Rates spark: Central bank palooza

Another day of heavy central bank action should keep markets busy. In the case of the BoE, we see no point in further hawkish warnings. The reaction should be a knee-jerk, and short-lived curve steepening.

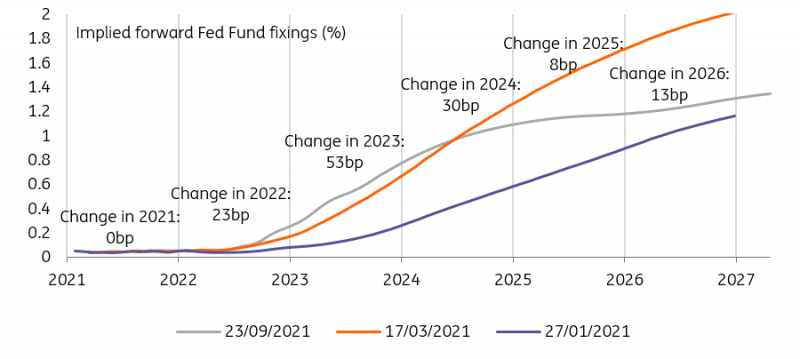

The Fed's dots have been shuffled forward, but the back end is asking some tough questions

The impact effect of the FOMC outcome was a mild ratchet higher on front end rates and a mild nudge lower in longer tenor rates. But there is also some volatility evident as the market digests that while nothing has actually changed, the timing of the first hike is now sooner and a more complete taper announcement is more probable from the November meeting. Risk assets seem quite unbothered about the Fed’s intentions, which is helping to mute any material bond market reaction. Even though risk assets have had a tough September to date, culminating in another layer of worry coming from China’s Evergrande, it has not caused the Fed to shy away from nodding approval towards the net improvement in the US economy.

The impact effect on rates is break lower in the 10yr yield, which even though driven by a fall in inflation expectations, does not gel with the more constructive macro outlook coming from the Fed. It seems that the long end is playing with the notion that the Fed is on a path towards a policy mistake if they were to tighten too soon. At the same time, the belly of the curve is still cheap to the wings, which is in fact maintaining a net bearish tilt, although flattening on the 2/5yr segment is muting this. The pull lower in longer tenor rates is coming from an easing lower in inflation breakevens. Real yields have not budged, but if there is to be a follow-through reversal upside test in market rates ahead it will likely come from real yields testing higher.

In the end, the 10yr is holding in the 1.3% area. It’s been at or about that level for a number of weeks now. It’s showing a mild vulnerability to the downside in yield as an impact outcome. A break lower here would not be very helpful, as it would be seen as pushing against the Fed. Remember, should the Fed want to hike rates at some point (and they will), the ideal starting point is a steep curve, or at the very least a decent gap between the funds rate and long end rates, as that’s what provides the room to push official rates higher. A taper will help, as it will stop the Fed buying of bonds, removing one of the bullish impulses that has helped to force market yields down.

The USD curve is projecting a more shallow hiking path than signalled by the Fed

Source: Refinitiv, ING

The Fed has also doubled the counterparty cap on the reverse repo facility from USD80bn to USD160bn. The volumes going into the facility hit a new high yesterday, and this move is a signal of direction of travel, ie, an indication that liquidity going into the facility are more likely to rise ahead. The debt ceiling remains an obstacle as it prevents the Treasury from coming in to mop up liquidity. It's also an indication that there is a lot of liquidity swashing around still. From a purely technical perspective, the sooner the taper comes the better.

BoE: Not labouring the point

Our economics team stresses that given the headwinds facing the UK economy over the winter months, including but not limited to fiscal tightening, higher energy prices, and end of the furlough scheme, it would be surprising for the BoE to insist on the risk of near-term policy tightening. Granted, more MPC members, perhaps even a majority, now see the conditions for future tightening as being met… but this doesn’t mean they will imminently. Another argument for not labouring the point is that the curve is already pricing a fair amount of tightening, including a first hike as early as 1Q 2022 (the February meeting realistically).

Some curve steepening is possible today but should prove short-lived

Source: Refinitiv, ING

The same arguments holds for longer interest rates. The aggressive flattening seen since the summer implies that markets think the end of this tightening cycle is in sight. A lack of hawkish warnings, or simply of endorsement of market pricing, should result in a knee-jerk re-steepening of the curve. We doubt this will be sustained however. Our economics team calls for the first hike to occur within a year, and agree that the terminal rate should be roughly similar to the previous cycle. Unless either change in the market’s mind, the GBP curve should remain flat.

Read the original analysis: Rates spark: Central bank palooza

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.