Markets rebound after US-Iran deal

The beginning of the week in the financial markets is developing under a narrative of easing of geopolitical uncertainty after the US-Iran deal, which was signed during the weekend.

After a volatile macro stretch earlier in June, sentiment is partially recovering: the combination of events, such as successful SpaceX debut, a peaceful agreement between the US and Iran, and the FOMC meeting on Wednesday, might improve the risk appetite this week.

Major stock indices have continued to trade near elevated levels, supported primarily by

AI-linked names and a broader appetite for growth. The SpaceX IPO has added a fresh wave of risk-on energy to the Nasdaq as it is included in the Nasdaq and Russell2000 index, even as bond yields are reluctant to change yet, as traders prepare for Kevin Warsh's first policy decision as Fed chair.

SpaceX: The largest IPO in history

The dominant market event of the past week was the public debut of Space Exploration Technologies Corp. (SPCX). The company priced its offering at $135 per share, raising approximately $75 billion — the largest initial public offering in US stock-market history — at a fully diluted valuation near $1.77 trillion.

Two features of the deal stand out for market structure. First, retail participation was unusually high: roughly 20–30% of the offering was allocated to everyday investors — well above the typical 5–10% retail slice for mega-cap IPOs. Second, SpaceX may be fast-tracked for inclusion in major indices such as the Nasdaq-100, creating a potential pipeline of passive-fund buying in the weeks ahead.

US–Iran peace talks - The relief rally

Alongside the IPO headlines, the main event in the market is a peaceful agreement between the US and Iran, which was negotiated on Sunday, June 14th. The Hormuz straight will be reopened for traffic at the end of this week - officials from US and Iran will meet in Switzerland on June 19 to sign official documents. So, there’s still some uncertainty around the situation, and markets have many concerns, but the most dominant risk is eliminated from the markets now.

Inflationary pressure still may persist as the oil demand from China will revolver and that might give another inflation uptick to the world’s economy.

This event is expected to trigger a familiar chain reaction: crude oil would face downward pressure (which already started to happen), bond yields at the long end could ease modestly, risk appetite would improve across cyclical sectors, and the US dollar could soften modestly in a peace-premium unwind.

However, the improvement of risk appetite probably will be limited, as higher yields persist and interest rate expectations point to hawkish scenarios until the year for most countries.

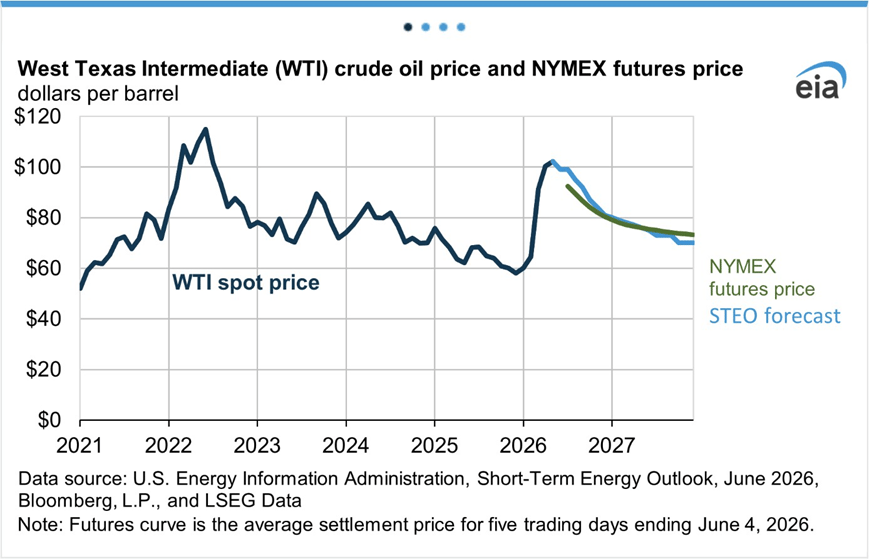

The short-term energy outlook from eia.gov points to a $80 per barrel for oil futures by the year end, so Crude oil futures might have limited capacity for the decline in the near future.

WTI Crude oil — STEO forecast. Source: eia.gov

The Fed decision on Wednesday

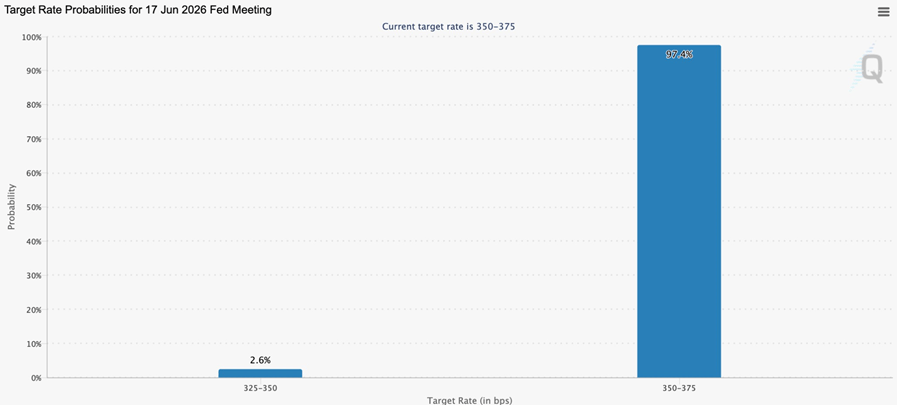

The centrepiece of the week is the FOMC meeting on June 16–17, with the rate decision and updated economic projections due on Wednesday, June 17. This will be Kevin Warsh's first meeting as Fed chair, giving the event outsized importance for both the statement language and the dot plot.

