LNG enters timing phase as storage rebuilding and cargo competition intensify

Key takeaways

LNG enters the final part of the week inside a balanced but increasingly timing-sensitive market as Europe continues rebuilding storage while global cargo competition remains active.

European LNG flows remain broadly stable, with total EU flow near 379 mcm and concentration metrics still pointing to a balanced distribution across major terminals.

The Strait of Hormuz is moving from shutdown risk toward managed recovery, but shipping stress remains elevated and keeps access, routing and timing risk embedded in gas markets.

The current technical structure reflects a neutral rotational regime, with price holding around the 3.25 pivot while resistance develops near 3.28–3.32.

LNG moves from disruption pricing to timing sensitivity

LNG enters Friday’s session inside a market that is no longer driven by immediate disruption fears alone.

The geopolitical shock surrounding the Strait of Hormuz has started to move into a different phase. Shipping intelligence now describes the corridor as shifting from shutdown risk toward managed recovery, while the broader maritime environment still carries elevated stress across security, tanker and flow signals.

That distinction matters for natural gas.

LNG markets rarely normalize immediately after a logistical shock. Cargo scheduling, vessel availability, insurance conditions and terminal coordination all require time to adjust, even when headline risk begins to ease.

This is why LNG should be viewed as a timing market.

The question is not only whether supply exists. The deeper question is whether supply arrives at the right place, at the right time, under acceptable cost and routing conditions.

That framework is becoming increasingly relevant as Europe continues rebuilding storage while Asia remains an active source of cargo competition.

Europe remains in a balanced flow regime

European LNG flows remain broadly stable, but the composition of that stability matters.

The latest LNG European Master Report shows total EU flow at 379.07 mcm, with the system classified in a balanced regime. Concentration remains moderate, with the top three terminals accounting for 27.7% of flows, the top five for 40.4%, and the HHI at 549.9.

This is important because LNG markets become more fragile when flows are concentrated across a small number of terminals.

A balanced distribution reduces immediate concentration risk, but it does not remove timing risk.

The leading terminals remain TVB, Gate Terminal and Zeebrugge, although flows have softened compared with the previous snapshot. TVB remains the largest node at 44.2 mcm, while Gate Terminal fell by 13.6 mcm on the day and Zeebrugge remained broadly stable.

The picture is therefore constructive but not complacent.

Europe is still receiving LNG across a diversified network, yet the refill process remains sensitive to daily flow variation and cargo timing.

Storage rebuilding keeps flexibility valuable

The core issue for European gas markets is storage timing.

As the summer progresses, Europe must continue rebuilding inventories before winter demand returns. This creates a seasonal framework where the market becomes highly sensitive to flow reliability and cargo availability.

When storage levels are comfortable, buyers can remain patient.

When refill progress slows, flexibility becomes more valuable.

LNG sits directly inside that mechanism because it is the marginal balancing source for many European buyers.

Pipeline flows provide base supply, but LNG often determines how quickly the system can respond to weather shifts, demand surprises or regional supply disruptions.

This helps explain why natural gas can hold a firmer structure even when crude oil remains under pressure.

The latest cross-asset data show WTI still down 7.9% over five days, while Henry Hub natural gas is up 4.4% over the same period.

That divergence matters.

Oil is digesting the removal of geopolitical premium.

Gas is still pricing timing, storage and flexibility.

Cargo competition remains the deeper risk

The LNG market’s second major layer is cargo competition.

Europe is not operating in isolation. Asian buyers remain part of the same global cargo pool, and any increase in weather-sensitive demand across Asia can tighten the availability of flexible supply.

This creates a market where price formation depends on relative urgency.

If Europe needs cargoes quickly, prices must adjust.

If Asia increases demand at the same time, flexibility becomes more expensive.

If shipping routes remain stressed, timing risk increases further.

That combination is why LNG often behaves differently from other energy assets. It is less about outright supply and more about access to supply within a specific delivery window.

This is also visible in the shipping layer.

The broader shipping radar remains in a high-stress regime, with freight, flow, bunker and risk signals all present.

Meanwhile, LNG shipping equities remain mixed, with Flex LNG down 1.64% and Golar LNG up 0.44%, producing a modestly negative average for the category.

The signal is not one of broad expansion. It is a market still adjusting to route normalization, flow reliability and cargo allocation.

