New US tariffs target Asia, but some countries stand to gain

President Trump’s new tariffs are higher than expected for most Asian economies. Moreover, most countries will face additional tariff rates on transshipments. The new announcements are silent on Singapore, India and the Philippines, which might stand to benefit from tariff concessions if negotiations progress favourably.

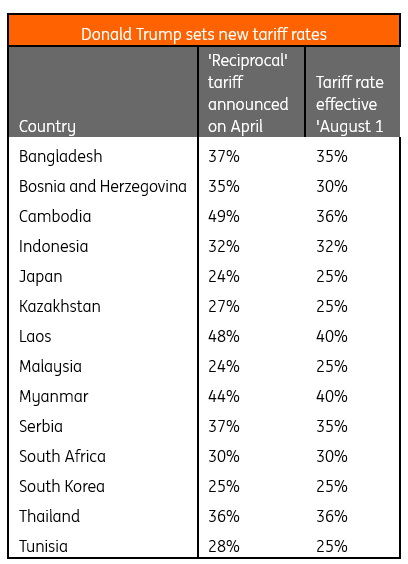

Asia has once again been hit hard with a fresh set of tariff rates announced by President Trump, set to take effect on 1 August. Out of the 14 countries that received tariff letters, nine were in Asia. While there is some respite in terms of reciprocal tariffs being pushed out by about three weeks, most countries are now facing higher or similar rates than those announced on Liberation Day. Here are our key takeaways:

-

The overall outcome is clearly worse than expected. Only three countries in Asia – Cambodia, Bangladesh and Laos – received tariff rates which were lower than on 'Liberation Day'. Despite lower rates, they remain high and penalising in the 35-40% range, much higher than the 20% Vietnam got.

-

These steeper tariffs may reflect Trump’s growing frustration with stalled negotiations with certain countries like Japan, Korea, Thailand and Malaysia, which all received a higher or unchanged tariff rate.

-

More importantly, they seem to signal a broader strategy targeting Asia’s trade links with China – particularly transshipment practices. The letters indicate that transhipped goods will be subject to higher tariffs, but there’s no mention of the rate that’ll be applied.

Interestingly, countries like India, Singapore, and the Philippines, which are not on the new tariff list, may be closer to finalising trade deals with the US, potentially giving them a competitive edge.

Overall assessment: a worse-than-expected outcome for Asia

Tariff rates that are higher than the 10% baseline are a worse-than-expected outcome for Asia, unless we see successfully negotiated deals over the next three weeks. Sector tariffs on autos and semiconductors, in addition to base tariff rates, will be more negative for Northeast Asia, including Taiwan, Korea, and Japan.

We are beginning to see signs of a pullback in exports in several Asian economies, after a good frontloading run in March-April. We had already factored in this expected slowdown into our outlook. However, our earlier assumptions were based on a 10% tariff rate. But tariffs remain a major swing factor, and the new higher tariff rates would imply that export growth could slow more sharply in the months ahead, with higher tariffs impacting global demand and rising business uncertainty.

Tariffs on transshipments, on top the new tariff rates, could be more negative for ASEAN

Within ASEAN, tariffs on Thailand and Indonesia remain elevated – unchanged at 36% and 32%, respectively. Indonesia is relatively insulated due to its domestic demand-driven economy, with only about 10% of its exports destined for the US. In contrast, Thailand is more exposed, given its higher trade dependence and stronger economic ties with the US, making it more vulnerable to prolonged tariff pressure, especially amid ongoing domestic political tensions.

Malaysia saw a modest increase in tariffs, from 24% to 25%. While still positioned in the middle of the pack, Malaysia retains room for further negotiation, potentially softening the impact if diplomatic efforts prove successful.

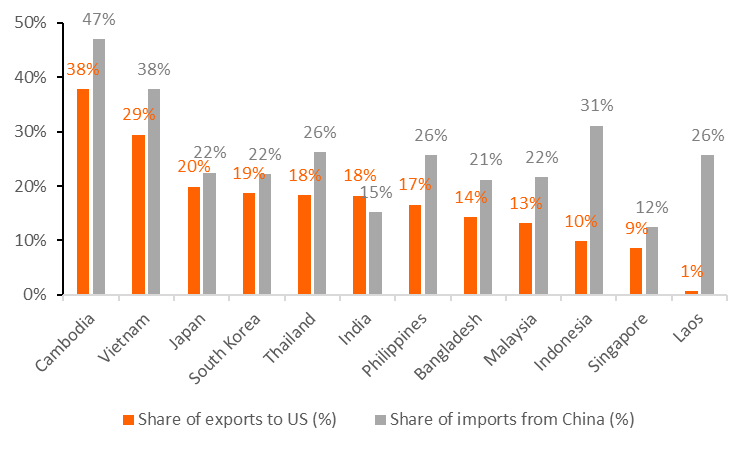

It remains to be seen how transshipments will be defined, but the letters issued yesterday indicate that, like Vietnam, most countries will face additional tariff rates on transshipments. The recent surge in ASEAN imports from China suggests that supply chains are deeply intertwined. While some companies might be diverting goods through ASEAN to avoid tariffs, other genuine ones export foreign components to ASEAN where the actual value added takes place. If transshipments were to include the latter, the negative impact on ASEAN could be more significant, and we’d need to reassess our projections.

Asia's growing reliance on China under scrutiny

Source: CEIC

India is likely next in line for a trade deal with the US

President Trump on Monday said that the US is very close to making a deal with India. India was one of the first countries to begin trade negotiations with the US, which appeared to have been going well. However, India has recently taken a firmer stance on offering tariff concessions to the US in politically and economically sensitive sectors such as agriculture and dairy. Differences also remain on steel (50%), aluminium (50%) and auto (25%) tariffs.

We think the two countries can conclude a deal soon if India allows for a few concessions on agriculture imports, allowing imports of some genetically modified US farm products while also agreeing to increase LNG imports from the US.

No new tariffs and a steady 10% rate favour Singapore’s trade-driven economy

Singapore and the Philippines were the only two ASEAN countries that did not receive a tariff notification letter from President Trump on Monday. Notably, these two also have the lowest reciprocal tariff rates – 10% for Singapore and 17% for the Philippines.

Singapore, in particular, stands to benefit significantly if the 10% rate is maintained. As one of the most trade-dependent economies in the region, preserving low-tariff access to the US market is critical. Additionally, the US currently runs a trade surplus with Singapore, and Singapore has the lowest reliance on Chinese imports among its regional peers. These factors enhance the likelihood of Singapore securing a concessionary or preferential tariff arrangement going forward.

Philippines – Tariff concessions key to electronics export growth

The Philippines has indicated that it is working toward a “mutually beneficial framework” for trade with the United States. The US remains a vital export destination, accounting for roughly 17% of the Philippines’ total exports as of 2024. A significant portion – about 53% – of these exports are electronic products, a sector in which the Philippines competes directly with countries like Vietnam and India for US market share.

Given this context, any reduction or concession on the current 17% reciprocal tariff rate would give the Philippines a competitive edge, particularly in electronics, and strengthen its position against regional peers.

Read the original analysis: New US tariffs target Asia, but some countries stand to gain

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.