Markets broadly expect the Fed to hold rates unchanged at the June meeting. CME FedWatch assigns a probability above 95% to no change on Wednesday. The real intrigue lies in the forward guidance and the median dot — whether the Committee signals a higher-for-longer path or opens the door to rate increases later in 2026.

A hawkish surprise could pressure duration-sensitive equities and revive dollar strength.

Fed policy expectations — ahead of June 17 FOMC. Source: CME FedWatch Tool

News in focus this week

- Wednesday, June 17: FOMC rate decision, dot plot and press conference — dominant event risk for all asset classes.

- Thursday, June 18: BOE’s interest rate decision.

- Friday, June 19: Japan’s inflation rate.

Now let's shift to potential scenarios and trading ideas for the week ahead.

Gold

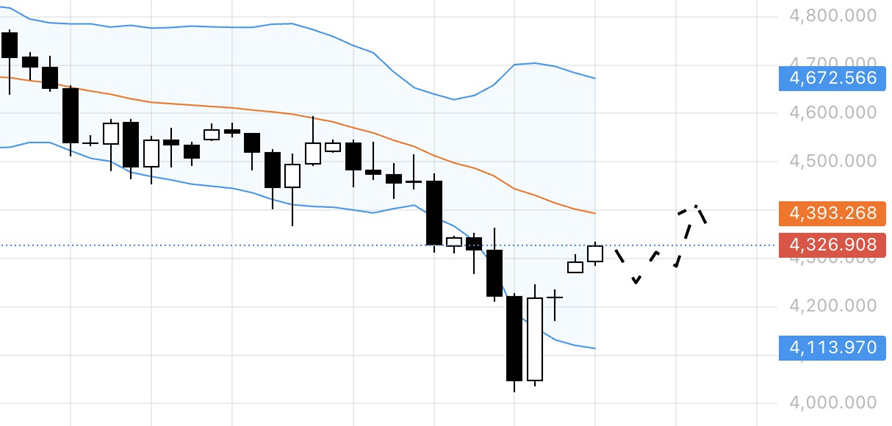

The US dollar is under pressure this week after the deal with US and Iran during the weekend. That might pressure yields of 30-year bonds and give gold fuel to recover.

Gold is moving in the upswing and has probably reached its local peak, but after a short consolidation or a pullback, it may continue climbing back to the dynamics resistance area of 4400. The price pulls back from the lower band of the Bollinger Bands, with the Relative Strength index also recovering from the oversold zone.

The main narrative affecting this trade is the potential improvement of market sentiment after the deal with US and Iran, which would mean open Hormuz straight and resolution of the energy crisis. That might provoke pullback for the US government bonds and pressure Gold prices higher.

XAUUSD, D1. Source: Exness.com

HK50

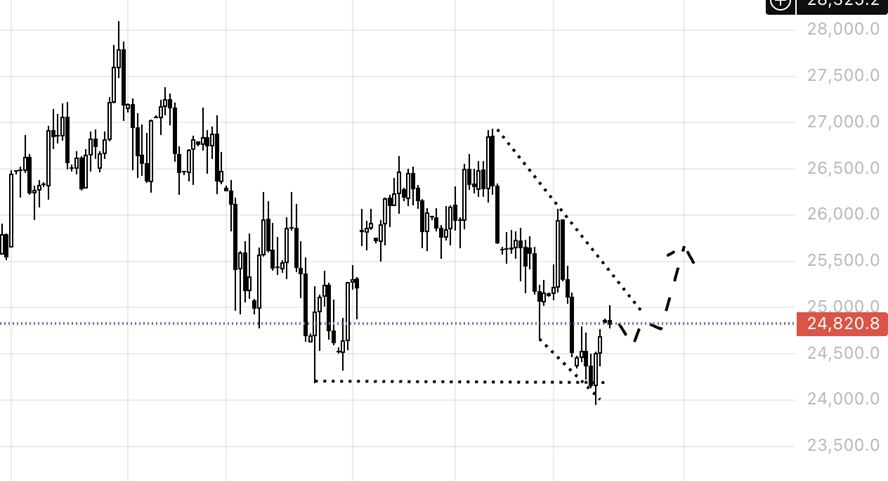

The possible idea of a long position might be initiated for the Hang Seng index, as Chinese markets might revive after the recovery of traffic in the Hormuz strait. While HK50 looks rather technically weak now, it might rebound and emerge from the descending channel if the correctional dynamics continue

Hang Seng index (HK50), daily chart. Source: Exness.com

Author

Stanislav Bernukhov

Exness

Born in 1980, Stanislav graduated from the university in 2003. He worked in the music industry and ran his own business ventures before being introduced to trading in 2004.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)