Market update: Taper gets a boost and transitory gets “retired”

Powell “retires” Transitory in light of Omicron & surprisingly suggests faster taper – Stocks tank, Dollar & yields rise on faster tightening expectations.

-

USD (USDIndex 95.90) back down from leap to 96.60 on Powell testimony. Saw fresh wave of risk aversion as Treasuries sold off, yields spiked (particularly the 2yr), Stocks fell significantly with USA100 down over -2.4% (APPL bucked the trend +3.16%) USA500 -1.90% (-88pts) 4567 & USA30 off 652 pts or -1.86%. Consumer confidence saw a slump in the headline, and a rise to a 13-year high in the inflation component. The Chicago PMI fell to 61.8. Home prices increased to fresh record peaks.

-

US Yields 10-year rates were down over 7 bps to 1.41% before closing at 1.443% before recovring to 1.468% now.

-

Asian Markets – Equities – Topix and Nikkei are currently up 0.4%, the Hang Seng bounced 1.1% and the CSI 300 is up 0.1%. The ASX, which outperformed yesterday, dropped back -0.3%. Data over night – Japan’s manufacturing PMI came in stronger than expected and while China’s private PMI reading signalled stagnation at 49.9, that was compensated somewhat by the stronger than expected official manufacturing PMI released yesterday. AUD GDP was not as bad as expected -1.9% vs -2.7% & 0.7% last time.

-

USOil – continues under pressure, down to $64.08 (14-week lows) yesterday – recovered to test $68.00 today – expectations continue to grow that OPEC+, will put on hold plans to add 400,000 barrels per day (bpd) of supply in January at their meeting tomorrow.

-

Gold finally some intra-day volatility – Powell surprise spiked to $1808 – before testing $1770 with a couple of hours, back to $1788 now.

-

FX markets – Yen rallied USDJPY dipped to 112.50, back to 113.40 now, EURUSD now 1.1326 & Cable steadied to 1.3300-1.3330.

European Open – December 10-yr Bund future down -11 ticks at 172.26, slightly outperforming versus Treasury futures. Central bankers may be getting more nervous about inflation outlook, but Omicron clearly is clouding over growth outlook & in Europe at least that will boost the arguments of the cautious camp at the central banks. US yields remain firmly below the levels seen before the new virus variant hit the headlines & sentiment is likely to remain jittery, even if stocks are set to back up from yesterday’s lows, with DAX & FTSE 100 future posting gains of 0.9% and 0.7% respectively & a 1.4% jump in the NASDAQ leading US futures higher. Data releases today kicked off with a big miss for German Retail sales (-0.3% vs 1.0%), higher UK house prices & firmer CPI from CHF.

Today – PMIs (EZ & UK),US Markit Final Manufacturing PMIs, US ADP and ISM Manufacturing PMI, JTC and OPEC meetings, BoE’s Bailey and Fed’s Powell & Yellen testify.

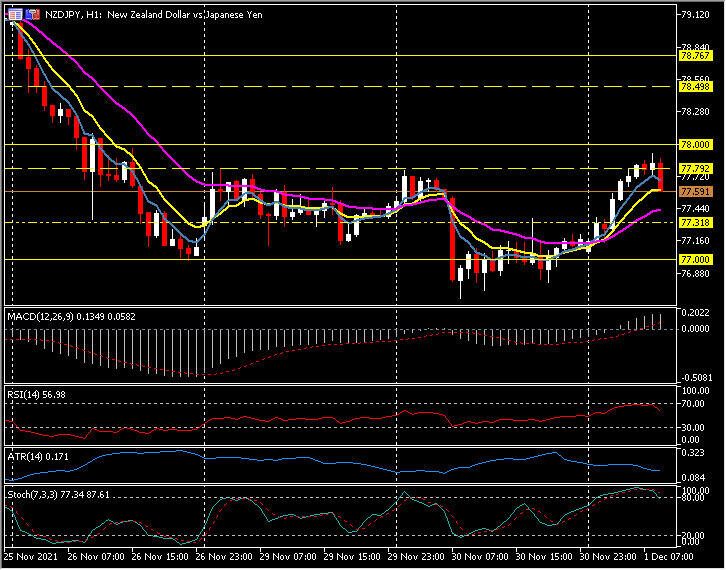

Biggest FX Mover @ (07:30 GMT) NZDJPY (+0.60%) Risk-sensitive currencies remain volatile, from a slide to 76.65 yesterday, today a rally to 77.80. Currently MAs aligned higher, MACD signal line & histogram over 0 and rising, RSI dipping from 70.00 at 58, Stochastic remain OB. H1 ATR 0.172, Daily 0.84.

Author

With over 25 years experience working for a host of globally recognized organisations in the City of London, Stuart Cowell is a passionate advocate of keeping things simple, doing what is probable and understanding how the news, c