Key drivers of recent market volatility: US jobs report fuels recession concerns

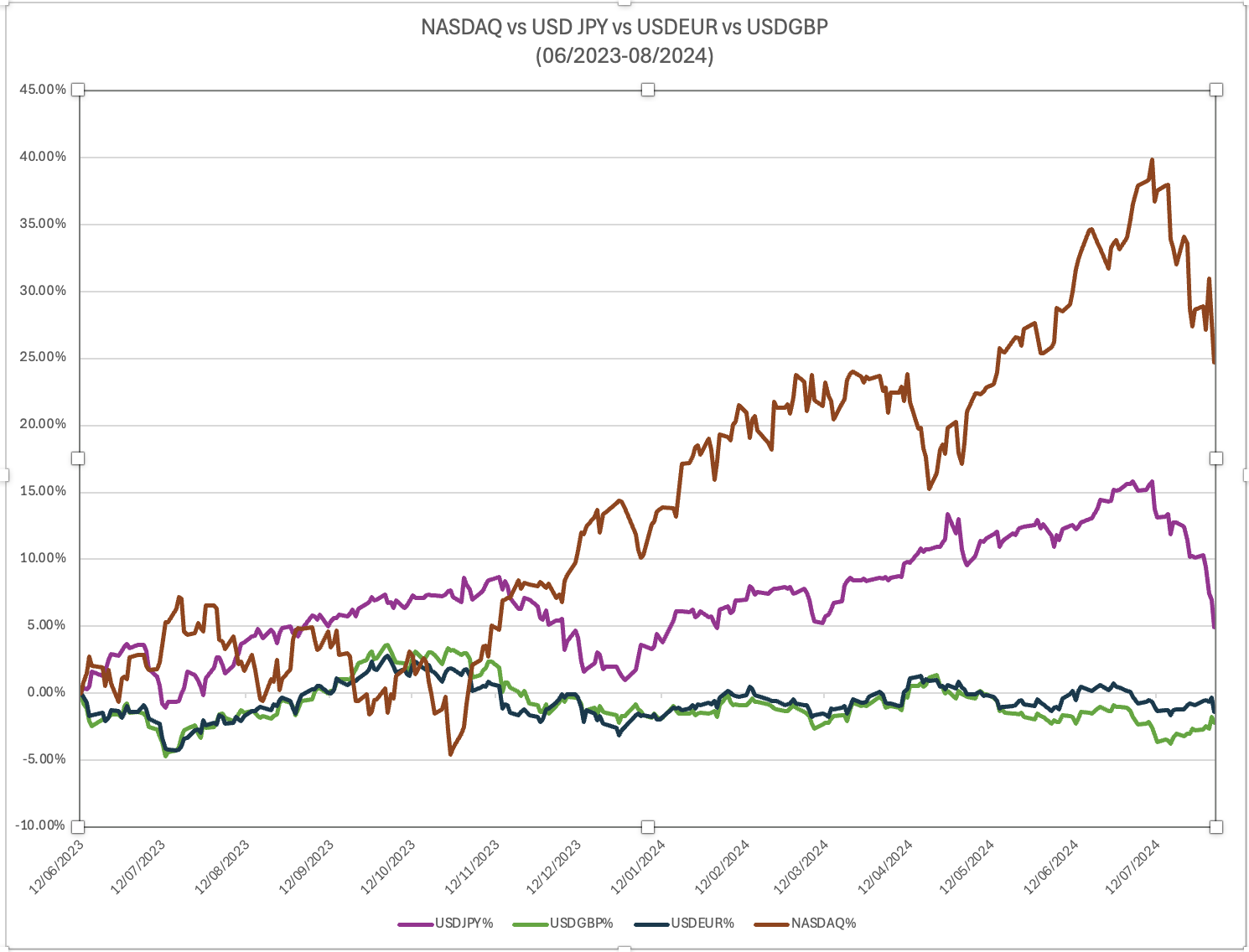

After the FOMC meeting last week, Chairman Powell hinted at a possible rate cut in September, initially causing a calm market reaction. However, on Friday, the BoJ raised interest rates, prompting further unwinding of the carry trade. The NASDAQ and USD/JPY have shown a correlated trend since January 2024, with the NASDAQ rallying and subsequently falling due to the carry trade unwinding.

Source: adopted from Reuters

The increased volatility over these two weeks can be attributed to three main factors: carry trade, geopolitical tension, and recession fears.

