Is It Worth Investing in Palladium?

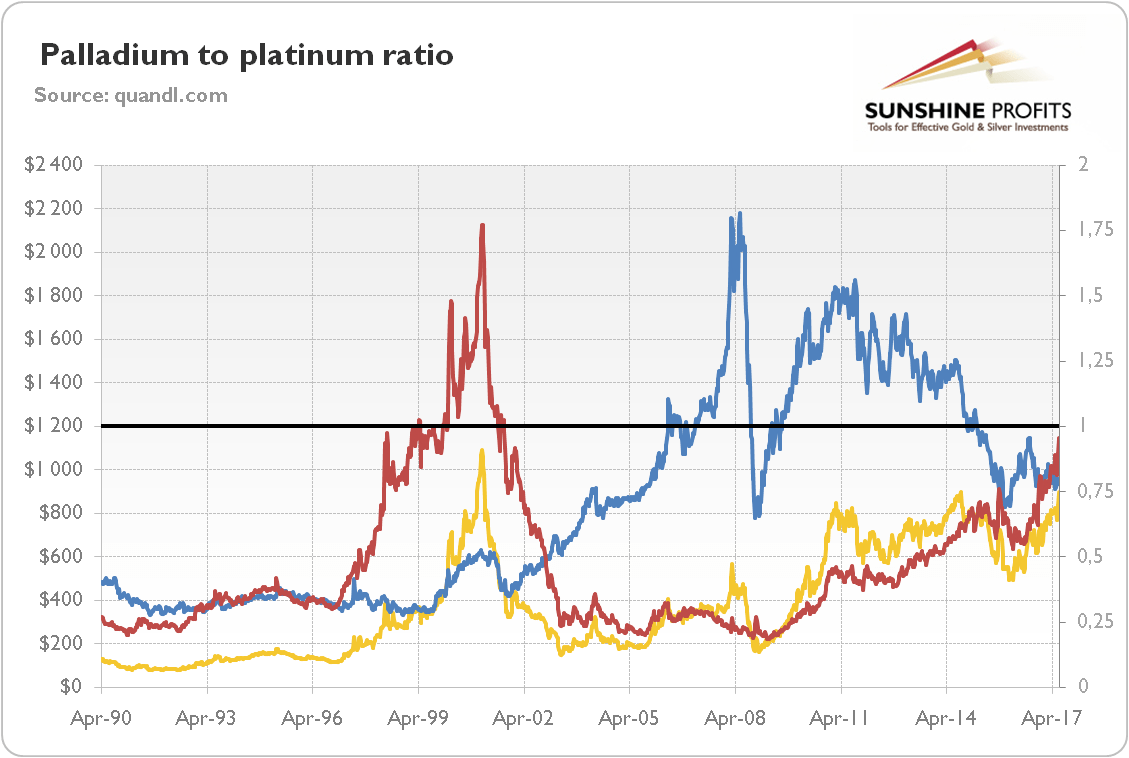

Palladium is another element with great importance to the modern economy, but it’s often overshadowed by the other more famous and expensive precious metals. As the chart below shows, palladium has been generally cheaper than platinum – its more expensive substitute in industrial use and jewelry.

Chart 1: The palladium to platinum ratio (red line, right axis), the price of palladium (yellow line, left axis, P.M. London Fix, weekly average), and the price of platinum (blue line, left axis, P.M. London Fix, weekly average).

However, the palladium to platinum ratio has been approaching parity. Does that mean it is the appropriate moment to invest in palladium? Let’s deal with that question, examining the supply and demand dynamics of this chemical element with the symbol Pd and an atomic number of 46.

Supply

The annual mining production in 2016 amounted to only about 6.7 million ounces. It came mainly from Russia (41percent) and South Africa (38.1 percent). Meanwhile, recycling added about 2.5 million of ounces. It means that the total supply was 9.2 million ounces.

The above-ground stocks of palladium vary from 7 million to 26 million ounces, which corresponds to from 1 up to 4 years of mining production. The existence of large stocks of palladium may explain why market deficits did not translate into higher prices.

The total supply of palladium is projected by Johnson Matthey to rise 1 percent in 2017, as an 8.6 percent rise in recycling (due to a continued recovery in the number of vehicles being scrapped in North America) is likely to more than offset a 1.9 percent decline in primary supplies (due to lower sales from Norilsk Nickel’s inventory). Hence, the supply side of the palladium market would not be supportive for the price of the metal.

Demand

In 2016, total demand for palladium amounted to 9.4 million ounces. It was made up of three core segments: automotive (84.3 percent), industrial (20.6 percent), and jewelry (2 percent). As one can see, the shares do not add up to unity, as investment’s contribution was negative (investors liquidated 0.65 million ounces from their ETF holdings). Similarly to platinum, palladium is primarily an industrial metal with the dominant part of demand coming from automotive catalyst use.

However, in contrast to platinum, demand for palladium in jewelry has almost disappeared (although palladium is an essential part of ‘white gold’), while investments have remained in negative territory. Instead, the share of automotive demand is much higher, so the palladium market is even more dependent on the situation in the automotive sector.

