Poland’s labour market remains resilient, but a delayed slowdown impact is emerging

Polish wage growth continued at a double-digit pace in April. Meanwhile, the average paid employment contracted 0.4% YoY in April as demand for labour showed a delayed reaction to the slow economic growth seen in 2023. Still, supply-side constraints are prevailing in the labour market.

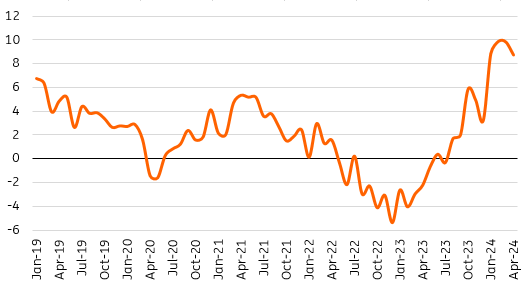

Averages wages and salaries in the enterprise sector rose 11.3% year-on-year in April, i.e., slightly slower than consensus (12.1%), after growing by 12.0% YoY in the previous month. In real terms, annual wage growth has stayed close the top since the late 1990s and early 2000s. Wage pressures are fuelled by very low unemployment (with Labour Force Survey unemployment at its lowest level in the EU, equal to the Czech Republic), as well as regulatory changes such as a very high minimum wage hike.

Real wages growth remains elevated

Real wage and salary in enterprise sector, %YoY.

Source: GUS, ING.

At the same time, some divisions of manufacturing are showing signs of softer demand for labour. Its negative impact on wages is still overshadowed by the minimum wage hike. Revenues from social benefits and wages in the public sector are rising rapidly. As a result, domestic demand remains strong enough that a large deterioration in the condition of the labour market has not occurred. Therefore, wage growth remains elevated.

A decline in the average paid employment deepened to 0.4% YoY (consensus: -0.3%), after -0.2% YoY in March. Although with a considerable lag, employment levels are gradually responding to the weaker economy we've seen in 2023 – but the magnitude of the deterioration is negligible. For the time being, the most pronounced job declines are being recorded by some export industries and are offset by rising employment in other domestic companies, or created by FDIs.

Limited labour supply is the main barrier to employment growth rather than low demand for workers. The number of vacancies per unemployed person has not deteriorated, showing resilient demand for labour. Companies are reluctant to cut jobs, fearing that they will not be able to find employees when economic growth accelerates further.

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.