Market update: Equities and currencies gain as Omicron worries wane

-

USD (USDIndex 96.15) steady, as Treasuries rose sharply on the improvement in risk appetite on expectations for an acceleration in QE tapering to be announced at next week’s FOMC meeting, and as the market set up for this week’s $112 bln in coupon supply. Stock market sentiment strengthened further overnight and the GER30 and UK100 are posting gains of 0.6% and 0.2% respectively, while a 0.7% rise in the USA100 is leading US futures higher.

-

The RBA left policy settings unchanged, but sounded relatively optimistic on the virus front, which for some signalled that an early exit from QE is on the cards.

-

Growing confidence that Omicron won’t derail the global recovery, but that also means that central banks remain on course to rein in stimulus as new virus restrictions will likely add to inflation pressures.

-

Today’s released UK BRC retail sales were stronger than expected, but may be distorted by warnings that consumers should bring forward Christmas shopping in the light of supply chain disruptions, which could worsen over the winter.

-

US Yields 10-year rate lifted 1.7 bp to 1.45% overnight, JGB rates are up 1.7 bp at 0.051% as stock market sentiment continued to improve. Australia’s 10-year jumped 6.5 bp to 1.64%.

-

USOil – higher above 200-DMA at $70.60 – concerns about the impact of the Omicron variant on global fuel demand eased, while Iran nuclear talks stalled, delaying the return of Iranian crude.

-

FX markets – EURUSD remains below the 1.13 mark, while Cable is still below 1.33 as the FOMC decision comes into view. USDJPY lifted to 113.72, but currently 113.58.

European Open – The March 10-year Bund future is down -50 ticks, underperforming versus Treasuries and leaving Bund yields to jump sharply in catch up trade, after Treasury yields continued to move higher through the Asian session.

Today – The calendar has Eurozone detailed GDP numbers for Q3, but the focus will be on German ZEW investor confidence. In the US session, we have US trade and productivity and Canadian Ivey PMI.

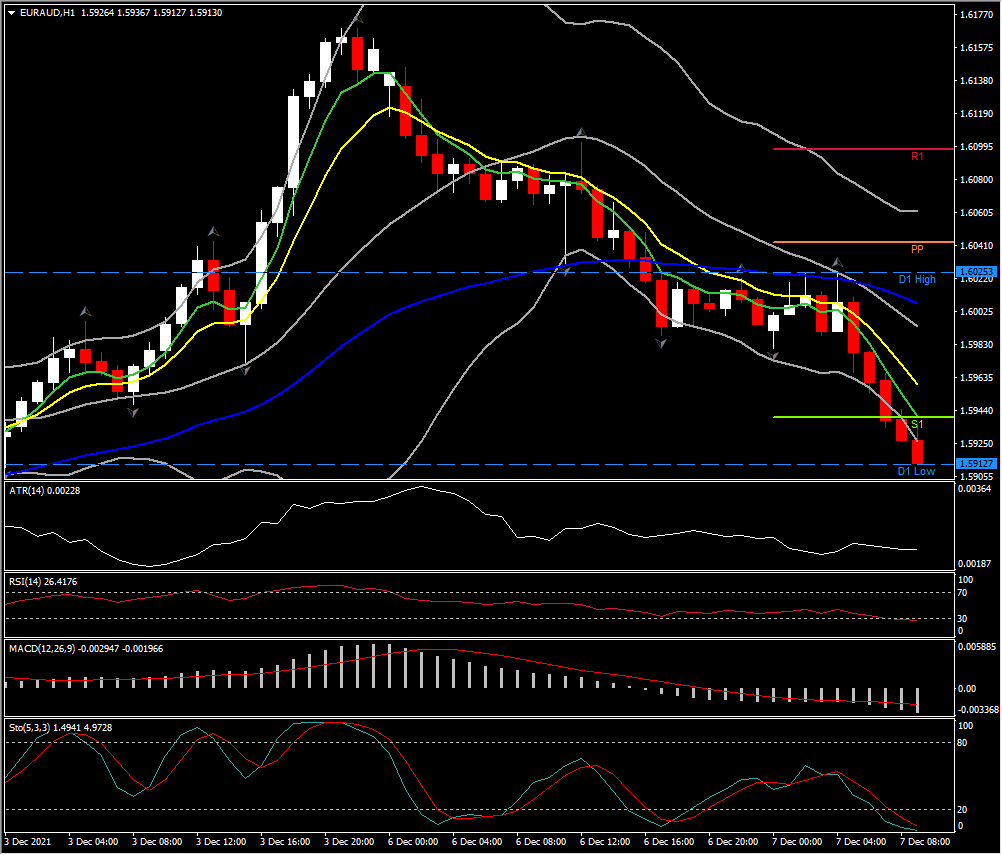

Biggest FX Mover @ (07:30 GMT) EURAUD (-0.41%) Currently MAs are aligned lower, MACD signal line & histogram below 0 and dipping, RSI sloping to 26, Stochastic declines. H1 ATR 0.00226, Daily 0.01442.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in