Is the US Dollar’s reserve currency status at risk?

Is the US Dollar’s reserve currency status at risk? If so, what does that mean for the Greenback?

For full disclosure, I am not an economist, I don’t have letters after my title, and I tend to have a simplistic view of the world. That said, I’ve lived through multiple cycles and have concluded that the most intelligent people in the room often overlook the obvious because they get caught up in academic arguments and theories. This is my humble take on the reserve currency debate and the fate of the US dollar.

What is a reserve currency?

A global reserve currency is one that is widely accepted for international trade, debt repayment, and as a store of value. Nearly 90% of global transactions via SWIFT (Society for Worldwide Interbank Financial Telecommunication) wires involve the dollar. Because of this role, central banks and governments hold significant stores of dollars. For this reason, a reserve currency is expected to be relatively stable in value and backed by a trustworthy government and a healthy economy. Before the dollar, the British Pound and gold acted as the world’s reserve currency. Having a reserve currency status brings a level of prestige and influence to the issuing country, but there are significant economic drawbacks that are often overlooked. In fact, one could argue that this system has significantly contributed to the decimation of the US middle class.

Reserve currency benefits

The world benefits from a reserve currency policy (regardless of the chosen currency) because it standardizes global trade terms to encourage market liquidity. Like futures contracts, which are standardized to allow for simple buying and selling without negotiating terms, having a single currency for pricing and transacting in commodities, such as crude oil, enhances efficiency by reducing currency risk and simplifying logistics.

The US enjoys some benefits of being the world’s primary currency, such as currency stability, compliments of widespread use and liquidity. Economic influence and sanction leverage (we control SWIFT) and lower borrowing costs (ideally, the demand for dollars means a demand for Treasuries because trading partners need a place to park those dollars). However, we have squandered these advantages by employing all bark and no bite sanctions, which have reorganized global trade with sanctioned nations but not thwarted it. Further, we have allowed our leaders to get drunk on cheap financing to the point that we have abandoned all fiscal reason and have dug a hole we might not be able to climb out of.

Reserve currency drawbacks

Our foreign trading partners are perpetually accepting political risk and US destabilization risk. They are also at the mercy of US monetary and fiscal policy due to fluctuations in the dollar. Thus, it should be no surprise that the new administration's uncertainty has triggered a moderate exodus from the dollar to gold and the euro. Similarly, there has been a liquidation of US Treasuries as cash is repatriated to other nations. However, in the big picture, we suspect governments, central bankers, and foreign investors participating in this knee-jerk reaction will eventually realize the grass wasn’t greener on the other side. The US dollar is still the most stable and liquid currency, while Treasuries are the most secure asset to hold, with the highest yield per unit of risk to boot.

Being a reserve currency isn’t all candy and roses. The high demand for dollars by trading partners keeps the dollar well bid, which has played a significant role in the gutting of the US middle class. A higher dollar makes US exports appear more expensive, making it more difficult for US farmers, ranchers, and producers to compete on the global stage, ballooning the trade deficit. Further, it abolishes our independence from shocks occurring in other parts of the world.

As mentioned, the US has turned a positive into a negative regarding the privilege of cheap money. The US reserve currency status enables cheap borrowing and encourages the US government to get drunk on debt.

Lastly, the demand for Treasuries by overseas investors looking for an attractive place to park dollar reserves can be a double-edged sword. When things are good, the US can borrow at low rates and offers a stable and confident interest rate market. But when the tide turns on US sentiment, as we have seen in recent months, the Treasury market can be weaponized. In other words, governments and Central banks holding large amounts of US Treasuries might aggressively liquidate their holdings to cause a spiteful spike in interest rates. From my view, this is akin to shooting themselves in the foot, but for a short time, it is a compelling warning shot.

What about BRICS?

Ten “Emerging” economies, including Brazil, Russia, Iran, China, and South Africa, have created an economic system known as BRICS to diversify away from the petrodollar (using the US dollar to price and transact in global commodity trade) and the SWIFT payment system. However, as chaotic as the US government can be, relying on reasonable codes of conduct from the likes of China and Iran feels like a poor life decision. Nevertheless, these countries feel alienated by the West, and I am a big fan of diversifying operations and business partners, so it is hard to argue against their logic. That said, should they create a reliable payment system outside of SWIFT in a stable currency, it will significantly reduce the influence the global reserve currency has on commerce. In short, sanctions will be even less effective. Complete detachment from the dollar and SWIFT anytime soon is unlikely. After all, BRICS was initially formed (then known as BRIC) in 2001. At that time, we were having the same conversations today; yet their progress has been minimal. This is because the dollar, its ease of use, and high-quality securities to hold with idle cash is a heck of a drug.

