Market update: Gold back under $4,000

Gold back under $4,000. War premium gone from oil markets. A volatile week for tech stocks amid AI bubble fears. Apple hit hard after raising its prices. Space X becomes the first company to lose $1trillion in market cap. Micron (MU.US) flying on blockbuster earnings. USDJPY sitting at its highest level in 40 years; yen ripe for intervention? Bitcoin under $60k. Perhaps most pertinently, traders are determining whether or not Warsh was just talking a big game or if he will back it up with hikes. Whatever your preferred asset class, markets are anything but dull at the moment.

A dove in hawk's clothing?

As previously discussed, the new Fed chair Kevin Warsh came out of the gates hawkish. His debut address drove further increased expectations for rate hikes and in turn asset reallocations. By talking tough first time out, Warsh has established himself as credible and unaffected by politics. But was it for show; was there an element of performance? If we zoom out, most of the indicators and measures employed by central bankers are back where they were pre-war, and that now includes oil (USOIL) prices. As such it won't take much for Warsh to turn much more dovish next time out. Or is this a complete misread? Is the new chairman intent on bringing inflation back down to 2%? Next month's meeting will be deserving of the popcorn.

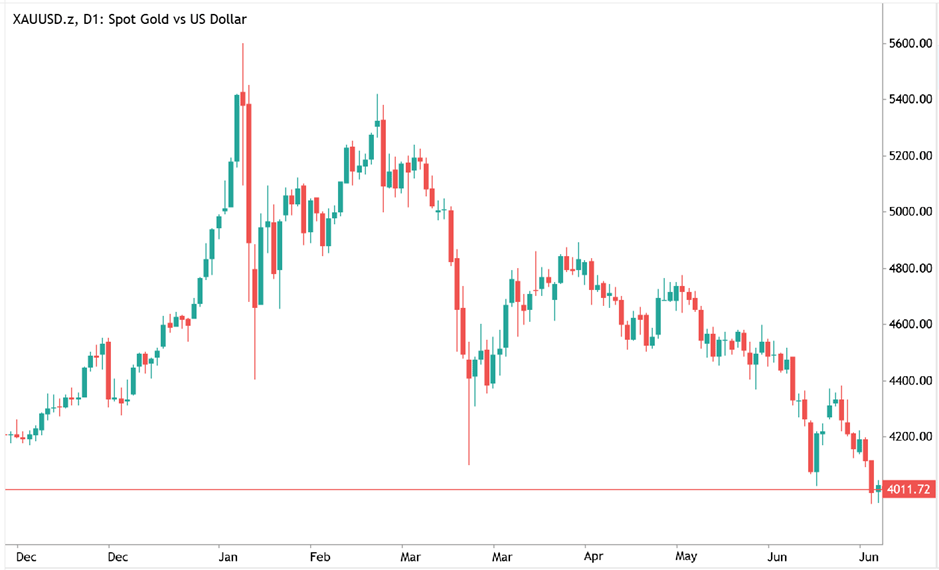

Gold through $4k

Gold (XAUUSD) slid almost 4% yesterday, notably closing below the $4,000 level for the first time since last November. The precious metal finished the session down 28% from its peak in January. Central bank purchases of gold continue to ramp back up, giving hope to more bullish traders, but that has not been enough to outweigh the outflows elsewhere. ETFs backed by gold have continued to sell, as investors reallocate funds.

The war in Iran has overall been a headwind for metal prices. Crude oil markets have been remarkably resilient throughout the conflict, given a 3–4-month closure of the Strait of Hormuz was seen as something of a worst-case scenario. Nonetheless a higher dollar and higher real energy costs have added fuel to already high inflation measures around the world. The resultant rate hikes have then motivated investors to move investments to yield-bearing assets. This trend was accelerated by incoming Fed chairman Warsh and his warning of more hikes to come.

So where to from here for metals? Several banks have reduced their target prices, but still see gold finishing the year significantly higher than current levels. Prominent analysts feel that rate hike expectations are overblown at present, a key factor in a relief rally from here. Goldman Sachs is calling for a bounce to $4,900 at year-end. Either way the volatility that short-term traders enjoy appears likely to continue as we enter the third quarter.

Mars ain't the kind of place to raise your kids

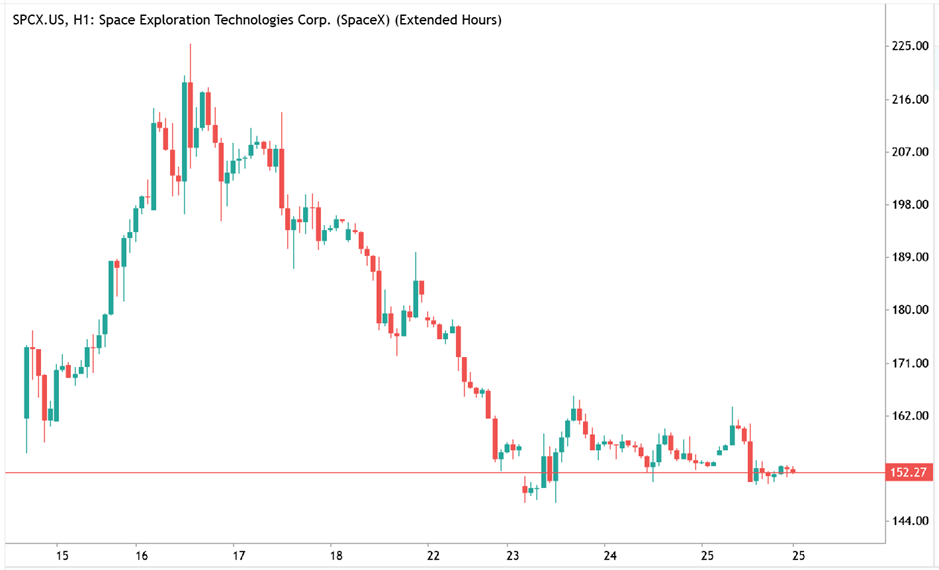

We are back to zero trillionaires here on Earth for now. After hitting a high of $225.64 on 16 June, SpaceX (SPCX.US) has retreated by about 33% to now be trading much closer to its IPO level. At its high point, we were all closer in our wealth to Jeff Bezos, than Bezos was to Musk. That staggering gap between Musk and the rest of the world has been narrowed swiftly in the days since though, his worth dropping in hundreds of billions a day as the shine wears off the biggest IPO ever. Nonetheless, at $150 currently, it is still trading 11% higher than where it listed, with a market cap hovering either side of the $2trillion mark. But no company has ever lost $1trillion in market cap, and the momentum is inarguably negative. With an extraordinary valuation based largely on the visionary's visions for the future, what can he say now to arrest the slide? Will the stock find an equilibrium level in the short term at least? Or will the froth continue to be extracted? Particularly as insiders become able to cash out longer term investments. Or will we see something more drastic hit the headlines to bolster the price, such as a merger with Tesla?

Next week

Thursday brings non-farm payrolls. Markets currently have a full hike by October priced in. NFP will be as key as ever in determining whether that bears out. Consensus is for unemployment to hold at 4.3%, with 115k jobs added. The ECB hiked rates earlier this month, the first rise there in three years. On Wednesday we will get the latest inflation reading from the EU. Headline inflation is expected is expected to hold steady at 3%, vs the ECB's targeted 2%.

Author

Scott Redford

Fintrix Markets

Through his 14 years in the industry, Scott has managed risk for a number of the world's biggest brokers, including IG and Pepperstone.