Rates spark: Banking stresses ease, inflation stresses won’t do so easily

Some relief that the Fed's emergency facilities were not further drawn upon in the past week is good. We're not out of the woods yet though, and further flight into money market funds point to some residual deposit flight from small banks. US PCE data today is set to remind us that the US is still a 5% inflation economy. Could be worse, but still not good enough.

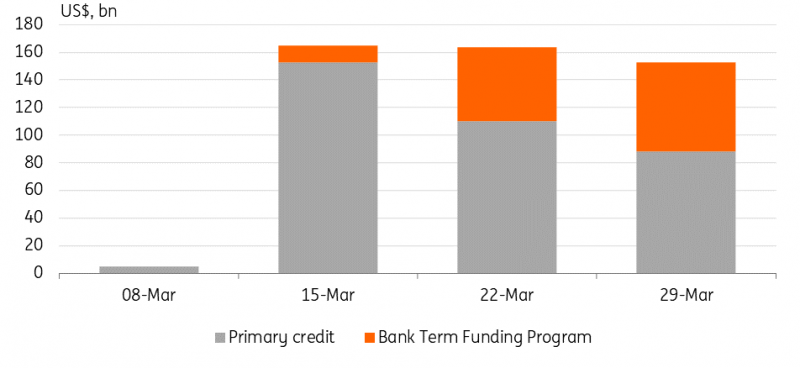

Use of the Fed's emergency facilities holds steady, and money market inflows slow

Borrowing at the discount window is down for the latest week, which is good. It's down to US$153bn, from US$164bn in the previous week.

Given that this is regarded as an emergency window, falls here are positive, even if the absolute number is still quite high. This was offset by a practically equal and opposite rise in use of the Bank Term Funding Program, which rose to US$64bn, compared with US$54bn for the previous week. So overall use of the Fed's emergency liquidity facilities is overall flat to the previous week.

Bottom line, no material wind down of use of emergency facilities, but importantly no evidence of increased panic, at least on this measure. Fed FDIC bridge loans were also flat on the previous week at US$180bn, which is less of a surprise, as there has been no material change here, given that no further deposits have required resolution. The Fed's foreign repo facility also eased lower in usage, from US$60bn to US$55bn. Overall decent data; no rise in level of angst.

There has also been a US$66bn inflow to US money market funds in the past week. This can suggest ongoing deposit outflows from small banks. That said this week's money market inflow is less than the inflow seen in the previous week, which was US$118bn.

Inflow volume to US money market funds has practically halved

So the overall inflow volume to money market funds has practically halved, although there was less of a fall-off of flows into Government Funds, as Prime Funds (essentially non-government funds) saw another week of (mild) outflows. It seems that flows into Government Money Market Funds are an ongoing consequence of deposit outflows from small banks. And at least it's slowing.

Market rates have not been up to much of late, but today's PCE data will be key. Market expectations for 0.3% month-on-month on headline and 0.4% MoM on core remain far too high for comfort. At least the Fed can get some solace from no material deterioration in the banking stresses, but the stress of inflation has not gone away. This is one of the reasons for market rates holding up recently, and for that 10yr to prefer to target the 3.5% area rather than breaking back down towards 3%.

Fed balance sheet data shows a gradual shift to long-term funding support

Source: Federal Reserve, ING

Macro data moves back into focus, but with differing impact

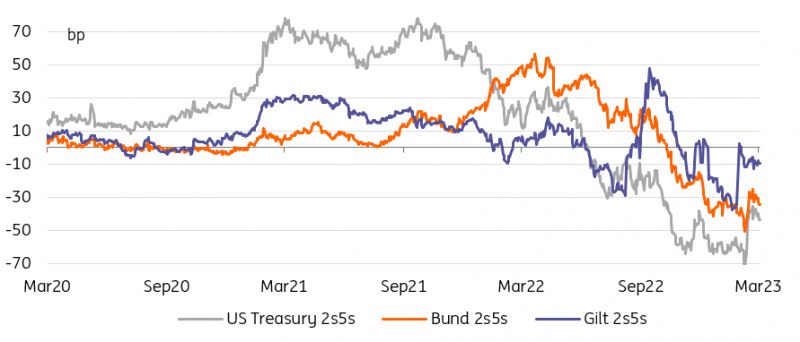

For EUR rates the CPI data starting with yesterday’s releases from Germany and Spain was a reminder that the European Central Bank is still not yet at target. As hikes get priced back in – the terminal rate notched up again towards 3.5% – we also witnessed a notable re-flattening of the 2s10s Bund curve which touched -40bp yesterday.

Data will be the focus for the US in the upcoming week shortened by the Easter holidays. It will kick off with the ISM manufacturing on Monday, but attention will then switch to the labour market, starting with the JOLTS job openings (for February) on Tuesday, and culminating in the US non-farm payrolls on Good Friday. In between the market will also have to digest the ISM services.

The question is to what degree the US market will be ready to lean into any robust data, given that it is already reckoning with an impending credit crunch which will likely make itself felt only gradually in the data. As for lingering banking stress, the still elevated reliance of the system on the Fed and further inflows into money market funds pointing to ongoing reshuffling of deposits will keep markets cautious of data that has yet to fully react to the turmoil.

The front-end of yield curves (2s5s) can re-flatten temporarily on good data, especially in Europe

Source: Refinitiv, ING

USD markets' reaction is increasingly asymmetric to data

US markets have been slower to adjust Fed pricing higher again as the worst of the turmoil has passed. The Fed is only seen pushing through one more hike at most. To be fair the Fed itself is not signalling more in its dot plot, but for the rest of the year the focus has pretty much shifted to rate cuts – 50bp from peak to year end are more than fully priced. Just ahead of the turmoil markets were eyeing maybe the possibility of one 25bp cut.

US markets could be more reactive to any signs of deterioration

With the focus having shifted that much to worries about the gradually unfolding real economic impact of the financial stress, we believe that reaction to this week’s data could be asymmetric. In the sense that going forward US markets could be more keen to jump on any signs of deterioration, while better data could easily be put aside as dated and not yet reflecting the additional tightening of financial conditions.

Read the original analysis: Rates spark: Banking stresses ease, inflation stresses won’t do so easily

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.