We have been here before

During the financial crisis, there was also talk of demoting the dollar from the pedestal of being a reserve currency. At the time, the dollar index traded in the 70.00s, not the 100.00s we see today. The euro and the yen were at all-time highs while the dollar struggled to hold ground. Celebrities demanded to be paid in euros, not dollars, and Moody's downgraded the US credit rating. Of course, just as the sentiment couldn’t be more bearish for the dollar and bullish for other major currencies, the markets reversed and haven’t returned to those levels since.

It could be argued that the weak dollar benefited the US’s recovery from the Global Financial Crisis. Our trading partners knew this and used it as a crutch for their plea to change the world’s reserve currency. During the weak dollar era, the US was benefiting greatly from its reserve currency status but that advantage has reversed itself over time.

The media is playing with our emotions

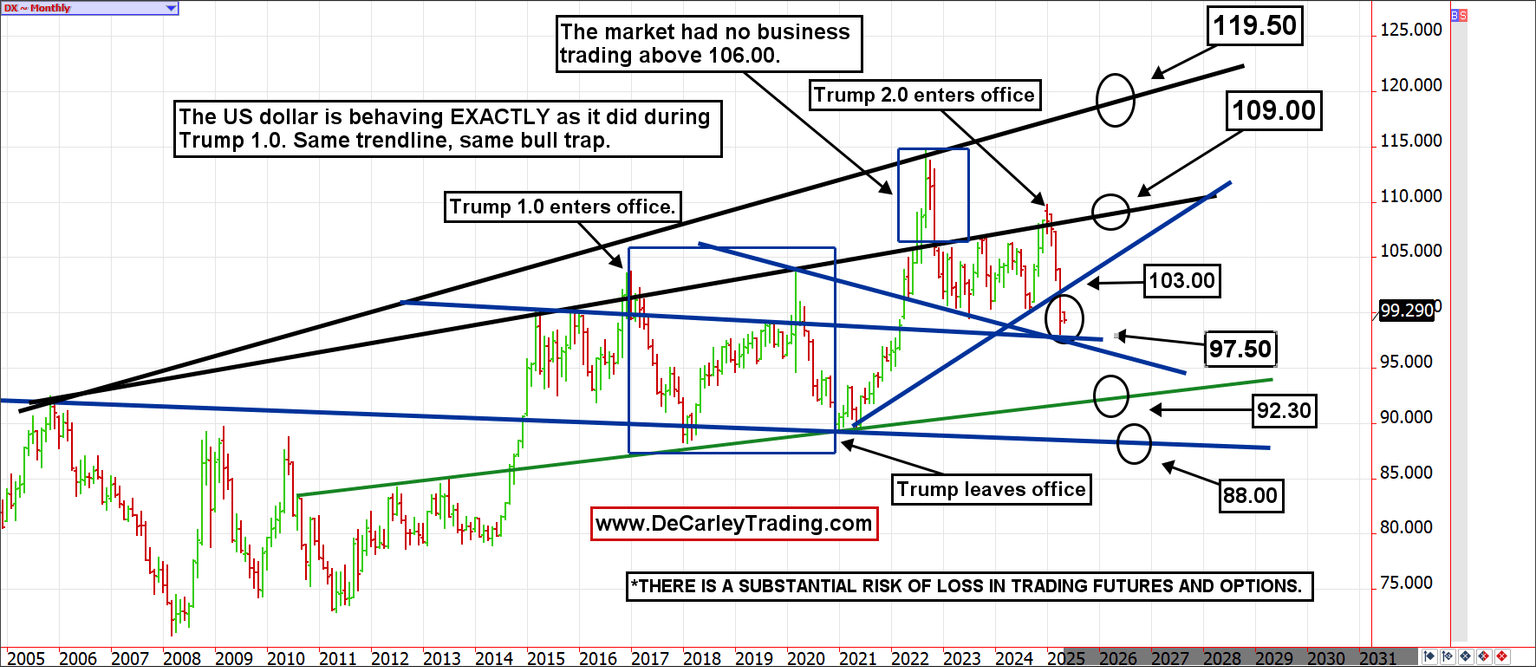

The media would have us believe that the US dollar is undergoing a historic freefall; if they believe this, they have short-term memories. Even after three months of selling pressure, the US dollar index is near 100.00, roughly the bottom end of the three-year trading range and a mere 6.00 to 8.00 points below the 20-year trading range trendline. There was a temporary spike above this trendline following the Russian invasion of Ukraine, but that was an emotional reaction to a global event, not a logical one. In other words, we are closer to historic highs than historic lows and are in the middle of a natural trading range (between the black and green lines on the chart).

Despite what has been touted as disbelief in how the currency markets have behaved during Trump 2.0, we are precisely following the path of the dollar during the last time Trump was in office. The same monthly uptrend line rejected the dollar index, leading to a slide into the high-80.00s. I suspect we get a repeat of that, but even that wouldn’t be cause for alarm or a reason to shop for an alternative reserve currency. Instead, it would level the playing field for US farmers, small businesses, and manufacturers. It would work against the trade deficit and favor our middle class. Yes, please!

