ISM Manufacturing PMI Preview: Why it could be the trigger for a big greenback comeback

- August's US ISM Manufacturing PMI is set to show an ongoing retreat from the highs.

- The indicator and its employment component serve as the last job report hints this time.

- Investors are waiting for a trigger to buy the dollar after Fed Chair Powell's blow.

Uncertainty breeds market volatility – and that may happen now as investors only have little information ahead of Friday's all-important Nonfarm Payrolls report. The ISM Manufacturing Purchasing Managers' Index is the last NFP hint and there are good reasons it could benefit the dollar.

August's job figures have become more critical to markets after Federal Reserve Chair Jerome Powell refrained from committing the bank to tapering its bond-buying scheme. The Fed buys $120 billion per month. While he noted progress and "thought" the Fed could reduce its massive program, he fell short of making a commitment, implying more data is needed.

During most months, the ISM Services PMI – a snapshot of America's largest sector – has the last word in shaping NFP expectations. This time, the first Friday of the month comes early, thus changing the order and making that service sector survey obsolete. In turn, that raises the importance of the Manufacturing PMI, despite its focus on the smaller industrial sector.

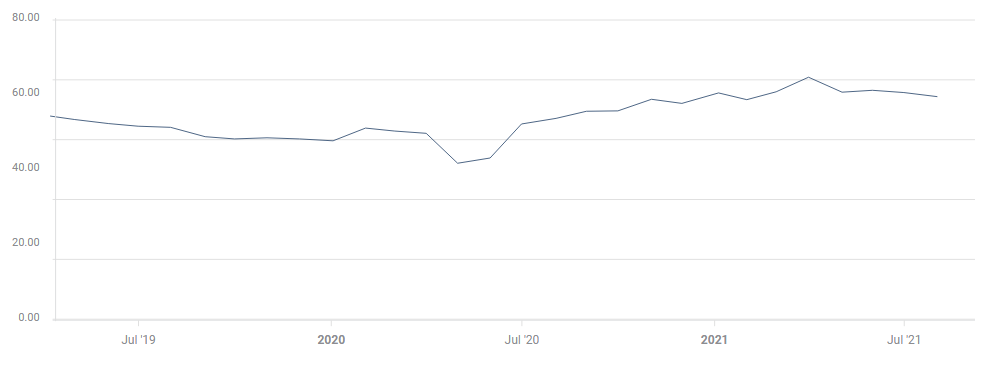

Economists expect a third consecutive decline in the headline ISM Manufacturing PMI from 59.5 in July to 58.5 in August. That is a significant fall, but not a collapse. Lower estimates make sense after two consecutive disappointments and drops – and also like the spread of the Delta covid variant weighs on business sentiment. Nevertheless, it may be marginally too pessimistic.

Source: FXStreet

More importantly, the Employment component may grab the attention as an NFP hint and especially in the absence of the services sector figure. Also here, projections stand at a decline from 52.9 to 51.4 points, a considerable 1.5 point fall.

After several months under the 50 level – representing contraction – the Employment component leaped above that threshold and showed that the shortage in labor is beginning to ease. Therefore, an immediate decline seems like a low bar to cross.

Dollar reaction

Given the relatively low expectations for the headline and especially the employment component, there is room for an upside surprise that could boost the dollar. The special focus on the publication – due to it being the last NFP hint and the importance of this jobs report – implies a relatively strong reaction.

Another reason to expect the greenback to stage a comeback stems from the fact that markets are in constant search of a new narrative. They also tend to return to previous levels more than they opt for big breakouts. In this case, even a small upside surprise could serve as a trigger – or an excuse – to jump on the dollar.

Conclusion

The ISM Manufacturing PMI is of higher importance due to the timing of the publication ahead of critical jobs figures and the late services sector publication. Relatively low expectations indicate an upside surprise is more likely than not, and markets may use this event to change course.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.