Japan: Economic and Monetary Policy Outlook

Executive Summary

Japan’s economy has expanded at a slow but steady pace for an extended period of time; however, recent economic data has indicated a potential pick-up in activity. A stronger economy should provide scope for the government to move forward with the planned consumption tax increase in early October.

A more solid Japanese economy also provides less of an incentive for the Bank of Japan (BoJ) to follow other major central banks and ease monetary policy. We believe the BoJ will maintain its current policy stance; however, we think the BoJ will continue making adjustments to its bond purchase program.

We think the BoJ will continue making adjustments to its bond purchase program.

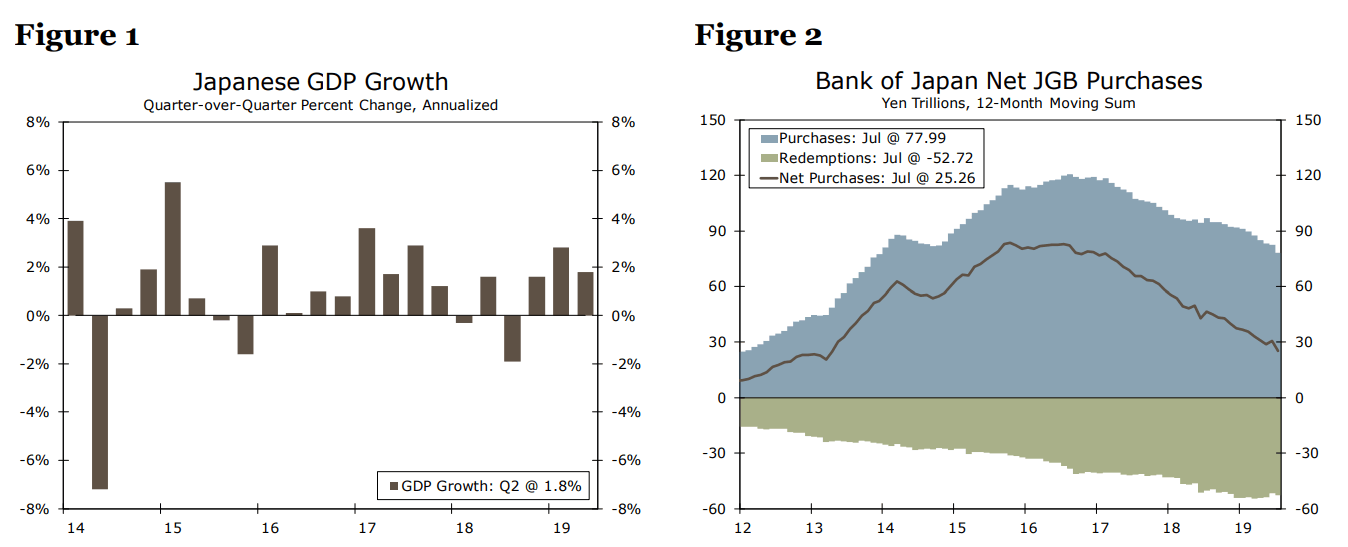

Economy Starting to Pick Up Steam

Japan’s economy was up and down during 2018, contracting in two quarters throughout the year and narrowly avoiding recession. So far this year, the economy has performed more strongly. In Q1, Japan’s economy grew 2.8% annualized, the fastest quarterly growth since Q3-2017, while in Q2 the economy expanded 1.8% annualized. As a result of stronger-than-expected growth in the second quarter, it is likely that we will upgrade our GDP forecasts in 2019 and possibly in 2020 as well.

Source: Datastream and Wells Fargo Securities

Perhaps the most telling indicator of Japan’s recent outperformance has been domestic demand, which grew 3.0% annualized in Q2 and a little over 1% in Q1. Historically speaking, these are relatively strong domestic demand numbers for Japan, while final private consumption has improved to start the year as well. In the second quarter, private consumption expanded at 2.5% annualized, also the strongest growth rate since mid-2017.

Solid domestic consumption in Japan should provide the government with the scope to pursue its planned increase to the consumption tax. As a reminder, Japanese Prime Minister Shinzo Abe planned to increase the country’s consumption tax rate to 10% from 8% as early as 2015; however, the hike has been delayed twice due to the potential impact on the economy. Given the strong performance of the economy this year, we believe the Japanese economy will be able to absorb the negative effects of the tax hike. As of now, we forecast only a moderate drag on GDP growth, and expect the tax increase to boost CPI inflation above 1%, but still below the Bank of Japan’s target of 2%.

We expect the tax increase to boost CPI inflation.

Bank of Japan to Buck the Easing Trend

Over the past nine months, global monetary policy has shifted towards a more dovish stance. The Fed has cut its policy rate by 25 bps, while the ECB has signaled it is likely to cut rates further in an effort to support the Eurozone economy. Other major foreign central banks have eased monetary policy as well, with the Reserve Bank of Australia and Reserve Bank of New Zealand cutting interest rates, while emerging central banks have also started lowering policy interest rates.

Given the renewed strength in Japan’s economy, and our view for only a moderate impact from the consumption tax hike, we believe the BoJ will not ease monetary policy any further at this time. Instead, we believe the BoJ will continue to purchase Japanese government bonds (JGB’s), but potentially at a slower pace. Since mid-2016, the BoJ has tapered its purchases of JGB’s, although it will likely continue net purchases for the time being.

We believe the BoJ will not ease monetary policy any further at this time.

While we expect the BoJ to continue purchasing JGB’s, we also think the Japanese central bank could continue making adjustments to the tenor of government bonds it will look to buy. In June and July, BoJ officials indicated some concern over a flattening yield curve, and suggested actions could be taken to address these concerns. Late last week, the BoJ made changes to its bond purchases across three separate maturity zones, as the BoJ looks to address its concerns over a flattening JGB yield curve. BoJ officials cut purchases of JGB’s in the three-to-five year maturity range, while also lowering purchases of longer-term bonds. In addition, the BoJ increased its purchases of short-term government bonds. These actions lower the yields on short-dated JGB’s, while resisting declines for yields at the longer end of the curve, effectively steepening the Japanese yield curve. In addition, we view these actions as compatible with a steady policy from the BoJ (10-year yield target near zero percent, with a tolerance band of +/- 20 bps) in the sense that the changing composition of the central bank’s bond purchases acts to resist a decline in longer-term bond yields.

Author

Wells Fargo Research Team

Wells Fargo