Oil market daily: Feast or famine

- The oil market was priced for a smooth normalization, but Hormuz is behaving more like a cracked artery than a reopened highway.

- The attacks matter less for the barrels immediately lost and more for the confidence lost among shipowners, insurers and cargo buyers.

- Revoking the Iranian waiver threatens the economic heart of the interim deal just as tanker attacks threaten its security foundation.

- The short oil trade remains vulnerable because the market has been selling surplus barrels while underpricing the risk that those barrels cannot move freely.

Feast or famine

Oil’s feast-or-famine market was handed a very different menu overnight.

For days, the trade had been built around the idea that the worst of the Hormuz shock was behind us: traffic was creeping back, stranded barrels would eventually find a home, Iranian exports would resume under the interim arrangement, and the war premium would continue leaking out of the front end of the curve. The market had started to treat the Strait less like a live battlefield and more like a badly delayed shipping lane.

Then the sea reminded everyone who was really in charge.

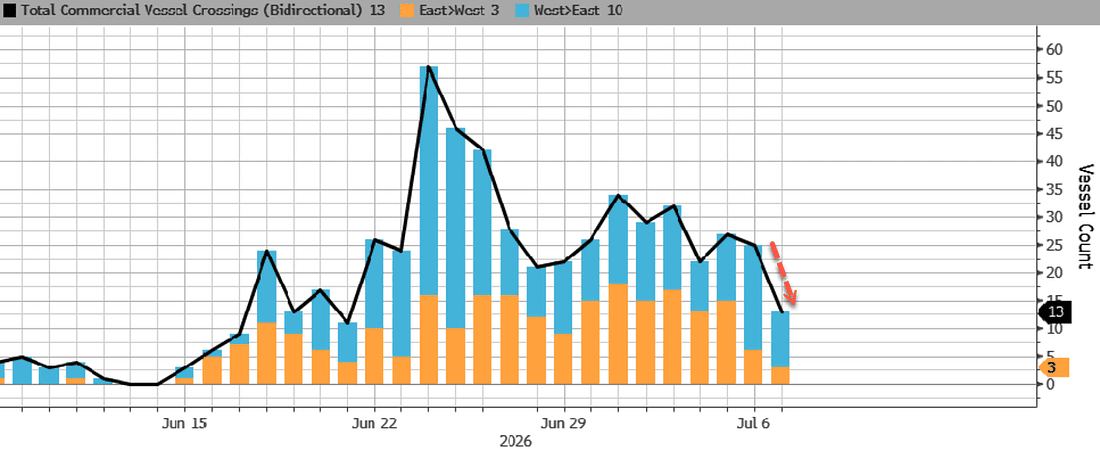

Fresh attacks on commercial vessels in the Strait of Hormuz, including strikes involving a Qatari LNG tanker, a Saudi crude tanker and another unidentified ship reportedly hit by a drone, pushed the maritime threat level to “severe.” The Red Sea also saw another security incident, adding to the sense that the region’s energy arteries are not reopening in a straight line but are instead being tested, one vessel at a time.

The latest Bloomberg ship-tracking data show vessel traffic through the Hormuz is declining today.

WTI pushed back above $72 and Brent climbed towards $76, but this was not simply a crude rally. It was a positioning event colliding with physical reality. The oil market had become heavily short because the bearish story was easy to tell: more supply, more stranded cargoes eventually clearing, more Iranian barrels, and a fading geopolitical premium. But markets built around an orderly normalization tend to wobble when the underlying map still has missiles flying over it.

Speculative positioning had become heavily tilted toward a return of surplus barrels, leaving crude exposed when the physical-risk narrative abruptly returned.

Zero hedge

The point is not that Hormuz has to close outright for oil to catch a bid. It only takes shipowners to hesitate, insurers to sharply reprice risk and crews to start second-guessing the route. A strait can remain technically open while becoming commercially dysfunctional. That is the grey zone confronting traders now: the channel may still be navigable, but it is no longer a normal trade corridor. It is beginning to resemble a toll road with IRGC snipers positioned around the overpasses.

That distinction matters because the physical market is not a Bloomberg headline. It is captains, insurers, charterers, refiners and cargo owners all deciding whether the risk-adjusted economics still work. Once that confidence starts to erode, the disruption spreads well beyond the ships that are actually struck. It affects loading schedules, delivery windows, regional differentials, freight costs, LNG balances and the willingness of buyers to commit to cargoes that may arrive late, damaged or not at all.