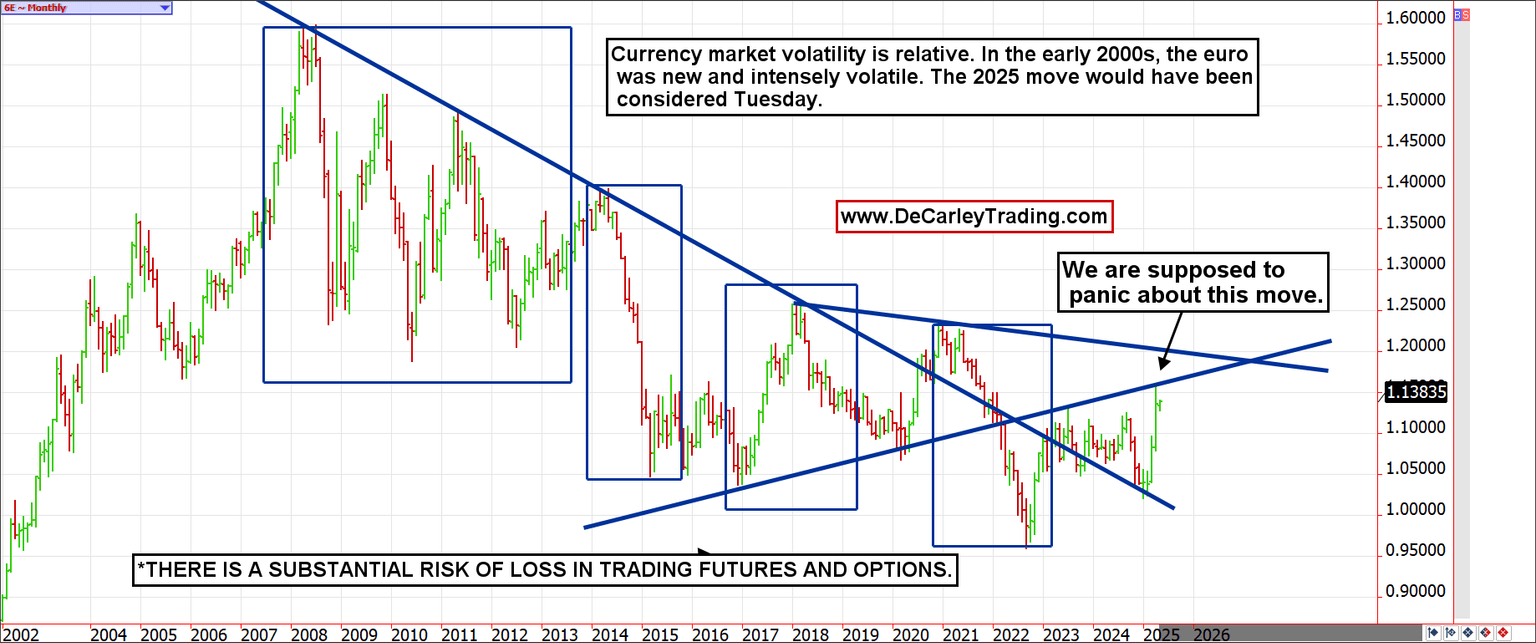

Currency market volatility is relative. We are coming off a few years of slumber, but that was the exception, not the norm. The 2025 volatility is child’s play compared to any time frame other than 2023 to 2024. Don’t let the headlines tell you how to feel. A monthly chart tells a more complete story; this is what the euro currency has looked like over the last 20+ years.

Conclusion

The US dollar and its reserve currency status have lubricated globalization. But for those who believe globalization has hindered certain parts of the US economy, such as manufacturing and small businesses, the US dollar's status as the reserve currency is seen as a catalyst for exporting middle-class prosperity away from the US and spreading it around the world in exchange for prosperity in the corporate sector (higher corporate earnings and stock values).

Regardless of your perspective and opinion, the dollar will be the world’s currency for the foreseeable future. The US and its currency are the least dirty shirt in the hamper. The consequence of foreigners selling dollars and treasuries to bring the money “home” is a less stable currency that earns lower yields.

From my view, being the world’s reserve currency is like hosting the Olympics; it comes with accolades and chest pounding but leaves the host country with a hangover and financial burden. No other country likely wants the baggage that comes with being a reserve currency because the system is currently working in their favor, not against them.

Author

Carley Garner

DeCarley Trading

Carley Garner is an experienced commodity broker with DeCarley Trading, a division of Zaner, in Las Vegas, Nevada. She is also the author of multiple books including, “Higher Probability Commodity Trading” and “A Trader's First Book on Commodities”.