Is Credit Growth Driving Economic Growth?

We find that economic growth leads credit growth, not the other way around. Drawing on international examples solidifies the point that credit growth is simply one ingredient in sustaining economic growth.

The Relationship Between Credit Growth and Economic Growth

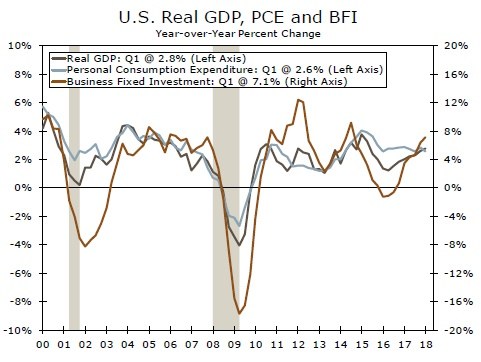

Despite varying degrees of volatility, business fixed investment and personal consumption move in sync with overall economic growth (top chart). In theory, the availability of credit should spur growth in other areas of the economy. In addition to generating revenue from the lender's perspective, credit availability allows businesses the opportunity to increase investment, by providing a means to finance projects. Credit availability also supports major spending decisions for households, such as financing an auto or home. Access to credit, therefore, should spur growth in business investment and personal consumption.

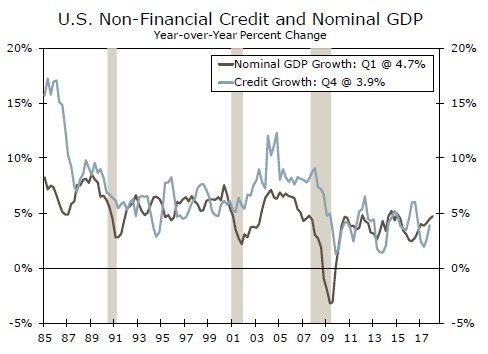

From a historical perspective, growth in nominal GDP and nonfinancial credit appear to have followed a similar trend over a business cycle (middle chart). However, credit growth has never moved into negative territory, even when GDP experienced several quarters of negative growth following the 2008 recession. Nominal GDP rose 4.7 percent in Q1 and 4.5 percent in Q4 year over year, both slightly below its long-run average of 4.9 percent. Meanwhile, total credit rose a mere 3.9 percent on a year-ago basis in Q4. Total credit is further from its long-run average of 6.7 percent, exemplifying the recent weakness in credit growth.

The tame performance of credit over the current expansion is particularly interesting given the relatively low interest rates seen over the same period. This leads us to question if slower credit growth is a contributing factor to the weaker pace of the current expansion.

From a statistical perspective, our analysis finds that GDP growth leads credit growth in the U.S., but growth in credit does not drive growth in GDP. The practical implication of these findings is that credit growth alone does not stimulate broader economic growth. This is especially interesting given that theoretically both variables should move together.

A Brief Analysis of International Credit Conditions

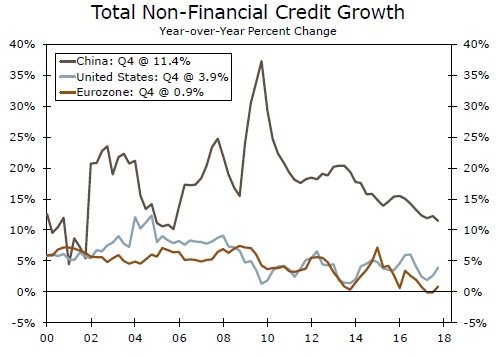

From an international perspective, credit growth has followed a similarly modest trend over the past several years (bottom chart). In China, for example, credit growth has slowed as the country continues its transition from a production to consumption model of growth, with the government attempting to reign in the explosive pace of business debt seen over the past decade, even as economic growth has remained steady. In the Eurozone, where the structure of the economy more closely aligns with that of the United States, credit growth also remains lower relative to the pre-crisis period, rising on average just 4.7 percent over the past 17 years.

These trends of slower credit growth amid solid overall economic growth lead us to believe that there could also be a similar relationship between credit and economic growth on an international basis. Sustained GDP growth therefore likely requires broader stimulation of the economy beyond simply fostering favorable credit conditions.

Author

Wells Fargo Research Team

Wells Fargo