Rates spark: No let up for now

There is no letup in the upward pressure on rates. While risk sentiment is deteriorating further, we saw inflation swaps coming off their elevated levels as well. Are we finally getting the medicine that was needed? Bund asset swaps remained calm despite wider sovereign spreads and a lower collateral supply outlook.

Rates pressure remains, but risk sentiment is souring

Following their rise at the start of the week, yields tested lower yesterday. But that rally proved short-lived, with the 10Y Bund yield ending the session above 2.8% again.

What remained of the day was a sense of risk-off again. Equities ending in the red and European sovereign spreads noticeably wider even when yield levels briefly dipped. The key spread of 10Y Italian bonds over the German Bund is now above 190bp, solidly back into the range that prevailed ahead of the summer. But the widening was not confined to Italy. We saw a widening in Greek and other periphery country spreads, though not quite as pronounced.

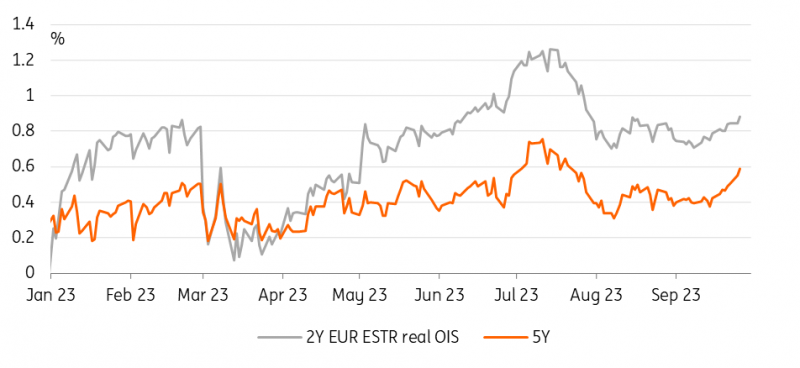

Perhaps it is the medicine that is needed. Real rates are on the rise again with the 5Y real ESTR OIS marching towards 0.6% – a level it had topped only briefly in July during this tightening cycle. Inflation swaps are coming off their highs, with the 5y5y inflation forward down another 2bp after Monday.

Perhaps more surprising against the backdrop of souring risk sentiment was the fact that Bund asset swap spreads (ASW) were little changed – typically, they are sensitive to risk-off. And even more notable as the German debt agency yesterday cut back the issuance targets for the fourth quarter by more than anticipated. Bond sales for the quarter were cut by €8 billion and Bubill sales by €23 billion.

There was only a very short-lived widening in the Bund ASWs on the lowered collateral supply prospects, but we have to acknowledge that the current conditions in markets for high-quality collateral appear rather benign judged by Bubills trading relatively inexpensive versus swaps. And going from a current Bubill outstanding stock of €155 billion to €148 billion by the end of the year as now pencilled into the new funding calendar is not a dramatic shift to prevailing conditions, even if the original plan was to bring the stock to €171 billion.

In terms of more direct impact, we also still have to wait for October when the Bundesbank ends remuneration of government deposits, which by the latest reading were around €38 billion at the end of last week. This could then still push into the collateral market. Note though that the debt agency itself has said its balances have already been shifted into the secured money market and are now close to zero.

Real rates are in the driving seat

Source: Refinitiv, ING

Read the original analysis: Rates spark: No let up for now

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.