Moreover, while platinum is mainly used in catalytic converters in diesel cars, palladium is adopted primarily in gasoline cars. This implies that platinum depends more on the European market, while palladium reigns in North American and Asian. And since the latter is cheaper, it displaces ‘little silver’ from the market.

According to Johnson Matthey, global demand for palladium will rise in 2017 by 7.6 percent to 10.1 million of ounces, thanks to the 3.6 percent increase in automotive demand (the sales of gasoline cars is likely to increase, as well as palladium loadings), the 4.6 percent rise in industrial demand (palladium is mainly used in electrical, chemical and dental sectors), and the reduced outflows from the ETFs (given two years of heavy selling, ETF liquidation should slowdown). Thus, the demand side of the palladium market should support the price of the metal this year.

Market Balance and Price Outlook

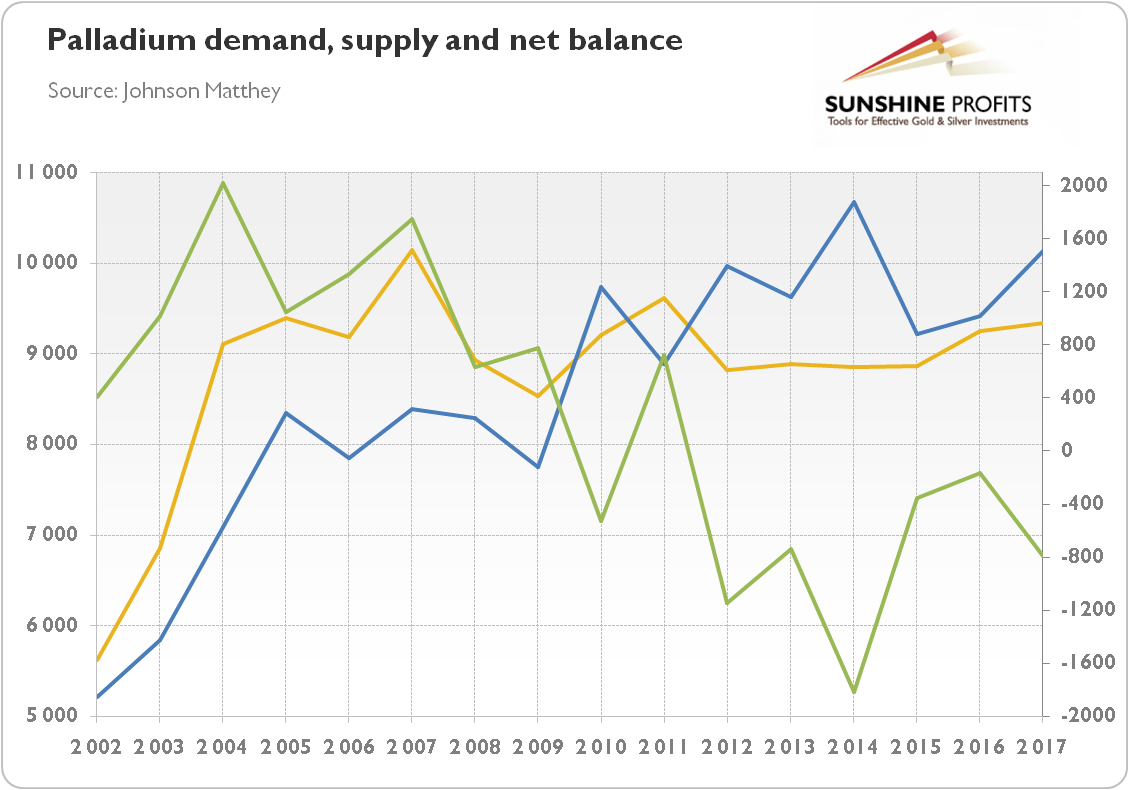

Given only the tiny rise in the supply of palladium and more decisive jump in demand for that metal (caused by higher auto demand and less disinvestment), the market deficit should widen to about 0.8 million of ounces in 2017, as one can see in the chart below.

Chart 2: Palladium demand (blue line, left axis, in thousands of ounces), palladium supply (yellow line, left axis, in thousands of ounces), and the net balance (green line, right axis, thousands of ounces) from 2002 to 2017 (the values for 2017 are projected).

Therefore, the price of palladium should be supported in the near future. We know that the above-ground stocks of palladium are relatively plentiful (and may be greater than the market expects), but market deficits at such heights cannot last indefinitely – and when the market eventually tightens, prices will need to rise, although it may take a while to deplete stocks.

Another bullish factor for palladium is the shift away from platinum toward more palladium in the automotive industry, although the price rally could undermine palladium’s competitiveness, especially since platinum is about twice as effective as palladium in catalytic converters (hence, given that platinum is trading with only a small premium over palladium, investors may turn to the former at some point in the future). The revival of global GDP growth bodes well for palladium prices, but if reflation falters, the outlook for palladium will deteriorate. And the rising share of electronic cars is another, although long-term, threat for the palladium market.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Arkadiusz Sieroń

Sunshine Profits

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017.