Moody’s US debt downgrade hints at further “sell America” trade

Bond credit ratings agencies had not been in the news for some time until Moody’s surprised investors on Friday. The agency, one of the Big Three credit rating evaluators, downgraded the United States sovereign bond credit from its prime Aaa rating to Aa1.

Moody’s downgrade is the last one of the Big Three, since S&P Global Ratings had already trimmed the US sovereign debt rating back in 2011 in the aftermath of the Great Financial Crisis, and Fitch Group did the same in August 2023.

The news triggered a US bond sell-off on Monday. US 30-Year Treasury yields, the ones with the longest maturity date issued by the US Department of the Treasury, spiked to 5%, very close to the 5.08% multi-decade high they reached in October 2023, before retreating somewhat and closing at 4.91%.

US 30-Year Treasury bond yields (source: CNBC)

The credit rating agency also changed the outlook of the US public debt, issued through Treasury bonds and securities, from negative to stable, so markets should not expect further downgrades in the immediate future. Nonetheless, the damage is done.

Moody’s: Large US fiscal deficits aren’t going anywhere

Moody’s explained the decision to cut its rating on US debt due to “successive US administrations and Congress having failed to agree on measures to reverse annual fiscal deficits and growing interest costs.” The agency “does not believe that multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration.”

The agency also added that over the next decade, larger deficits are expected as spending rises while government revenue remains broadly flat. Moody’s expects “the US’ fiscal performance to deteriorate relative to its own past and compared to other highly-rated sovereigns.” Basically, the US “debt problem” is unlikely to be solved anytime soon and other countries are doing better.

The US sovereign bond downgrade is another flashing sign of the precarious US fiscal situation. Even if US Treasury Secretary Scott Bessent tried to minimize the news by saying, “credit ratings are lagging indicators,” Moody’s mentioned in their press releases that their base case is an addition of around $4 trillion to the federal fiscal primary deficit (which excludes interest payments) over the next decade.

Those figures are not far from official estimations. The current Trump administration is pushing for its Republican trademark tax cut plans, and the US Congress is currently debating a tax and spending bill that could cost up to $3.8 trillion to American taxpayers, according to a report by the Joint Committee on Taxation.

Elon Musk’s DOGE won’t fix US fiscal issues

Any of these scenarios adds a burden to the US fiscal balance that dwarfs the savings achieved by the Elon Musk-led Department of Government Efficiency (DOGE). During the last month of the Presidential campaign, Musk pledged to cut “at least $2 trillion” from the federal government budget. Over time, that target was repeatedly revised downward, first to $1 trillion and then $150 billion by April. According to the DOGE website, the current estimated savings from their actions amount to $170 billion.

The imbalance between the promises made by President Trump and his ally, Elon Musk, during the campaign highlights the overwhelming challenge that fixing the long-term trajectory of the US fiscal deficit represents. Politicians don’t have the incentives to enact policies to fix such kinds of deficits, which often include cuts in spending and tax increases, as these actions will likely get them out of office by the next election.

“Sell America” trade dynamics are likely to continue

George Saravelos, from Deutsche Bank Research, reflects this conundrum in his latest newsletter: “Whatever the Republican Congress decides to do with fiscal policy, it will most likely be ‘locked in’ for the remainder of the decade. The very difficult reconciliation process and the potential loss of a Republican majority in the mid-terms essentially leaves space for only one major fiscal event during the current Trump administration.”

The “sell America” trade that came into effect after Donald Trump’s tariff announcement triggered a rare combination of sell-offs in US stocks, the US Dollar, and the US Treasury bonds at the same time. It reflected a change of paradigm in global financial markets, adding fuel to those who argue that US financial assets are losing their safe-haven status.

What about market implications?

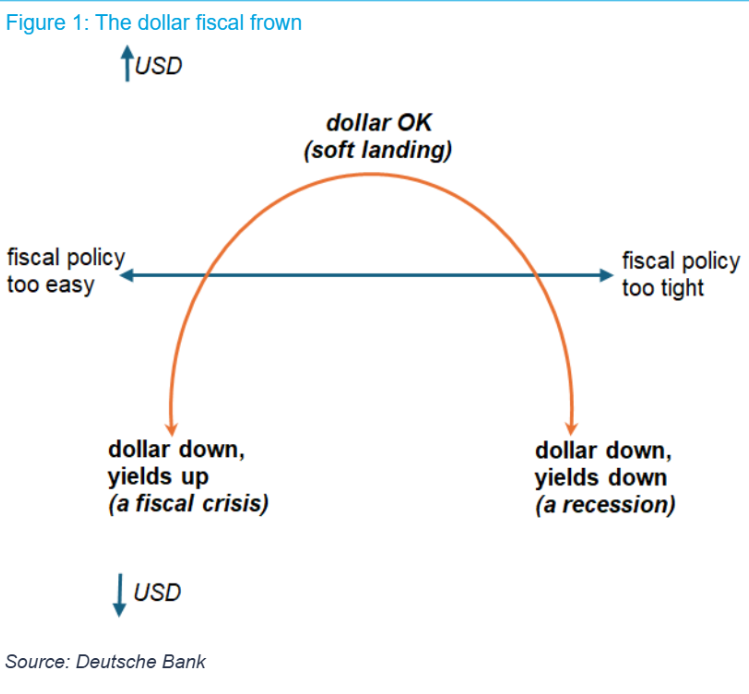

Deutsche Bank’s Saravelos presents a tricky outlook for the US Dollar: The scenario of an easy fiscal stance, without deficit cuts and continued spending, would lead to a combined drop in US bonds and the US Dollar, as it happened recently. “The persistence of this pattern would be a clear signal that the market is losing its appetite to fund America's deficits,” he says.

However, a quick reduction in deficits and debt piles would likely trigger a recession and force the Federal Reserve to cut rates. “In this more conventional world, the Dollar drops and bond yields rally at the same time,” he adds.

Not the best outlook ahead for an ailing US Dollar.

Author

Jordi Martínez

FXStreet

Jordi Martínez is the Editor in Chief at FXStreet, leading editorial operations at the company, before being promoted to the role in 2023, he worked in several editorial positions at FXStreet, including roles as Senior Editor and