Hormuz may be open on paper, but shipping is increasingly split between normal lanes and a narrow risk-managed corridor — leaving every transit dependent on confidence, insurance and individual captaincy.

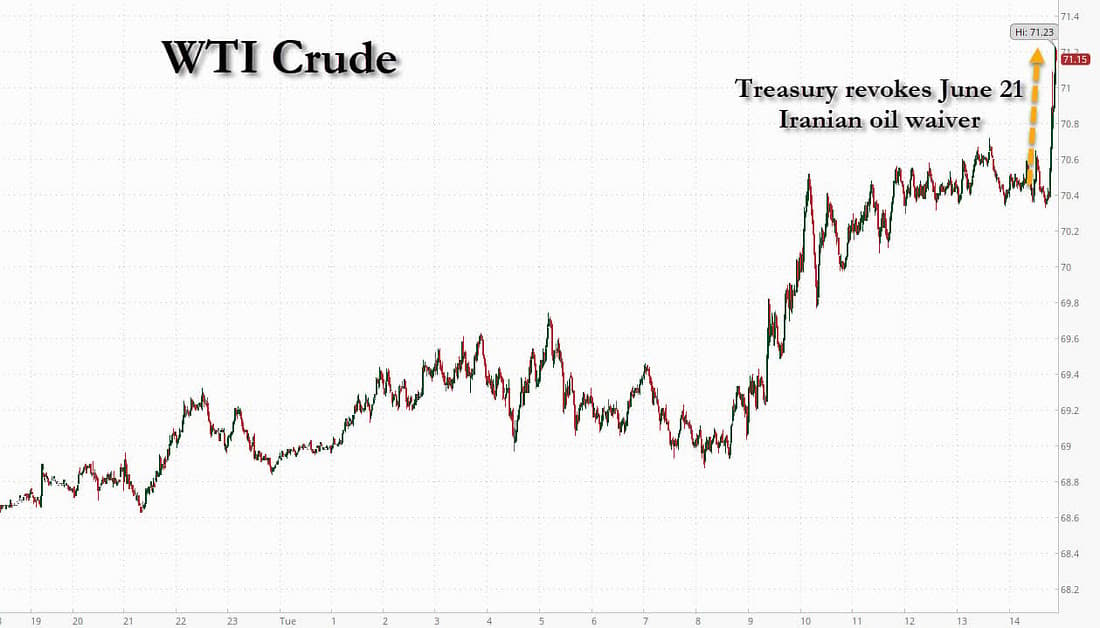

Late in the session, Washington added a second layer of risk by revoking the June 21 Iranian oil waiver. That was the headline that turned an already nervous market into a more meaningful short-covering event.

The waiver was not just a diplomatic courtesy. It was the economic anchor of the interim US-Iran arrangement. Iran was being allowed to sell oil and repatriate revenue, while Washington sought safer passage through Hormuz and a 60-day runway toward a wider nuclear agreement. Tehran got access to money. The US got the prospect of energy flows moving without missiles and drones shadowing every tanker crossing.

Treasury’s decision now ties those two things together explicitly. If Iran cannot guarantee the passage of commercial shipping, Iran cannot expect to retain the financial benefit of sanctions relief. That leaves both sides standing on a far narrower ledge. Iran wants the revenue. Washington wants the free flow of energy. At the moment, neither side appears to be getting what it thought it had secured.

The danger is that the ceasefire starts to look less like a settlement and more like a temporary pause between bargaining rounds. The attacks test the maritime side of the agreement. Revoking the waiver tests the economic side. Neither issue can be separated cleanly from the other, because both sit at the heart of the same bargain.

There is also a more tactical issue for oil traders. The bearish consensus had become too comfortable with the idea that Iranian exports, Gulf flows and global supply would normalize quickly enough to overwhelm any lingering risk premium. But normalization is not a switch that can be flicked back on from Washington or Tehran. It is more like reopening a railway after a derailment: the tracks may be technically repaired, but traffic does not instantly return to schedule while everyone is still wondering whether the next train will make it through.

That is why the rally matters. It is not yet proof that the oil market has suddenly become structurally tight. There are still plenty of barrels in the system, and the supply-glut argument has not disappeared. But the market is now being forced to reprice the gap between theoretical supply and deliverable supply. Crude sitting on a balance sheet, floating offshore, or trapped behind a maritime risk premium is not the same as crude moving smoothly into a refinery system.

For now, the market sits in the awkward middle ground between, and until shipping confidence genuinely returns, every fresh incident has the potential to turn an overcrowded bearish trade into another violent squeeze higher.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.