weeks – it was long end BTPs in particular that underperformed yesterday.

Today’s events and market view

Regarding today’s US payrolls number, the Fed’s Powell has largely taken the excitement out of today’s anticipated strong reading as he will want to see a series of good readings before contemplating any changes. If anything, the risks are that a disappointment in the data could elicit a more robust market reaction with the first instinct for another move lower in rates. In a twisted way, that could prove short-lived if such an outcome helps to lift risk sentiment.

In supply, Belgium offers up to €0.5bn two bonds in its optional reverse inquiry facility.

Attention today will fall on the rating agency Moody's which has pencilled in a review of Italy’s Baa3 rating with a currently stable outlook.

Read the original analysis: Rates spark: One million swallows should make a summer

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.