Rates spark: Carry on worrying

As the dust settles, the implications of the ECB and Fed June meetings are subtle. EUR rates should be shielded to an extent from a hawkish Fed but, if the outlook deteriorates, long-end rates will continue falling. This is a bond market that refuses to bow to contemporaneous macro circumstances, and in fact sees something nasty down the line.

Despite the Fed, monetary conditions in fact have loosened when you look at the fall in the 30yr rate

Some USD 756bn went back to the Fed on the reverse repo facility yesterday, a new record high - so much for the technical hikes of 5bp. These do affect the price of liquidity (on the reverse repo and excess reserve buckets), but do nothing to address the excess of liquidity, which continues to grow.

The 10yr is now below where it was before the Fed, in sub-1.5% territory again. It's not all about excess liquidity, but clearly there is a rump of liquidity outside of that, which filters into the fixed income market. In addition the fall in nominal rates is coming entirely from a fall in inflation expectations. Real yields are practically static - the 10yr is still deep negative at -75bp, but doing nothing.

In contrast inflation expectations dropped from over 2.3% to almost 2.2%, pulling nominal rates down with them, or at least coinciding with the fall in nominal rates. The 5yr area is still cheapening to the curve, but the dominant move is coming from the back end; the 10/30yr is almost 20bp flatter in a few days.

Post Fed reation is morphing into a monetary loosening coming from the 30yr

Having had an implied monetary tightening on higher 30yr mortgage rates, that is morphing into a definite monetary loosening as 30yr rates head ever lower. This is a bond market that continues to refuse to bow to contemporaneous macro circumstances, and seems to insist that it sees something nasty down the line.

A hawkish Fed and dimmer outlook are reflected in a flatter curve, and lower inflation swaps

-637596006309940903.PNG)

FOMC and bottlenecks all point to flatter curves

Going forward, the implications are more subtle than they first seem. Firstly, it will take time for markets to wholeheartedly shift the narrative to seeing signs of inflation as putting upward pressure on rates, by way of higher Fed tightening probability. Secondly, this apparent shift in Fed tone comes at a time markets are increasingly cautious about the outlook.

The Fed played no small part in this but the resulting reaction might well be that long-end rates decline further to price an early end to the recovery, precipitated by the Fed. This would go a long way to explain the fact that long-dated US rates more than retraced their post-FOMC sell-off yesterday. The other factor might be worries about the Delta Covid-19 variant spreading quickly among one of the most vaccinated populations in the world, or further threat to global supply chains from bottlenecks in China.

The subtle implications for EUR rates

Starting with the market implications of recent central bank events, the Fed has very much thrown a spanner in the works to investors gearing up to a quiet summer dominated by carry-chasing behaviour. On the face of it, it looks like a major risk to the status quo has materialised. In practice, the implications are more subtle. The ECB’s tone one week prior served as a major endorsement to low volatility/carry-chasing strategies. This hasn’t changed.

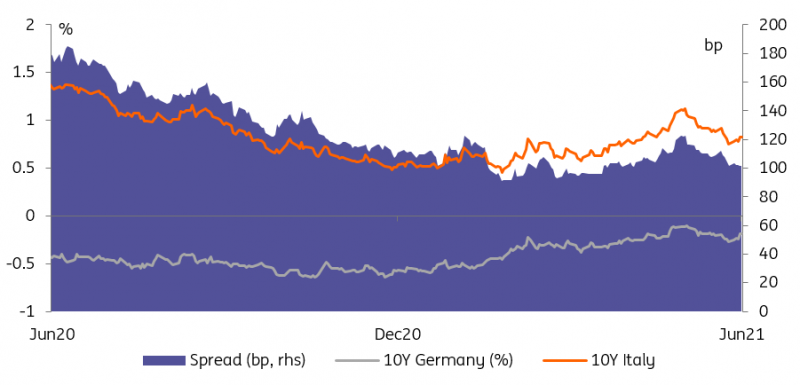

We expect the ECB’s dovish tone, even in the face of greater optimism, to shield European markets to some of the effects of a more hawkish Fed. This is particularly true in higher yielding bond markets where spreads offer a buffer against rises in risk-free rates. Our view seems confirmed by the mechanical tightening observed post-FOMC between Italian and German yields. It helps that the former might benefit from improved growth expectations.

Higher yielding EUR debt has weathered the Fed's change of tone, we expect tighter spreads still

Source: Refinitiv, ING

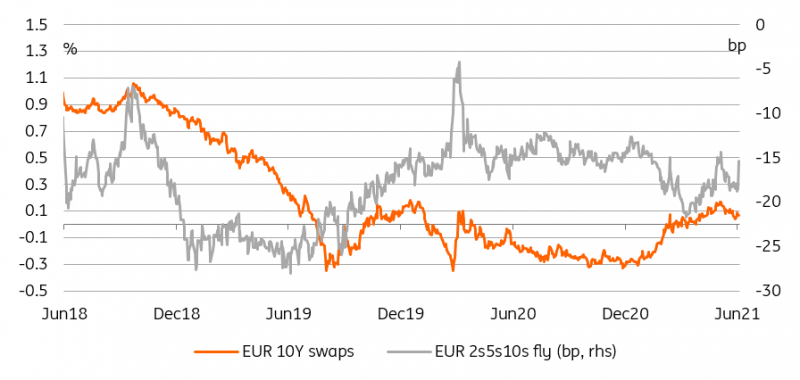

At the safer end of the credit spectrum, regular readers will know our view that EUR rates are still on a rising path, albeit gentle. A more hawkish Fed adds to our conviction although the way it manifests itself on the curve might seem disconnected with the outlook for monetary policy in the Eurozone. For instance, the steepening of EUR 2s5s and cheapening of EUR 2s5s10s both indicate the markets do see a read-cross to the path for EUR rates, even if the ECB has indicated it will be comparatively patient.

The main impact on the EUR curve has been a greater ECB hike discount

Source: Refinitiv, ING

Read the original analysis: Rates spark: Carry on worrying

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.