Macro data add another layer of timing risk

The macro calendar also matters.

Thursday’s US data showed firmer final GDP growth, while Core PCE remained aligned with expectations. For LNG, the effect is indirect but still relevant.

Stronger growth supports energy demand expectations.

Stable inflation data reduces the risk of immediate policy repricing.

A softer dollar can also influence global commodity flows by improving purchasing conditions for some non-US buyers.

The latest EcoModities data show the Dollar Index slightly lower on the day but still up over five days, while volatility remains positive.

That combination keeps the macro backdrop mixed.

LNG is therefore moving through a market where local storage needs, global cargo competition and macro positioning are all active at the same time.

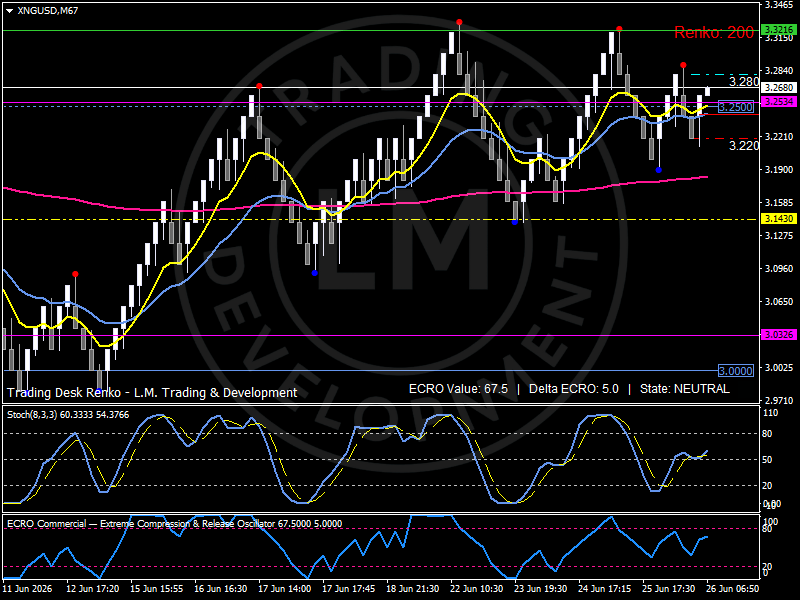

Technical structure: LNG rotates around the 3.25 timing pivot

The technical structure reinforces the timing-market interpretation.

The Renko chart shows LNG trading inside a neutral rotational framework rather than a clean expansion phase.

Price remains organized around the 3.25 participation pivot, which has become the central balance area of the current structure. Repeated rotations around this level suggest that the market is not rejecting the recent recovery, although it has not yet generated sustained continuation above the upper resistance corridor.

Resistance develops between 3.28 and 3.32, where previous upside extensions lost momentum.

Support remains concentrated around 3.22, followed by the broader stabilization region near 3.19.

The EMA configuration remains constructive but measured. Shorter-term averages are still operating above the broader trend layer, but price action has become more rotational after the latest recovery phase.

The ECRO indicator stands near 67.5 with a positive delta, while the market remains in a neutral state. That combination reflects active participation without full directional confirmation.

The technical picture is therefore consistent with a market waiting for timing confirmation from storage progress, cargo availability and route normalization.

Bird’s eye view

LNG currently operates inside a balanced but timing-sensitive market.

European flows remain diversified, with total EU LNG flow near 379 mcm and concentration metrics still consistent with a balanced regime.

The dominant market pivot remains the 3.25 area, while resistance develops across 3.28–3.32 and support remains concentrated around 3.19–3.22.

The key systemic variables are storage rebuilding, Europe-Asia cargo competition, Hormuz route normalization, shipping stress and summer demand sensitivity.

The market is no longer dominated by immediate disruption fear, but timing risk remains firmly embedded in price formation.

Outlook

LNG enters the final session of the week inside a market where balance does not mean comfort.

European flows remain stable enough to avoid immediate stress, yet the refill season continues to make timing important. Cargo competition remains active, shipping routes are still normalizing and the broader energy system continues adjusting after the recent geopolitical repricing.

The next phase will depend on whether European storage rebuilding continues smoothly and whether global LNG cargo availability remains sufficient as summer demand develops.

Until that becomes clearer, LNG is likely to remain a flexibility market where timing, access and cargo competition matter more than outright supply alone.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.