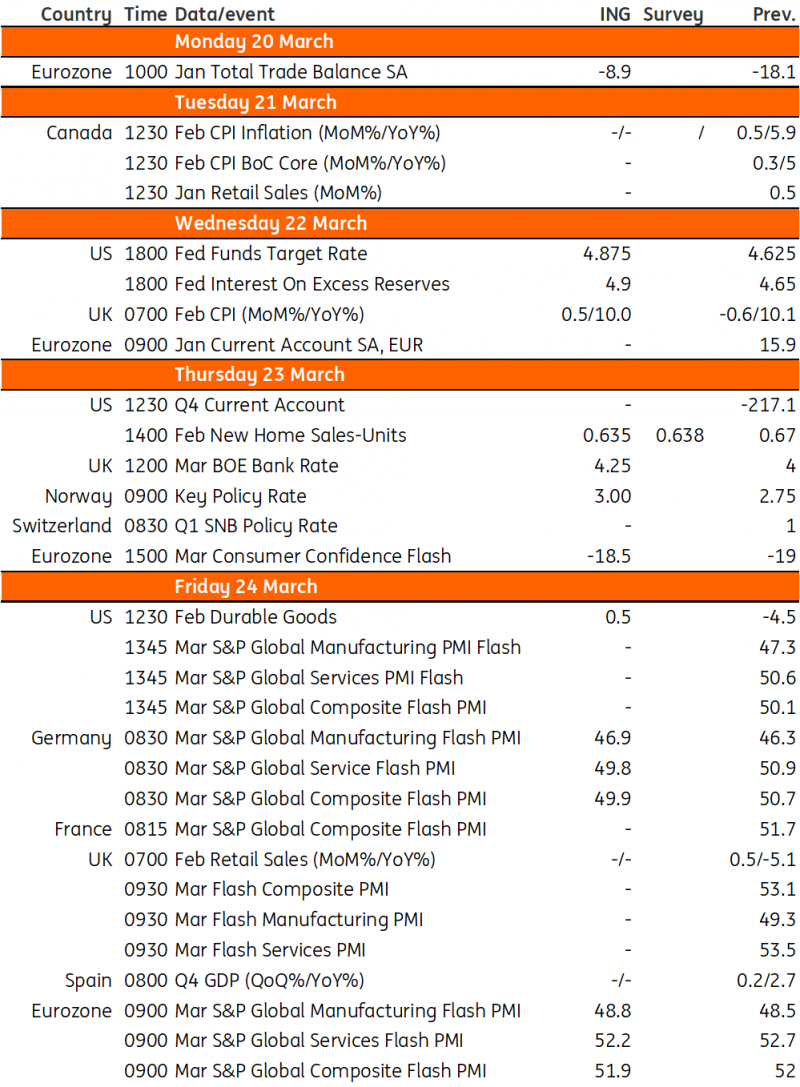

Key events in developed markets next week

Given the turbulence in financial markets this week, central bank meetings have become a much closer call. For the Federal Reserve, we narrowly favour a 25bp hike given the tightening lending conditions. For the Bank of England, we also lean towards a 25bp increase as the impact of past hikes has yet to feed through.

US: A close call, favouring 25bp as of now

Next week's Federal Reserve policy meeting is a very close call. On the one hand, inflation continues to run hot, the jobs market is strong and Federal Reserve Chair Jerome Powell’s testimony, which opened the door to a 50bp hike, suggested a desire to get interest rates a fair bit higher. However, lending conditions were already tightening and the fallout from recent events surrounding Silicon Valley Bank, Signature Bank and Credit Suisse will only make banks more cautious. Regulators are also likely to recognise the need to be more proactive in this environment, which could in turn feed into more pressure on the banks and greater caution with regards to who they lend to, how much they lend and at what rate. This is a de-facto tightening of monetary and financial conditions in the US which could weigh heavily on economic activity. The Fed may be wary that a no-change response could signal that they have finished tightening and the next move will be lower rates, but they can head that off by signalling in the text that this is a temporary pause and they stand ready to tighten again should conditions warrant it. Moreover, they also have the updated forecasts this month which could continue to show their central tendency is for rates to end the year higher than their current level. Nonetheless, with the European Central Bank hiking rates by 50bp without causing too many market ructions, this is likely to embolden the Fed to move by 25bp.

UK: Bank of England decision on a knife edge

Last month, the Bank of England signalled it might finally be done with tightening, or at least that it was close. It said it would be monitoring signs of “inflation persistence” and hinted the burden of proof was on seeing inflation fall back, rather than vice versa. Since then the data has been encouraging – wage growth is finally showing signs of having peaked, though it’s early days. The Bank’s own Decision Maker Survey has suggested firms’ pricing strategies are becoming less aggressive too. We’ll get one more inflation reading next week before Thursday’s meeting, but last month saw a surprise dip in core services CPI. Until the recent drama in financial markets, and on the basis of recent BoE communications, we felt this data probably wasn’t quite enough to steer the BoE away from a 25bp hike this month, but we also felt that if those encouraging trends continued, the committee could pause in May.

We’re still leaning towards that outcome, though clearly a lot can change in the days leading up to the meeting. It’s clear from recent communication that the bar for pausing is much lower at the BoE than at the ECB or the Fed, with officials noting that the impact of past hikes is still largely to feed through. On the flip side, last September/October’s volatility in UK markets after the ‘mini Budget’ saw the BoE use targeted measures to address financial stability issues, which policymakers indicated would allow the Bank’s monetary policy to continue focusing on inflation. We suspect that the philosophy of (at least trying to) separate inflation fighting and financial stability, which was also adopted by ECB President Christine Lagarde this week, will again underpin next week’s decision-making.

In short, the meeting is on a knife edge and to a large extent it will come down to whether stability in financial markets starts to return. Either way, expect the committee to remain heavily divided.

Eurozone: Little sign of a strong rebound

For the eurozone, all eyes will be on the PMI and consumer confidence data for signs about how the first quarter is shaping up. So far, sentiment data has painted a relatively positive picture of the economy in February, but hard data for the first quarter shows little sign of a strong rebound. Also interesting will be the trade balance for January, which has seen big moves in energy import volumes and prices.

Switzerland: Central bank will act with caution

In Switzerland, since the beginning of the year, inflation has continued to rise and exceed expectations, reaching 3.4% in February, after having fallen in the second half of 2022. As the Swiss National Bank only meets once a quarter and has only raised rates by 175 basis points since the start of the tightening cycle (compared to 350 basis points for the ECB and 475 basis points for the Fed), recent inflation developments in Switzerland argue for a 50 basis point rate hike at the March meeting. A fortnight ago, this was a fairly safe bet, but recent developments in the financial markets have clearly reduced the likelihood of this happening. As Credit Suisse is one of the two largest banks in Switzerland, which implies that the systemic risk is greater there than elsewhere, the SNB will have to act with caution. Ideally, the SNB would like to manage the risks to financial stability with other instruments than interest rates, such as providing liquidity to banks that need it, so that it can continue to use interest rates to fight inflation. For the moment, this seems feasible, but one knows that market conditions can change very quickly. A conflict between the financial stability and monetary policy objectives could emerge, forcing the SNB to act more cautiously in its rate increases. In conclusion, our baseline scenario remains a 50bp rate hike, but the probability of this has seriously diminished, and neither the status quo nor a 25bp hike can be ruled out. Unlike the ECB, the SNB has not pre-announced anything, so it is freer in its choices.

Key events in developed markets

Source: Refinitiv, ING

Read the original analysis: Key events in developed markets next week

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.