Latin America: How vulnerable is it beyond tariffs?

The vast majority of Latin American countries have been subject to 10% tariffs, the minimum rate, since April 2, imposed by the Trump administration. This leniency is due to the composition of their exports (raw materials and energy, whereas the Trump administration's “reciprocal” tariffs mainly targeted exporters of manufactured goods) and the fact that most of them have a trade deficit with the US.

Mexico's unique position in Latin America

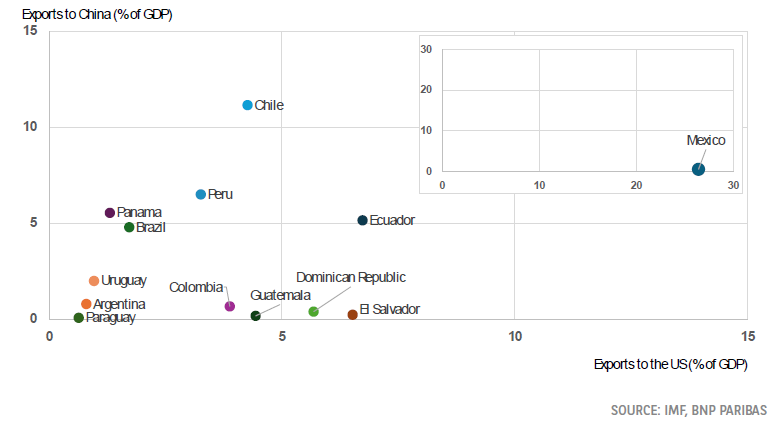

Mexico's position is unique in the region, making it particularly vulnerable to short-term developments in the US: exports to the US account for nearly 80% of total exports (27% of GDP) and the two economies are highly integrated. Under the trade agreement between the US, Canada, and Mexico (USMCA), Mexico is exempt from “reciprocal” tariffs. However, previous announcements remain in effect: a 25% increase is applied to non-USMCA goods, certain automotive goods, and steel and aluminum products. This affects nearly 50% of total exports. The IMF now forecasts a 0.3% contraction in Mexican GDP in 2025. The slowdown in the US economy and investor fears (following what are likely to be turbulent renegotiations of the USMCA) will add to Mexico's structural weaknesses. In the longer term, Mexico's positioning could enable it to benefit from the reorganization of world trade.

Limited direct effects on growth in Latin American countries

The direct effects on growth in Latin American countries should be limited, given their low degree of trade openness (exports account for less than 20% of GDP on average, excluding Mexico) and their low exposure to the US market (see chart). Furthermore, exports are mainly composed of raw materials, which are currently exempt from tariffs: copper for Chile and Peru, oil for Ecuador and Colombia. In the short term, Brazil could even benefit from the situation. The structure of its agricultural exports is quite similar to that of the US (soybeans, sugar) and could replace them in China, as was the case during Trump's first term.

Significant indirect consequences of the protectionist shock

However, the indirect consequences of the protectionist shock initiated by the US are likely to be significant: Latin American countries are vulnerable to falling commodity prices, weaker global growth and fluctuations in Chinese demand, especially as the authorities have limited room for manoeuvre to support economic activity. Their public finances are fragile and inflationary pressures could force a new cycle of rate hikes in Brazil, Colombia, and Chile.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.