ISM Manufacturing PMI Preview: NFP Hint? Inflation component to steal the show, rock the dollar

- May's ISM Manufacturing PMI is set to hold onto high ground and serve as a signal toward the jobs report.

- After 13 upside surprises, the inflation component may steal the show.

- An energetic post-long-week mood could add to volatility.

Has the bitterly disappointing jobs report been a one-off or a reason to worry? In normal times, that would be the most significant question on investors' minds, and the headline ISM Manufacturing Purchasing Managers' Index would serve as the first hint. This time is different.

While Friday's Nonfarm Payrolls' figures for May are undoubtedly crucial, markets are rattled by the Federal Reserve's other mandate – inflation. Ahead of the long Memorial Day weekend, the US reported that the Core Personal Consumption Expenditure (Core PCE) hit a peak of 3.1% yearly in April.

That beat already elevated estimates and raised concerns that the Fed would have to taper down its bond-buying scheme earlier than expected, en route to raising rates. The focus may easily shift from the headline PMI – and the employment component – to the Prices Paid statistic.

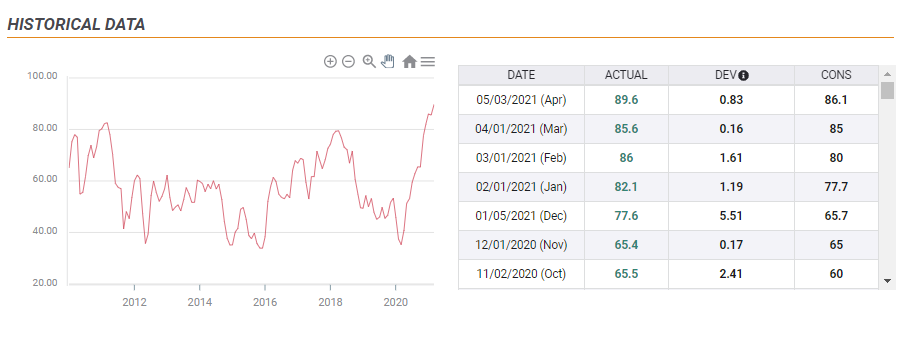

This data point stood at 89.6 in April, a record high and substantially above the previous peaks of the last decade. Moreover, it beat expectations I the past 13 months, showing that economists have been failing to grasp the rapid increase in price pressures. Will the upcoming report be the 14th in a row?

Source: FXStreet

The economic calendar is showing expectations for a repeat of 89.6 in May. A move above the 90 point level – and especially something closer to 95 – could boost the dollar.

Conversely, there is a case for falling inflation. Stimulus checks arrived on Americans' doorsteps in mid-March and the a substantial chunk was spent in April. Perhaps expenditure cooled down in May, allowing prices to decline. A fall to 85 or 80 may send chills down dollar bulls' spines.

Circling back to the headline, it is projected to hold up at 60.7, pointing to robust expansion in the industrial sector but below the peak of 64.7 recorded in March. If it slips below 60, it could weigh on the greenback. A minor increase, especially one above 65, would be positive, but seems highly unlikely now.

The Prices Paid component and headline will likely take attention from the employment component – especially as fewer people work in the manufacturing sector in comparison to the services one. The importance of this figure is due to the timing – it is released ahead of the Services PMI.

How much impact will the release have on the dollar? Volatility has been low on Monday, typical to a bank holiday in both the US and the UK. However, while some traders return to their desks with a hangover, others accumulate energy over the long weekend and may be ready to push currencies in a specific direction. Volatility could be higher than usual.

Conclusion

After the surge in Core PCE, inflation is firmly in the spotlight and the ISM Manufacturing PMI's Prices Paid component is the center of attention on Tuesday.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.