Progressive – Auto insurance share increased, stock price will increase too?

FY20 has been an amazing year for Progressive Corporation, with record increases in net profit and pretty much all other relevant metrics. The insurance company has enjoyed the results for the same reason others in the sector have: An increase in investment holdings and fewer claims. However, with market conditions expected to return to normal, we are doubtful if the company can duplicate these results in the future. What’s worse, it seems that the company is about to fall even beyond its FY19 levels.

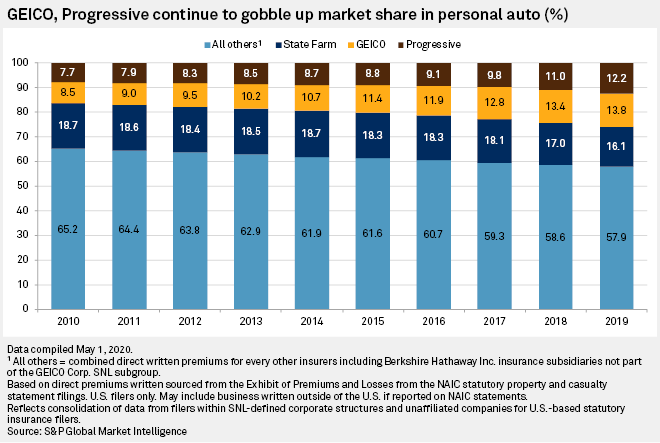

Progressive has been increasing its market share in the auto industry, defeating the big boys in the process. Even before COVID, the company was doing well. COVID, however, has provided amazing results. Source: S&P Global.

COVID-19 to the rescue

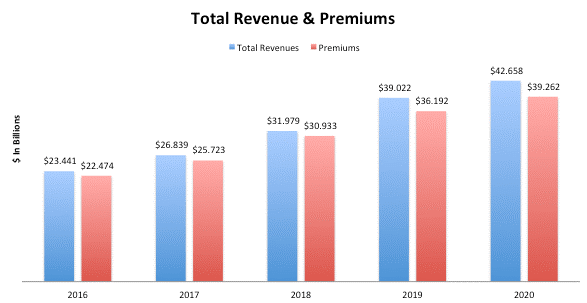

Over the last few years, the company has been able to enjoy a strong financial performance. Revenues went from $32.5 billion in FY18 to over $40.5 billion in FY20. However, this was on the back of its auto and property insurance business. The pandemic further nudged the performance, as a fall in the total number of vehicles on the road leading to fewer auto insurance claims.

On top of this, insurance companies usually invest excess cash in a wide variety of assets. With asset prices going up across the board during FY20, the company could pump up its numbers further. To be fair, COVID is not the only reason the company has been doing well. In the three years before 2019, the company increased its share in the auto insurance industry from 9.1% to 12%, a huge leap in an industry considered to be immensely fragmented.

The company is also very well-diversified. It can leverage its large product base to cross-sell customers on various kinds of insurance. As such, the company can enjoy a benefit in the industry that few others (apart from the major players) can.

The company has a history of growth and increasing margins. Operating margin surged from just over 10% in FY18 to over 18% in FY22. Sadly, it seems that the party may be coming to an end.

The company’s investments have begun producing a bigger share of the company’s total revenue since FY19. However, with the market state being what it is, we do not think that can continue. Source: SeekingAlpha.

The curse of success

With the effects of COVID waning off, the markets are in a completely different state. Inflationary pressures mean that fixed-income investments, which form the vast majority of the portfolio of insurance companies, will not perform as well as they did previously. On top of that, the reduction in claims that inflated FY20 numbers cannot continue as the number of vehicles on the road return to normal; people start going to the doctors more often and find other ways to file insurance claims.

This is quite evident in the consensus estimates. For FY21, the company is expected to generate upwards of $45 billion in revenue, but the net profit is expected to fall from $5.7 billion to around $3.4 billion. The revenue is expected to increase, but the fat margins are expected to starve, hampering net profit in the process. The picture for FY22 is even worse, with a projected net profit of $3.1 billion.

For FY19 and FY20, the company was valued at around 10x its earnings. Even prior to that, the company has almost always been valued at less than 15x times its annual profit. However, forward estimates show the company being valued at 17x its FY22 price. Not bad if Progressive was a tech company, but terrible numbers considering that Progressive is in the insurance business.

So, if the financials can’t, can the dividend make the company a worthwhile investment? Let’s find out!

The erratic dividend

Historically, the main aspect of Progressive that analysts have had a problem with has been its dividend. The dividend has been all over the place. Most insurance companies offer a small but consistent dividend with slight growth. This way, the company can continue to offer a modest dividend even through bad times.

On the other hand, Progressive has a dividend that increases during the good times, falls during the bad times (but it sometimes doesn’t), and goes all over the place in its frequency.

The simplest way to predict the dividend is this: If the company performs badly over the next few years, expect the dividend to fall. The overall dividend for FY19 was $2.65, and for FY20, it was $4.90. It is simply impossible for the company to match that unless it can deliver a similar performance. All indicators point to the fact that it cannot. With a possible recession looming, expect the company to reduce its dividend drastically.

Simply put, the company cannot continue its current performance, and we expect the share price to suffer. However, the underlying business is solid. It’s just that the company is overpriced. As such, the company would be very interesting after a correction, but it seems like a bad bargain right now.

Author

Baruch Silvermann

The Smart Investor

Baruch Silvermann is a personal finance expert, investor for more than 15 years, digital marketer and founder of The Smart Investor.