Carry trade effect

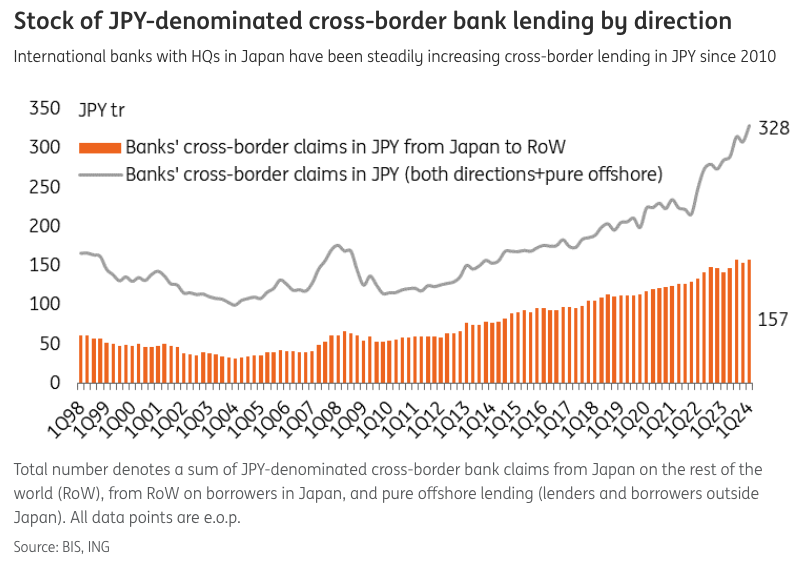

Cross-border usage of JPY

According to the Bank of International Settlements (BIS), banks' JPY-denominated cross-border claims reached JPY328 trillion (US$2.2 trillion) by the end of March 2024, a 52% increase from the end of 2021 (US$742 billion net of FX revaluation effect). This increase is due to the carry trade, which often leads to crowded trade unwinding. Periodic unwinding of JPY carry trades impacts global markets. I highlighted the significant influence of the BoJ's decisions on global markets in the article "Monetary Maneuvers: How Japan's Decisions Affect Global Markets" on 25 June 2024.

Source: ING

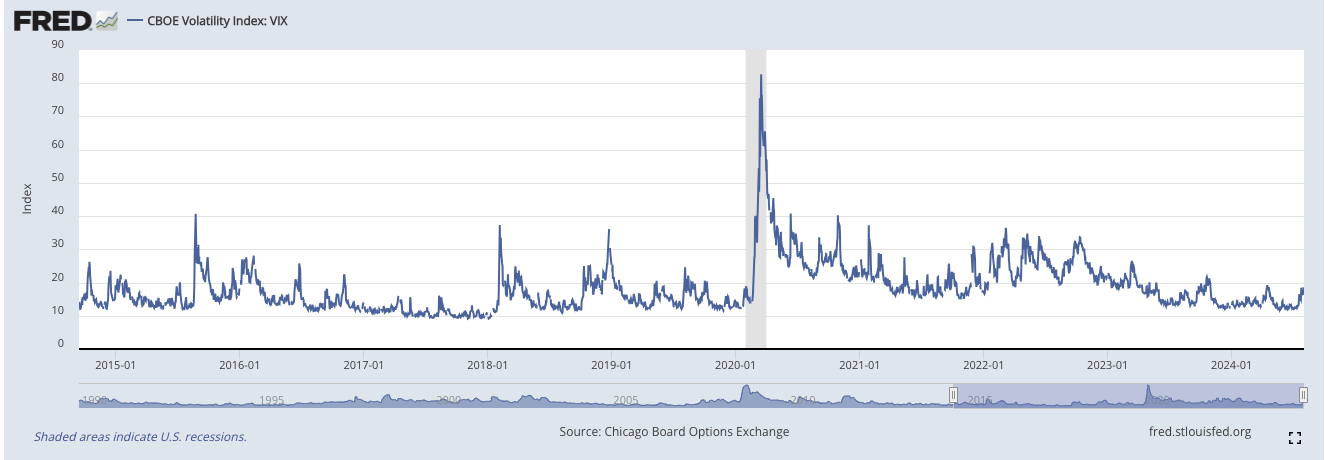

Short volatility trade

The chart shows periodic spikes in VIX volatility, averaging every 38 days, with a maximum duration of 60 days and a minimum of 28 days. Recent stock market corrections have triggered short squeezes on the VIX, increasing volatility.

Source: FRED

Geopolitical tension

The assassination of Hamas leader Ismail Haniyeh on 31 July 2024 in Tehran, reportedly attributed to Israel, has caused market anxiety about potential Iranian retaliation and a broader Middle East conflict. This tension has triggered a risk-off sentiment and market correction, although such geopolitical events usually have only a temporary market impact.

US recession fear

The latest U.S. jobs report showed a significant slowdown in job growth, with nonfarm payrolls increasing by only 114,000 in July 2024, below the expected 175,000. The unemployment rate rose to 4.3% from 4.1% in June, triggering the Sahm Rule, which signals a recession. In response, three senators urged Federal Reserve Chairman Jerome Powell to cut interest rates. This, along with former New York Fed Governor William Dudley's call for rate cuts, has led to speculation about worse economic data. The timing, just one week before the FOMC meeting, has increased scrutiny on the Fed's next move and raised concerns about the economy.

Technical analysis

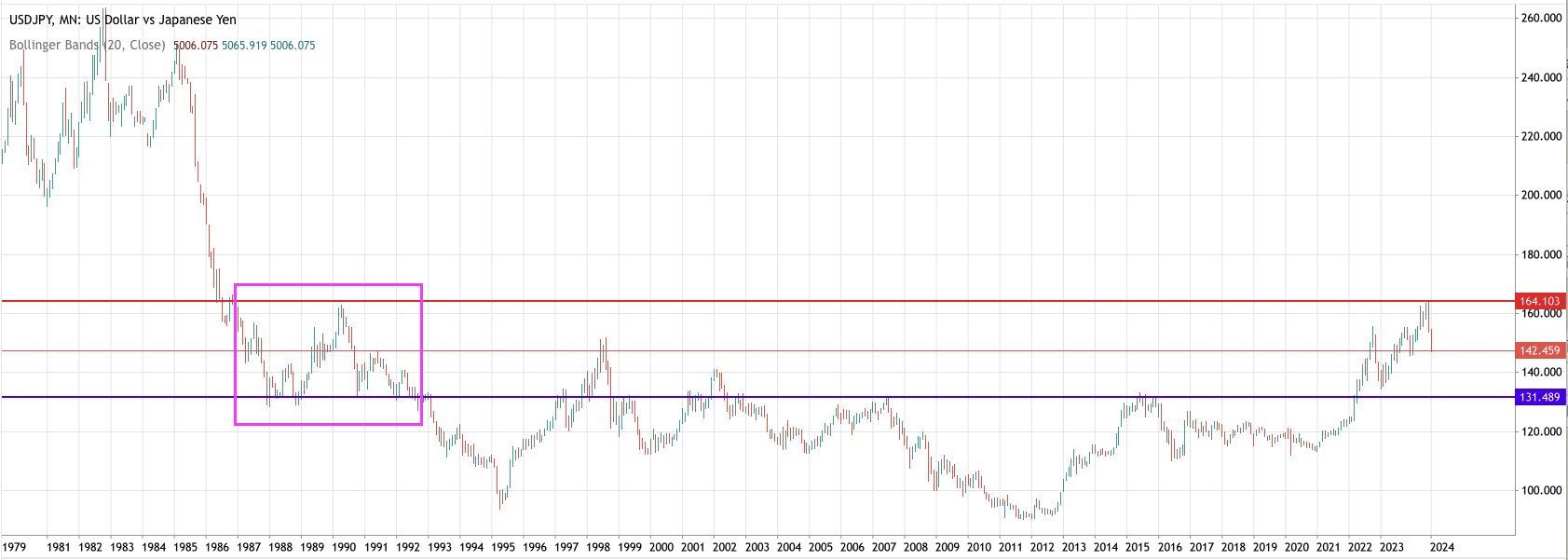

Source: Deriv MT5

USDJPY is have form a complex head and shoulder bottom, and it’s shoulod have just finished the 2nd shoulder, it’s should follow the left hand side pattern which was high lighted in purple rentango. Initial support 137.38 to 131.

Source: trading view

For S&P 500, it’s still having higher high and higher low, so the trend has not been destroyed yet. Though the stochastic suggest more correction is possible, but we have not be about to draw the conclusion that year high is in.

Conclusion

The recent increase in volatility is due to the unwinding of carry trades rather than an impending recession. Chairman Powell should not yield to senators' suggestions for faster rate cuts, as there is no immediate crisis. After the unwinding of the yen-based carry trade was completed and market sentiment stabilised again, market participants will likely return, as liquidity has increased due to easing by the Fed, Bank of England, ECB, Bank of Canada, and BPoC, with only Japan tightening its monetary policy.

Author

Prakash Bhudia

Deriv

Prakash Bhudia, HOD – Product & Growth at Deriv, provides strategic leadership across crucial trading functions, including operations, risk management, and main marketing channels.